SOTP Update on Bakkt ($BKKT)

• Transchem warrants (BSE: 500422) @ ₹303.9 — ~$123M, net of the unpaid 75%

• 28% of Bitcoin Japan (TYO: 8105) @ ¥204 — ~$25M

• Cash (Q1) — ~$83M

Total: ~$231M. Market cap: $331M.

So ~70% of the company is cash plus two strategic stakes — and the market is pricing the operation (the licenses, Bakkt Markets, the Agent, all of DTR) at ~$100M.

Disclaimer: the above is not to say that they could monetise the India and Japan stakes at these prices (nor would they want to).. and if anything, they trade at these valuations precisely because of Bakkt’s involvement and the future promise it comes with. And the cash of course is still burning for now, so a haircut is fair.

Bakkt $BKKT is currently experiencing an aggressive wave of open-market accumulation driven by independent director Michael Alfred. Over a thirty-day window, Alfred deployed over seven million dollars of his own capital to acquire 865,000 shares. This massive financial commitment signals profound internal confidence that the market is severely undervaluing the ongoing strategic pivot toward a highly lucrative institutional stablecoin and cross-border payment platform. Could this bold multimillion-dollar insider bet be the definitive leading indicator that a historic operational turnaround is quietly underway?

I have purchased an additional 280,000 shares of BKKT via my affiliated entity Alpine Fox LP. Alpine Fox LP now holds 905,000 shares in total and has become the 4th largest institutional shareholder in the company. See SEC Form 4 filing here: https://t.co/ADd32fLoVX

Decoding Bakkt’s Investor Day, Quote by Quote

Disclaimer: What follows is analysis and speculation. Nothing discussed below regarding unnamed partners has been signed, announced, or confirmed by Bakkt (NYSE: $BKKT). Bakkt’s own presentation footnotes state that no binding commercial agreement with a named telecom operator has been publicly disclosed. All candidate names in the speculation blocks are my own inference. I hold a long position in BKKT. This is not financial advice; don’t do what I do.

Source materials:

· 📊 Investor Day 2026 presentation: https://t.co/Iv1YCBfoI5

· 🎥 Webcast replay + full event materials: https://t.co/VZjBO0tviV

· The webcast is also on YouTube: https://t.co/zhgijBtq5W

______

On March 17, 2026, Bakkt held its first-ever investor day. I’ve now been through the full webcast transcript a couple of times, and tried to piece together any clues they gave, and highlight the choice of words used to describe certain aspects of where we can expect the company to be in 6-12 months.

This piece does three things. First, it catalogues the actual language used — the momentum vocabulary, the timing promises, the pipeline claims. Second, under the quotes that matter, I speculate on who the unnamed counterparties could plausibly be, and why. Third, it maps what H2 2026 looks like if even part of this language converts to signed contracts — and what kind of re-rating that implies for a stock with this float structure.

Quotes are taken from the investor day webcast transcript. Emphasis throughout is mine.

______

Part I — The Momentum

Before the specifics, read the tone. This is the language the CEO (@akhsay_naheta) chose for his opening ten minutes:

· “We are entering the next phase of Bakkt’s growth with massive momentum behind us.” — Akshay Naheta, CEO, opening remarks

· “Our pipeline is primed, the regulatory path is clear and we are rewriting the definition of category-defining deals.” — Akshay Naheta, CEO, opening remarks

· “We are deep in discussions with several partners across the ecosystem and we’ve got immense momentum on that front.” — Akshay Naheta, CEO, on the accelerants slide

· “These are all commercial agreements with real volume and real economics and I’m extremely confident in each of these partnerships and what they’re going to deliver for Bakkt shareholders.” — Akshay Naheta, CEO, on the partnership slide (Better, Zoth, Nexo, AscendEX, Oobit)

· “We are extremely confident about our pipeline and our advanced conversations with a few partners, especially for the consumer fintech platform.” — Ankit Khemka, CPO, distribution section

Across roughly an hour of prepared remarks and Q&A, variants of “very near term” appear at least five times, “category-defining” at least four, “momentum” at least six, and “advanced discussions/conversations” at least four. This is not a team managing expectations down.

______

Part II — The Telco Quotes

This is possibly the most consequential claim.

· “For Agent, we’ve signed up tier-one telco partnerships across US and Europe which will embed connectivity into our fintech product.” — Akshay Naheta, CEO, prepared remarks

· “There are two to three large-scale telco players in each market and we are partnering with one of the top two or three telco players in each of those markets.” — Akshay Naheta, CEO, Q&A (responding to Dylan Heslin, Roth)

· “We have massive momentum from these telecom partners.” — Ankit Khemka, CPO, distribution section

Read that again. “We’ve signed up tier-one telco partnerships” is the language that was used; granted, the footnote on the deck says “no binding commercial agreement”.

Speculation: who is the telco?

Nothing below is confirmed. This is pattern-matching from public information.

Candidate 1 — Deutsche Telekom / T-Mobile US

The highest-probability inference. The constraint set: top-two-or-three operator, covering both the US and Europe, willing to embed eSIM into a third-party fintech app.

Now the relationship map: before founding DTR, Akshay was the SoftBank executive who personally architected the 2021 transaction in which Deutsche Telekom acquired SoftBank’s T-Mobile US stake and SoftBank became a major DT shareholder. He negotiated that deal directly with DT’s leadership. One group relationship — Deutsche Telekom — covers Europe’s largest operator and a top-three US carrier (~130M T-Mobile customers). T-Mobile already operates a subscale banking product (T-Mobile Money) that could be replaced or upgraded; DT has no scaled consumer fintech in Europe. This would be my best guess as to who they are close to announcing a partnership with.

Candidate 2 — Vodafone, via the Abu Dhabi relationships

DTR is Abu Dhabi-based and Akshay’s post-SoftBank network runs through the UAE. e& (Etisalat) is Vodafone’s largest shareholder. Vodafone is the one European tier-1 with proven telco-money DNA — M-Pesa, the most successful carrier-payments product ever built — and a footprint that maps directly onto the remittance corridors Bakkt keeps naming (Europe→South Asia, Africa).

______

Part III — The “Hundreds of Millions of Users” Quotes

The second unnamed counterparty class is more interesting than the telco, because the product architecture all but names what kind of platform it has to be.

· “From a Bakkt Agent perspective, we are looking at very large networks where you have hundreds of millions of users — either on the platform or already having touch points with these networks.” — Akshay Naheta, CEO, Q&A

· “It’s literally a — you skin the app and launch it, or if you have an existing platform, you embed our chatbot within it, and you can basically run on our regulated rails with all of the infrastructure and piping at the back to launch a fully-fledged fintech platform.” — Akshay Naheta, CEO, Q&A

· “We are in very, very advanced discussions on some category-defining deals and in the very near term I really look forward to updating you once we are ready to do so in accordance with SEC regulations.” — Akshay Naheta, CEO, Q&A

The phrase “embed our chatbot within your existing platform” is doing a lot of work here, and it narrows the candidate space considerably.

Speculation: who is the network?

Likely a messaging platform, most plausibly Telegram

Zaira is chat-native by design: voice, text, image inputs, single API endpoint, built to live inside a conversation. There is exactly one category of platform where “embed our chatbot” describes the native user experience: messaging. Telegram has ~1B users and an existing crypto wallet that is excluded from the US market precisely because it lacks regulated rails. Bakkt’s pan-US MTL coverage plus the NY BitLicense is the exact missing piece — the entire pitch of the investor day was “our regulatory infrastructure becomes theirs.” A US-regulated remittance agent inside a messaging app, aimed at diaspora corridors (US→South Asia, Philippines, Nigeria, MENA — the corridors Bakkt itself listed), would genuinely justify the phrase “category-defining.”

______

Part IV — The Timing Receipts

Every dated or dateable claim from the day, in one place. This is the section to revisit each quarter.

· “I think Zoth is something which will also go live over the course of the next month or so.” — Akshay Naheta, CEO, Q&A (March 17)

- The receipt: the Zoth MOU was only formally signed in May 2026 — two months after investor day — and definitive commercial agreements are still pending as of this writing. “Live over the next month or so” did not happen on schedule.

· “So far we’ve successfully done it for almost 57 countries and I don’t see any problems with us getting to 90 by the end of the year.” — Akshay Naheta, CEO, Q&A (payout country coverage)

· “We’re really looking forward to bringing that out to market in the next couple of months.” — Nicholas Baes, COO, on stablecoin/cross-border capability in Bakkt Markets

· “We’ve announced — or are very close to announcing — some very, very large partnerships. The discussions are progressing. We’re in advanced conversations and we expect aggressive growth at Bakkt Agent through the adoption of monthly active users on the platform. We have a very clear line of sight on that.” — Akshay Naheta, CEO, closing remarks

· “Really, all of the structural work — I would say 90% of it — is behind us at this stage.” — Akshay Naheta, CEO, closing remarks

· “Every dollar of this is either nonrecurring or already behind us.” — Karen Alexander, CFO, on the $66.8M of 2025 legacy charges

· “We have sufficient liquidity to execute across all three growth engines.” — Karen Alexander, CFO

______

Part V — The Picture They’re Painting for H2 2026

Here is the implied sequence, in management’s own claims:

1. Q3 2026: Bakkt Agent launches (reaffirmed on the Q1 call), with MAU becoming a reported KPI. The Zaira remittance app plus the Everyday Money app, distributed through at least one named telco.

2. A named tier-1 telco partnership is announced “in the very near term” — embedding eSIM and putting the consumer fintech product in front of a carrier customer base.

3. A “category-defining” distribution deal with a network of hundreds of millions of users — white-label or embedded-chatbot — is announced under the same timing language.

4. Zoth converts from MOU to definitive with live corridor volume, scaling toward the $1B annualized TPV that Zoth projects by year-end (from a $300M base that is currently Zoth’s volume).

5. Markets TTV ramps from ~$241M YTD toward the ~$2.5B year-end target — a ~10x ramp in three quarters — as Nexo, AscendEX, Oobit and the DTR stablecoin rails activate.

6. Payout coverage expands from 57 to 90+ countries by year-end.

If items 1–3 land — a launched product with a disclosed MAU number, plus one or two named partners — the re-rating math is straightforward and violent. Post-DTR there are roughly 42M shares outstanding; at ~$7.68 that’s a ~$320M market cap for a company holding ~$83M in cash, debt-free, with a 50-state MTL stack and a BitLicense. Two strategic stakes sit outside that cash line, marked to market at roughly $121M combined: ~$21.6M for its 27% of Tokyo-listed Bitcoin Japan (ex-Marusho Hotta, 8105) at today’s price, and an illustrative ~$99M on its unexercised Transchem warrants (BSE: 500422). A named telco or a messaging-platform deal is enough to move the stock into the $20–40 range on announcement momentum, before showing any fundamental proof.

The Pharaoh’s view: Bakkt’s investor day was full of promises, in a confident tone, indicating imminent (within 1-2 quarters) transformational announcements. The regulatory moat is real, the balance sheet is clean, and the unnamed-partner speculation above is genuinely asymmetric — this float does not absorb good news gently. But the company’s own footnotes tell you the deals aren’t signed, and the KPIs have no dates. Nothing is real until it’s binding. Until then, we (patiently, but not so patiently) wait.

The Company Inside Bakkt

Over the past year #Bakkt changed its CEO, its core business, its board and its balance sheet. The stock price still reflects the old company, not the new one – and that's the opportunity.

A few days ago I said I bought 22,000 shares at $10.20. Let me show you the company inside Bakkt.

Start with the old Bakkt. It was built inside the New York Stock Exchange. ICE, the NYSE's parent, launched it in 2018 and took it public in 2021 at a $2.1 billion valuation. Then it lost the plot. The first leg down came post-SPAC, when the original vision never materialized and the stock collapsed roughly 95%. The second leg came on March 17, 2025, when Bakkt disclosed in an 8-K that both Bank of America and Webull were walking from their contracts. Webull alone was 74% of crypto revenue. The stock fell 27% that day and shareholders sued.

Then, four days later, the company did something unusual.

On March 21, 2025 — the same week the existing revenue model died — Bakkt brought in Akshay Naheta (@Akshay_Naheta) as co-CEO and signed a commercial partnership with his stablecoin payments firm, DTR. If that name doesn't mean anything to you: Naheta spent five years at SoftBank investing next to Masa Son, with a hand in the ARM and Nvidia positions. By August, the old CEO was gone and Naheta was running the company alone. The loyalty business was sold off. The dual-class super-voting share structure was scrapped. The balance sheet was cleared out: no debt, $82.6 million in cash. In October, Mike Alfred (@mikealfred) joined the board, then Lyn Alden (@LynAldenContact) a few days later. And in January 2026, Bakkt formally acquired DTR. On paper, Bakkt acquired DTR. In substance, it was a reverse merger — the acquired company is now running the acquirer.

So when you pull up $BKKT today, the chart you're looking at belongs to a company that effectively no longer exists. New CEO, new core business, new board, a clean balance sheet. The only things that carried over are the NYSE listing and the licenses. And the licenses, as you'll see, are the one piece of old Bakkt actually worth keeping.

That gap is the entire opportunity. When the company underneath a ticker gets swapped out but the ticker, the name and the chart all stay, the price can sometimes stay stuck to the ghost.

Even the one number that looks current is misleading. The headline says Q1 revenue "collapsed 77%." But open the filing. Revenue was $243.6 million. Of that, $242.0 million was pass-through crypto cost. The actual margin left over was about $1.6 million. Bakkt's "revenue" was always gross transaction notional, a number that looks enormous and tells you nothing. The real cost of running this company is around $18.5 million a quarter, against $82.6 million in the bank.

Now look at what the new company owns.

The licenses come first. Pan-U.S. money transmitter licenses, a New York BitLicense, a European VASP license. And while that may sound trivial, it's actually what protects the business. Assembling that stack from scratch takes 2-3 years and millions of dollars. Plenty of bigger players have it — Coinbase, Circle, PayPal, Robinhood — but for each of them, licensed crypto payments is one piece of a much wider business. The faster route is M&A, which is why Stripe paid $1.1 billion for Bridge and Mastercard paid $1.8 billion for BVNK — both private. As far as I can tell, Bakkt is the only publicly traded, NYSE-listed company whose entire forward business is the licensed stablecoin payments rail. If you want public-market exposure to this, there is nothing else to buy.

Then the plan. Three businesses. Bakkt Markets is institutional trading rails, with transacting volume the company expects to grow from $241 million last quarter to around $2.5 billion by year-end. Bakkt Agent is programmable payments for AI agents, launching in Q3. An AI agent can't pull out a credit card. It needs licensed, programmable money rails, and very few companies can legally provide them. Bakkt Global is a capital-light international arm. The Japan position — $11.5M into Bitcoin Japan Corporation (TSE: 8105, formerly Marusho Hotta) — is marked at $31.7M as of March 31, a 2.8x return that includes $14.9M of cash already received from Rizap share sales. The India position is a $9.5M warrant subscription in Transchem (BSE: 500422), an Indian brokerage that will offer regulated access to offshore and tokenised investment products. The warrants are subscribed but not yet exercised — conversion is pending regulatory and shareholder approval — with an illustrative quarter-end mark of $44.3M (4.7x). Combined Bakkt Global asset value: $76M. Strip that out of the $445M market cap along with $82.6M of cash and you are left with an enterprise value of roughly $286M for the entire operating business — the licenses, the rails, Bakkt Markets, and a yet-to-launch Agent product.

Then there's the board. Lyn Alden (author of Broken Money) is on it - one of the most respected voices on how money actually works. She describes the financial system that's run since the 1970s as "antiquated monetary technology." She has now agreed to help govern a company building the replacement for it. Sitting next to her: Mike Alfred, who also sits on the $IREN board and recently bought 585,000 shares of Bakkt in the open market, and Richard Galvin, who runs an institutional digital-asset firm.

So what could it be worth?

Sum-of-the-parts, today. On 44.6M shares: cash is $1.85/share, Bakkt Global is $1.70/share at current levels (Japan $0.71 + India $0.99). That is $3.55/share of net assets before you value the operating business. Put the licensed, NYSE-listed payments rail at a 50% discount to what Stripe paid for Bridge and Mastercard for BVNK — call it $500-900M — and the operating business is worth $11 to $20 per share. SOTP fair value today: $15 to $25. The stock is trading at $10 following the rally this week.

From there, two paths to the bull case, and you don't need both. Path one: an acquirer decides buying the only public-market licensed rail beats building one, and pays a strategic premium. Path two — the one I think is underappreciated — the Clarity Act passes, the sector re-rates, and Bakkt trades like the public pure-play it is. If Markets and Agent together drive $200–300M of real (non-pass-through) revenue by year three, and the sector trades at 15–20x revenue — still a discount to where Circle trades today — that's a $3–6B company, or $60 to $115 per share. If multiples expand the way they did in 2021 and Bakkt commands a scarcity premium as the only public option, you can defend higher. Circle, the only public stablecoin pure-play, is worth $28 billion today.

One more piece I’m following with interest. Bakkt has changed its investment policy to allow it to hold Bitcoin on the balance sheet. Bakkt would be a Bitcoin treasury sitting on top of a real, licensed, operating business. The market currently prices that option at nothing.

The Pharaoh's view: the market is paying $10 for the ghost. The company inside is worth far more, and eventually the market will figure it out.

$BKKT investors 👀

@ICE (Bakkt’s biggest backer) is leading this regulated tokenized stocks push with OKX + Securitize.

Bakkt was created by ICE and is now focused on exactly this, tokenization, stablecoins, and digital infrastructure.

When NYSE’s 24/7 on-chain equities go live in H2 2026 @Bakkt tech is perfectly placed to handle the flow.

This could be the big tailwind $BKKT has been waiting for!

A bit more patience required

Tick Tok ⏳

@Buhlahkay@DeepVaue_Adv @BTC_Bella69420

We’ve already solved buying crypto.

But actually using it in real life? Still broken.

@mudra_pay is building a crypto to UPI payment layer, enabling users to spend crypto through UPI in just 3–5 seconds!

With 500M+ UPI users, this is exactly where real adoption can happen.

Thread below. 👇

"Chain abstraction is like wifi; you don't invent your own."

Hoskinson praised @NEARProtocol's team and confirmed he's been studying their intents framework and account model closely.

His comparison positions NEAR's standards work as foundational infrastructure that the rest of the industry should adopt.

He described a seven-layer architecture where intents sit on top, enabling users to interact across chains without managing the complexity underneath.

1/6 Every cycle has a new narrative that leads the market.

2021 was DeFi and NFTs. 2024 was memes and $SOL.

My big bet for 2027? AI + crypto with a side of privacy.

Here's why I put 2/3 of my port in $NEAR. 🧵 👇

$NEAR

NEAR: Blockchain’i Görünmez Hale Getiren AI Altyapısı

Marketcap: 1.79b$, FDV: 1.79b$

Blockchain’ler hızlandı.

Ucuzladı.

Ama yeni problem farklı:

AI geliyor, ve mevcut blockchain’ler buna hazır değil.

Çünkü AI:

Yüksek veri ister

Yüksek işlem gücü ister

Düşük gecikme ister

Klasik blockchain mimarisi bu yük için tasarlanmadı.

Problem Tanımı

Bugün:

AI sistemleri merkezi

Veri kontrolü birkaç şirkette

Kullanıcı sahipliği yok

Blockchain tarafında ise:

Veri işleme zayıf

Kullanıcı deneyimi karmaşık

AI + blockchain birleşemiyor

Çözüm

NEAR Protocol: Ölçeklenebilir Layer 1

Ama bu sefer odak farklı:

AI için altyapı

Veri işleme

Kullanıcı sahipliği

Chain abstraction

Teknik yapı

NEAR’ın mimarisi:

Sadece performans değil

AI uyumlu ölçek

Nightshade Sharding:

Paralel işlem

Yüksek throughput

AI veri yükü taşınabilir

Chain Abstraction (kritik):

Kullanıcı chain’i görmez

AI + uygulama arka planda çalışır

Web2 deneyimi

Web3 sahipliği

Veri & hesaplama altyapısı

NEAR; sadece finans değil, veri katmanı.

AI modelleri

Kullanıcı verisi

Daha verimli işlenebilir

Ekosistem (AI odaklı)

NEAR son dönemde, AI projelerine odaklandı.

AI agent yapıları

Veri sahipliği çözümleri

Kullanıcı kontrollü AI

Bu, Web3 AI anlatısının merkezine oturuyor.

Ekip & yatırım

Kurucular:

Illia Polosukhin

Alexander Skidanov

Kritik detay; Illia Polosukhin, Transformer (AI) paper’ının yazarlarından.

Yani, bu proje AI’ı sonradan eklemedi içinden geliyor.

Yatırımcılar

Andreessen Horowitz(a16z)

Tiger Global

Dragonfly

Fonlama: 600M$+

Değer; kullanım + AI entegrasyonu ile oluşacak.

Rekabet:

Solana

Ethereum

Fark:

NEAR, AI + kullanıcı deneyimi odaklı.

Benim yorumum:

AI + blockchain birleşiminin erken fiyatlanan altyapılarından biri olacak gibi görünüyor.

This is the cleanest bull case I've read on any L1 in months. Let me break down what actually happened to NEAR.

Token emissions: stopped. Completely. On February 23, 2026 NEAR flipped its fee switch and zeroed out new inflation. The same mechanism that every other L1 uses to paper over weak fundamentals - "don't worry, emissions will boost activity" - NEAR just turned off.

Revenue: $34M annualized. 96% of it comes from Intents doing $3B in monthly cross-chain volume. This isn't points programs or airdrop farming. 78% of that volume is stablecoins moving across 35 chains. Real economic activity, not speculators rotating in and out of meme tokens.

Supply: fully unlocked. No VC unlocks left. No team vesting cliff coming. The number of NEAR in circulation today is the number tomorrow. Every other L1 still has years of dilution ahead.

Market cap: $1.78B. Down 76% from highs. Trading like a dead project.

Daily fees: $1 a year ago. $80,000 today. That's five orders of magnitude of real usage growth while the price chart was going the other way.

ETF filings: Bitwise and Grayscale both filed for spot NEAR ETFs. Institutional access layer being built.

Here's what makes this different from every "undervalued L1" pitch. Most L1s with low market caps have one of three problems: bad fundamentals, massive unlock overhang, or inflation eating the holders alive. NEAR has none of them right now. The fundamentals are real and accelerating, the supply is clean, and inflation is literally zero.

The fee switch math is what nobody is paying attention to. At current revenue, NEAR is already net deflationary - more NEAR is being bought back and burned through Intents fees than is being issued. That flips a core L1 thesis: holders don't need to beat inflation because there is no inflation. They just need the revenue to keep growing.

The gap between "$34M revenue, zero inflation, fully unlocked, $3B/month volume across 35 chains" and "$1.78B market cap" is the mispricing. Either the revenue is fake and collapses, or it gets priced in. A year from now we'll know which.

Real-world asset tokenization is reshaping financial markets.

@CantonNetwork is one of the networks where this shift is already live: $8T in assets and $350B in daily volume.

RedStone provides the pricing infrastructure that enables institutional RWA to function at scale.

🚨 Wall Street just plugged into @CantonNetwork governance — all in the last week:

• Apollo Global Management ($938B+ AUM) named Super Validator (Weight 7) • Visa filed for Weight 10 Super Validator (max tier — same as DTCC & Broadridge) • Moody’s now operating a node + launched Token Integration Engine (first credit ratings agency on-chain)

Broadridge already at $362B/day repo. DTCC tokenized settlement live Q2. Private burns expanding.

The institutional flywheel is spinning. $CC scarcity incoming. Burn rate Crossed over 1.09 yesterday

Tokenization isn’t coming. It’s here. @CantonArmy

#CantonNetwork #RWA #Tokenization #CC

Featured App Update #5: Tokenomics group has approved @Cantex_io as a Featured App on @CantonNetwork 🎊

Cantex is an institutional grade, non-custodial trading platform built natively on Canton by the team at @CaviarNine

The platform combines an AMM DEX and a high throughput limit order book with atomic on-ledger settlement. Canton Coin is a core trading and quote asset across all pools and order books.

Privacy is core to how Cantex works. Only the parties involved in a trade see the details, and users can set their own counterparty preferences before execution.

AMM swapping is live on mainnet and the full order book and API suite are next.

Excited to see them drive real trading volume and liquidity on Canton!

🚨 APOLLO JOINS CANTON AS A SUPER VALIDATOR 🚨

@ApolloGlobal Management is joining Canton as a Super Validator, with a weight of 7, is a big deal for institutional tokenization.

Their $938B+ AUM (Dec 2025 figures, with $749B in credit alone and $1T+ target for 2026), $32B FY2025 revenue, 5,800+ employees, presence in 30+ countries, thousands of institutional clients/portfolio companies, and $228B record inflows position them to bring serious private credit and RWA volume on-chain.

Tokenized funds like ACRED (feeder to Apollo Diversified Credit) and ACRDX (~$51M AUM, stable $1.01 NAV via Anemoy/Centrifuge) are already live across chains/DeFi. Adding @CantonNetwork’s privacy-enabled rails means real potential for scaled on-chain credit, stablecoin yield, atomic settlements, and programmable RWAs with institutional-grade compliance and privacy.

Implications:

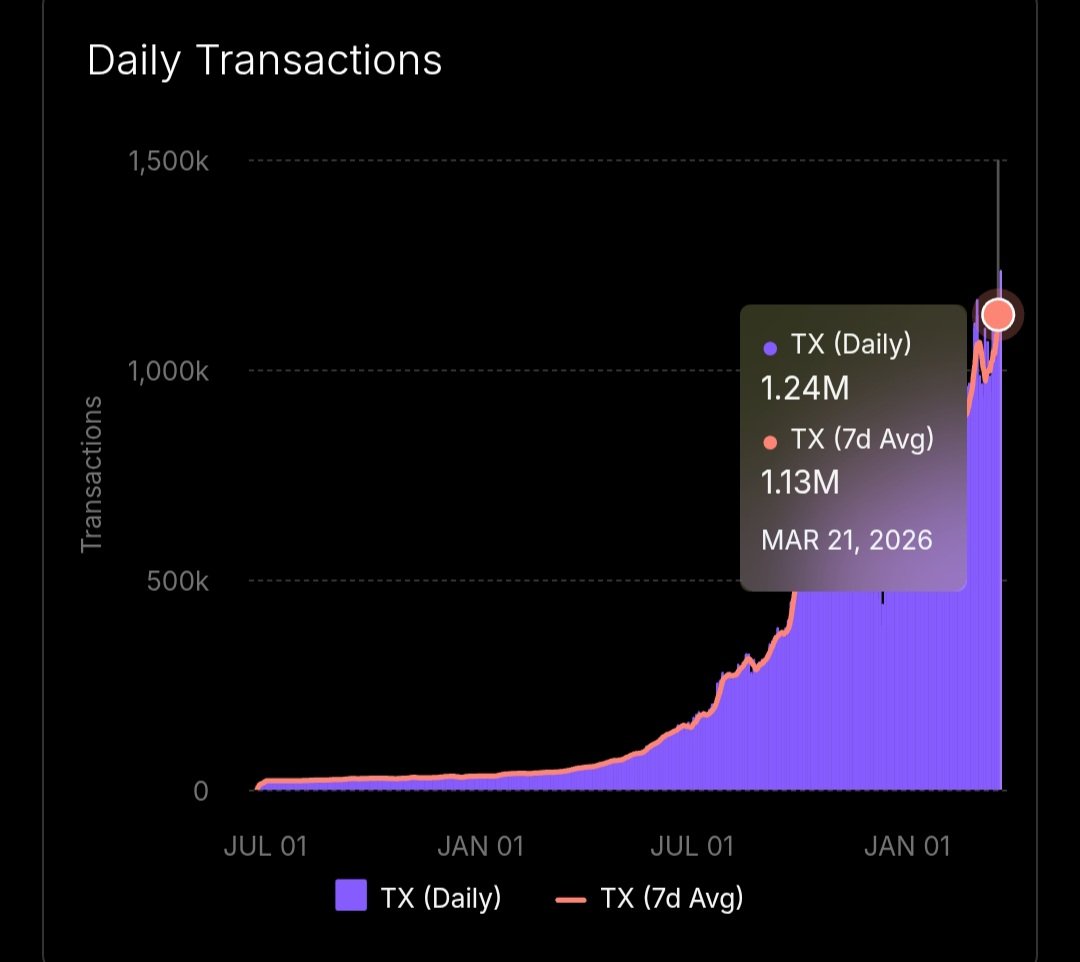

➜ Billions in tokenized private credit/structured products flowing through Canton’s Global Synchronizer (already at 700k+ daily txns, $9T+ monthly volume).

➜ Stronger network security/governance from a major player earning milestone-based CC rewards.

➜ Faster bridging of TradFi liquidity to onchain (think tokenized repo, cross-border collateral, reduced ops risk).

➜ Clear market signal that Canton is the go-to production infrastructure for serious institutions—building with DTCC, Nasdaq, LSEG, Euroclear, Goldman pilots, now Visa etc.

Christine Moy, @cmoyall, Partner and Head of Digital Assets, Data & AI Strategy at Apollo: “The killer use case for blockchain is being open architecture infrastructure where multiple different asset types can coexist and be programmable.”

That sounds like the type of global composability and scale @CantonNetwork has unlocked.

That sounds like @zenithfdn.

Zth.