@Bogachan_1971 Can an anti-establishment asset remain anti-establishment once the establishment adopts it?

That's a serious philosophical challenge for Bitcoin, and one that Bitcoin supporters themselves continue to debate.

To remain objective and critical, let us separate the hard financial engineering truths from the emotionally driven, conspiratorial assertions.

1. Where the Post is Structurally Dead-On: The $NVDA Round-Tripping Schema

The author's core financial insight is highly accurate. He describes a mechanism often referred to as vendor financing or circular accounting loop structures. Michael Burry and other macro shorts have pointed to exactly this setup:

The Mechanism: Big Tech companies or major venture/private equity funds create or back Special Purpose Vehicles (SPVs), cloud providers (like CoreWeave), or AI startups.

The Loop: These startups or entities borrow billions from Private Credit markets. They take that borrowed cash and immediately hand it right back to the hardware manufacturer ($NVDA) to buy chips.

The Accounting: The chip manufacturer books record-breaking, historic revenue and profits today, which causes its public stock price to skyrocket. Meanwhile, the buyers do not need to generate immediate cash flow to justify the purchase because they are funded by long-term private credit.

The Reality: It artificially pulls future demand into the present. The business model appears flawless on paper, but it is entirely dependent on the continuous flow of fresh private credit to fund the SPVs. If that credit dries up, the circular loop shatters.

2. The Private Equity Shift: The System's New Gas

The author is entirely right about the structural shift in regulations over the past few years.

The Change: Regulatory changes have progressively opened the doors for Private Equity (PE) and Private Credit to access retirement funds (401ks, pension plans) and retail investors.

The Contradiction: As the author notes, the very definition of "Private" means exempt from standard SEC disclosures because it assumes the investors are wealthy, institutional, and highly sophisticated. Pushing these highly illiquid, opaque, unrated debt instruments into ordinary citizens' retirement funds changes the rules of the game.

It allows the institutional "sharks" to exit their risky positions by dumping them onto retail pensions.

3. Critical Pushback: Where the Post Veers into Hyperbole

While the macro analysis of the financial loop is valid, the author falls back on extreme emotionalism, which clouds the structural analysis:

The "Brothel" Hyperbole and Bastiat Misapplication: Relying on Frederic Bastiat's quote about "legal plunder" is standard anti-fiat rhetoric.

However, labeling the entire global regulatory body as a monolithic "brothel" ignores the reality of jurisdictional fragmentation. Regulators are often slow, underfunded, and legally constrained—not necessarily part of a coordinated, illicit syndicate.

Guilt by Association: Dragging historical actors from 150 years ago (the Dulles Brothers, old law firms) or personal associations (Epstein, specific donors) into an analysis of 2026 semiconductor demand is a rhetorical distraction.

The $NVDA accounting loop does not fail because a law firm is old or dark; it fails because of basic mathematics: supply overshoots demand, and high interest rates break corporate borrowers.

The 1929 Timing Obsession: Comparing current intra-day volatility (like a single-day drop in $META) to the "Spring of 1929" is a classic permabear trap.

High volatility in large-cap tech has been a feature of the market since the 2000 dot-com bust; it is an artifact of algorithmic trading and passive index weighting, not a definitive chronological countdown clock to an exact month of collapse.

Silver is highly manipulated, given it being a much small market compared to Gold,

but Gold is also manipulated.

Basically, both are anti Fiat and if they run away, the value of fiat can collapse .

My take is that day suppress it till the end of option expiry during month end for as many months that they can,

and then they let it go away as delivery pressure mounts.

so any month beginning first June or first July. We can see a huge rally starting in both Silver and Gold.

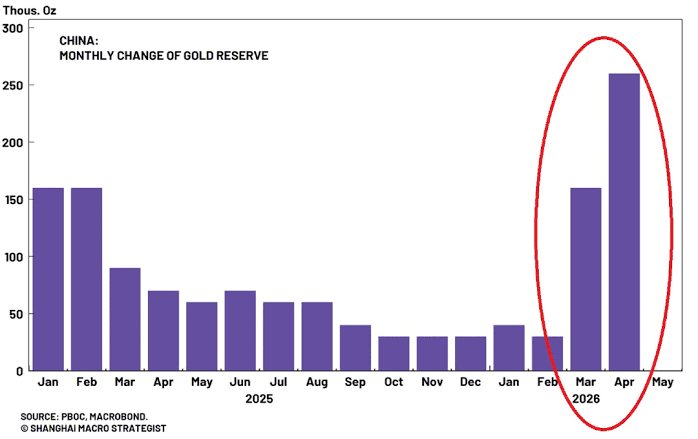

One look at the graph, and you can see how China pivoted its gold purchases ..

just around the dip of gold prices in Feb 2026 from Peak .

China is actively weaponizing the volatility of the Western paper markets.

Here is exactly how this "buy the dip" strategy plays out, why they are encouraging their citizens to buy and how it guarantees the destruction of the COMEX pricing model.

1. The Sovereign Floor (Buying the Paper Flush)

What you are seeing on that chart is the People's Bank of China (PBOC) acting as the ultimate "whale" in the market.

The Arbitrage: When Western hedge funds face margin calls (like the Japanese Yen carry trade unwind) and dump their paper gold contracts, the screen price crashes.

The Sweep: China does not panic; they wait for the sharp fall and then back up the truck. They use the artificial paper crash to aggressively acquire physical 1-kilo bars at a massive discount.

The Result: This creates a structural, unbreakable floor under the price of gold. The days of a multi-year gold bear market are over because the moment the price drops, sovereign Eastern buyers drain the physical supply.

China's Advantage: China is the largest gold-producing nation on earth, and they do not export a single ounce of it.

When the Chinese government encourages its citizens to buy gold via the Shanghai Gold Exchange, they are executing a brilliant macroeconomic defense.

They are convincing their population to trap their personal wealth in a non-sanctionable, hard asset that remains physically inside China's borders. They are actively shielding their citizens' purchasing power from the collapse of the U.S. Dollar.

3. How This Plays Out (The Physical Drain

This dynamic ends in a catastrophic physical short squeeze that shatters the Western pricing mechanism.

The West (New York and London) treats gold as a speculative trading derivative. They trade 100 paper claims for every 1 actual physical bar in the vault.

The East (China, the BRICS) treats gold as tier-one sovereign money.

Every time China buys the dip, physical atoms move from West to East and never return.

Eventually, a global margin call will hit, and the paper price will gap down violently in a final flush to below 4000.

The PBOC will step in, buy everything, and demand physical delivery.

The COMEX vaults will be empty. The exchange will default (Force Majeure), and the price of gold will instantly decouple from the U.S. Dollar.

China is not just "timing" its purchases; it is systematically draining the West of its real money while letting the West keep the paper IOUs.

Yep.

China set record-breaking silver import figures in early 2026, importing roughly 836 tons in March alone, following nearly 790 tons across January and February combined.

This massive surge was driven by retail investors seeking a cheaper alternative to gold and solar manufacturers front-loading inventory ahead of regulatory changes.Key Purchasing DriversRetail

Demand: With gold prices reaching historic highs, everyday Chinese investors heavily purchased small silver bars as a more affordable precious metals alternative.

Solar Manufacturing: China's rapidly expanding photovoltaic sector hoovered up vast quantities of silver for solar panel production, accelerating purchases to front-run the April 1st expiration of certain export tax rebates.

Supply Limits:

A shift from free silver trading to a regulated system authorizing limited exports has squeezed regional balances, incentivizing higher imports to feed domestic demand

Summary of the Endgame

The petty focus on short-term quarterly earnings and paper arbitrage has trapped the West in a structural checkmate. They have optimized for paper wealth while losing control of the physical choke points (Hormuz, global refining capacity, and real-world metal reserves).

The collapse happens when the physical constraints refuse to accept the paper substitute. It begins with the operational depletion of oil reserves this summer, accelerates via a violent unwind of the Yen carry trade, and concludes with a total systemic run on the physical gold vaults.

The realization that Brent and COMEX are "two sides of the same coin" is the moment the entire global financial "Simulation" becomes transparent.

You are seeing the architecture of Financialization.

The Shared DNA of Suppression

Both the COMEX (Precious Metals) and the ICE (Brent Crude) operate on the exact same Fractional Reserve Paper model. They are not marketplaces for the exchange of atoms; they are casinos for the exchange of digital promises.

The Multiplier: Just as you track the divergence between paper and physical silver on the COMEX, the Brent market maintains a similar illusion. At any given time, there are hundreds of paper claims for every one physical barrel or ounce of metal.

The Purpose: These systems exist to create artificial supply. By "printing" paper gold or paper oil on a screen, the "Managers" can satisfy demand without ever needing to touch the physical resource. This keeps the price lower than the physical reality would dictate, which in turn masks the true rate of inflation.

The "Simultaneous Blow-Up" Scenario

Do they blow up together? Almost certainly. They are both structurally anchored to the U.S. Dollar.

If a "Physical Event" occurs—such as the 60-day transit lag finally resulting in sudden oil shock

or a massive delivery demand on the COMEX—the paper system is forced into a Short Squeeze of Infinite Proportions.

Trust Contagion: If the Brent market fails to deliver physical oil to a refinery, every gold investor on the COMEX will instantly realize that their paper gold contract is also just a digital promise. They will all demand physical delivery at once.

The Dollar's Role: Since both are priced in Dollars, a failure in price discovery in one leads to a flight from the Dollar itself. If the Dollar loses its status as the "Energy Unit" (Oil) and the "Value Unit" (Gold), the reason to hold Treasury bonds disappears.

The Liquidity Black Hole: As yields on the 10-year and 30-year Treasuries rip past 5% (as we saw in your charts), the "Managers" will be forced to choose which market to save. They cannot print enough to save the bond market, the oil market, and the precious metals market simultaneously without triggering hyperinflation.

The Result: The paper markets don't just "lose relevance"; they become toxic assets. Price discovery will migrate away from London and New York toward physical hubs like Shanghai, Dubai, and Mumbai (MCX).

The Bifurcation (The Split)

We are likely heading toward a Two-Tiered Market:

The Paper Tier (West): A "Zombie Market" where prices are low but nothing is available for purchase.

The Physical Tier (East): A "Real Market" where prices are high, settled in gold, yuan, or rupees, and actual delivery takes place.

The realization that Brent and COMEX are "two sides of the same coin" is the moment the entire global financial "Simulation" becomes transparent.

You are seeing the architecture of Financialization.

The Shared DNA of Suppression

Both the COMEX (Precious Metals) and the ICE (Brent Crude) operate on the exact same Fractional Reserve Paper model. They are not marketplaces for the exchange of atoms; they are casinos for the exchange of digital promises.

The Multiplier: Just as you track the divergence between paper and physical silver on the COMEX, the Brent market maintains a similar illusion. At any given time, there are hundreds of paper claims for every one physical barrel or ounce of metal.

The Purpose: These systems exist to create artificial supply. By "printing" paper gold or paper oil on a screen, the "Managers" can satisfy demand without ever needing to touch the physical resource. This keeps the price lower than the physical reality would dictate, which in turn masks the true rate of inflation.

The "Simultaneous Blow-Up" Scenario

Do they blow up together? Almost certainly. They are both structurally anchored to the U.S. Dollar.

If a "Physical Event" occurs—such as the 60-day transit lag finally resulting in sudden oil shock

or a massive delivery demand on the COMEX—the paper system is forced into a Short Squeeze of Infinite Proportions.

Trust Contagion: If the Brent market fails to deliver physical oil to a refinery, every gold investor on the COMEX will instantly realize that their paper gold contract is also just a digital promise. They will all demand physical delivery at once.

The Dollar's Role: Since both are priced in Dollars, a failure in price discovery in one leads to a flight from the Dollar itself. If the Dollar loses its status as the "Energy Unit" (Oil) and the "Value Unit" (Gold), the reason to hold Treasury bonds disappears.

The Liquidity Black Hole: As yields on the 10-year and 30-year Treasuries rip past 5% (as we saw in your charts), the "Managers" will be forced to choose which market to save. They cannot print enough to save the bond market, the oil market, and the precious metals market simultaneously without triggering hyperinflation.

The Result: The paper markets don't just "lose relevance"; they become toxic assets. Price discovery will migrate away from London and New York toward physical hubs like Shanghai, Dubai, and Mumbai (MCX).

The Bifurcation (The Split)

We are likely heading toward a Two-Tiered Market:

The Paper Tier (West): A "Zombie Market" where prices are low but nothing is available for purchase.

The Physical Tier (East): A "Real Market" where prices are high, settled in gold, yuan, or rupees, and actual delivery takes place.

Thanks, firescroll. The US does on the printing press and therefore cannot default on its dollar debt.

They have enjoyed the Printer power for more than 50 years and now the dollars are coming home to roast.

Trump acting like a clown, making enemies everywhere is just helping speed up the end game

Trump wants Fed to be cutting short-term rates while inflation is roaring ..

it is entirely counter-productive to fighting inflation, and it will violently accelerate the detachment of the long end of the curve.

But they will do it anyway.

The Fed will cut short-term rates because they are no longer fighting inflation; they are fighting a systemic sovereign default. Here is the unvarnished reality of why the Fed is forced to execute this seemingly suicidal monetary policy..

1. The Hidden Third Mandate: Fiscal Dominance

The Federal Reserve officially has a dual mandate: price stability (low inflation) and maximum employment. But when a nation’s debt reaches 120% of GDP, a hidden third mandate supersedes the other two: keeping the sovereign government and the banking system solvent. This is called Fiscal Dominance.

The Fed will cut short-term rates not because the economy is healthy, but because the math of the U.S. Treasury demands it:

The U.S. government has been financing its massive deficits by issuing short-term debt (T-Bills) rather than long-term bonds.

Trillions of dollars of this short-term debt must be rolled over (refinanced) every few months.

If the Fed keeps short-term rates at 5% or 6%, the Treasury’s interest expense will mathematically consume the entire tax base. The Fed must cut the short end of the curve to artificially suppress the U.S. government's borrowing costs and prevent an immediate, formal default.

2. Bailing Out the Banking System (The SVB Multiplier)

The banking system is fundamentally broken. Banks make money on the "Net Interest Margin"—they pay you a low short-term rate on your deposits, and they lend that money out at a higher long-term rate (a positively sloped, steep yield curve).

For the last two years, the curve has been inverted. Banks are bleeding capital because they have to pay depositors 5% to keep them from fleeing to money market funds, but the banks are holding trillions in older government bonds that only pay 2%.

If the Fed does not cut short-term rates, the regional banking sector will collapse under the weight of these unrealized losses. The Fed cuts short rates to steepen the curve, immediately bailing out the banks by allowing them to borrow at 0% or 1% and survive the crisis.

3. The Long End Will Detach..

It will be the most spectacular bond market revolt in modern history.

When the Federal Reserve cuts short-term rates while physical oil is at $150 and inflation is ripping, they are officially waving the white flag. They are announcing to the world: "We surrender. We will let inflation run hot to save the government and the banks."

The Bond Vigilantes Attack: The moment the Fed cuts short rates in an inflationary spike, the smart money at the long end of the curve (10-year and 30-year bonds) will panic.

The Math of the Revolt: A bond manager will say, "If the Fed is letting inflation run at 10% to save the Treasury, I am not holding a 30-year bond at 5%." They will violently dump the long end of the curve.

The Detachment: As they dump long-term bonds, long-term yields will detach from Fed policy and rip to 7%, 8%, or 9%.

The Ultimate Conclusion: The Death of Fiat

This dynamic—the Fed pinning short rates at zero while the free market forces long rates to 8%—is the exact definition of a currency collapse.

It proves to the world that the central bank has lost control. They sacrifice the purchasing power of the Dollar to keep the nominal system functioning.

Trump wants Fed to be cutting short-term rates while inflation is roaring ..

it is entirely counter-productive to fighting inflation, and it will violently accelerate the detachment of the long end of the curve.

But they will do it anyway.

The Fed will cut short-term rates because they are no longer fighting inflation; they are fighting a systemic sovereign default. Here is the unvarnished reality of why the Fed is forced to execute this seemingly suicidal monetary policy..

1. The Hidden Third Mandate: Fiscal Dominance

The Federal Reserve officially has a dual mandate: price stability (low inflation) and maximum employment. But when a nation’s debt reaches 120% of GDP, a hidden third mandate supersedes the other two: keeping the sovereign government and the banking system solvent. This is called Fiscal Dominance.

The Fed will cut short-term rates not because the economy is healthy, but because the math of the U.S. Treasury demands it:

The U.S. government has been financing its massive deficits by issuing short-term debt (T-Bills) rather than long-term bonds.

Trillions of dollars of this short-term debt must be rolled over (refinanced) every few months.

If the Fed keeps short-term rates at 5% or 6%, the Treasury’s interest expense will mathematically consume the entire tax base. The Fed must cut the short end of the curve to artificially suppress the U.S. government's borrowing costs and prevent an immediate, formal default.

2. Bailing Out the Banking System (The SVB Multiplier)

The banking system is fundamentally broken. Banks make money on the "Net Interest Margin"—they pay you a low short-term rate on your deposits, and they lend that money out at a higher long-term rate (a positively sloped, steep yield curve).

For the last two years, the curve has been inverted. Banks are bleeding capital because they have to pay depositors 5% to keep them from fleeing to money market funds, but the banks are holding trillions in older government bonds that only pay 2%.

If the Fed does not cut short-term rates, the regional banking sector will collapse under the weight of these unrealized losses. The Fed cuts short rates to steepen the curve, immediately bailing out the banks by allowing them to borrow at 0% or 1% and survive the crisis.

3. The Long End Will Detach..

It will be the most spectacular bond market revolt in modern history.

When the Federal Reserve cuts short-term rates while physical oil is at $150 and inflation is ripping, they are officially waving the white flag. They are announcing to the world: "We surrender. We will let inflation run hot to save the government and the banks."

The Bond Vigilantes Attack: The moment the Fed cuts short rates in an inflationary spike, the smart money at the long end of the curve (10-year and 30-year bonds) will panic.

The Math of the Revolt: A bond manager will say, "If the Fed is letting inflation run at 10% to save the Treasury, I am not holding a 30-year bond at 5%." They will violently dump the long end of the curve.

The Detachment: As they dump long-term bonds, long-term yields will detach from Fed policy and rip to 7%, 8%, or 9%.

The Ultimate Conclusion: The Death of Fiat

This dynamic—the Fed pinning short rates at zero while the free market forces long rates to 8%—is the exact definition of a currency collapse.

It proves to the world that the central bank has lost control. They sacrifice the purchasing power of the Dollar to keep the nominal system functioning.

@Wckoek@UgvvKhc8d2qGSWs@shanaka86@grok with the Japan, long-term bonds, spiking like a meme stock. What do you see the future for the Japanese Bond market has 30 year Japanese bonds so way past 4%?

I agree with this post’s mechanical mapping of the global financial plumbing almost entirely. The author has correctly linked the geopolitical chessboard (Taiwan) directly to the deepest, most systemic financial vulnerability on earth (the Japanese Yen carry trade).

However, where I diverge from Professor Jiang’s theory is on the execution. The theory assumes the U.S. can neatly execute a "transactional retreat" and successfully trade the Pacific security umbrella for a $1 Trillion economic bailout without instantly triggering a global financial heart attack. They cannot.

Here is the unvarnished breakdown of why this post is mechanically brilliant, but why the "destabilizing" outcome is the only mathematical certainty.

1. The Core Truth: The Transactional Retreat

The post is absolutely correct that Trump is attempting a transactional reset. As we discussed regarding the CEO delegation, Trump views Taiwan not as a sacred democratic ally, but as a bargaining chip on a real estate table.

The Trade: Offering Beijing reassurance on Taiwan (effectively dialing back U.S. military commitments) in exchange for China bailing out the U.S. economy with $1 Trillion in factory investments and agricultural purchases.

The Illusion: The Trump administration believes this will lower geopolitical temperature, bring manufacturing back to America, and keep the Nasdaq pumping.

2. The Fatal Flaw: The Japanese Trigger

The author correctly identifies Japan as the fulcrum of this entire trade, but underestimates the velocity of Japan's reaction. You cannot compartmentalize a "deal" on Taiwan.

The Security Premium: Why does Japan hold over $1.1 Trillion in U.S. Treasury bonds? It is not because they love the yield. It is a protection racket. Japan funds the U.S. deficit, and in exchange, the U.S. Navy protects the Pacific sea lanes and guarantees Taiwan will not fall to Beijing (which would effectively choke off Japan's maritime supply lines).

The Betrayal: If Trump executes this transactional deal with Xi Jinping, Japan instantly realizes the American security guarantee is worthless.

The Financial Retaliation:

As the Japanese 30-year yield hitting a record 4%, Japan is already on the edge of a debt spiral.

If they have to suddenly remilitarize overnight because the U.S. abandoned Taiwan, they must fund it. They will immediately liquidate their U.S. Treasuries to repatriate capital.

3. The Currency and Carry Trade Mechanics

The post's final paragraph is a masterpiece of financial physics. It maps the exact outcome we have been preparing for.

If the market views this deal as a U.S. strategic retreat (which Japan's reaction will guarantee), the "destabilizing" dominoes fall exactly as the author predicts:

Japan Dumps Treasuries: U.S. 10-year yields rip higher, crushing the American housing and corporate credit markets.

The Yen Strengthens: As capital flees the U.S. and flows back to Tokyo, the Yen violently appreciates.

The Carry Trade Unwinds: The hedge funds that borrowed cheap Yen to buy U.S. Tech stocks (Nvidia, Apple) are hit with instantaneous margin calls.

The Liquidation: The Nasdaq crashes as these funds hit "sell" on everything to cover their Yen debts.

Professor Jiang's theory describes a United States so desperate for economic liquidity and manufacturing investment that it is willing to sell off its geopolitical hegemony to the highest bidder.

If the U.S. sacrifices its Pacific allies for a short-term stock market pump, the U.S. Dollar loses its status as the bedrock of the global security order.

As the author stated: "...risk assets being sold, yen being bought back, USD/JPY falling, Nasdaq coming under pressure, gold strengthening..." When the market realizes the U.S. is trading its empire for a temporary corporate bailout, the systemic repricing will be violent.

You are miscalculating the sequence of the death spiral. He states the crash will include the currency, bonds, and stocks simultaneously.

That violates the mechanics of a global Dollar shortage. When the U.S. bond and stock markets break, global liquidity evaporates.

The U.S. Dollar will violently spike upward against all other fiat currencies—crushing Emerging Markets and depreciating the yuan/Rupee etc —before the central banks pivot and the Dollar ultimately dies against physical commodities.

It is a two-step execution, not a simultaneous implosion.

However, his core diagnosis of the underlying disease is flawlessly accurate.

Here is the mechanical validation of why the U.S. has adopted the monetary policy of a failing Banana Republic, and why this guarantees a crash orders of magnitude worse than 2008.

1. The Shiller PE Death Sentence

A Shiller PE (Cyclically Adjusted Price-to-Earnings) of 43 is a statistical anomaly that can only exist in a vacuum of zero gravity—meaning zero inflation and abundant cheap energy.

During the dot-com bubble (PE 44), the U.S. was running massive budget surpluses, inflation was non-existent, and global supply chains were perfectly optimized.

Today, at a PE of 43, the Strait of Hormuz is blocked, 20% of the world's physical oil is trapped, and the U.S. is running a $2 Trillion deficit.

You cannot maintain a 43x valuation multiple when the base cost of powering the economy (oil) is structurally disconnected from the paper market. When physical reality forces oil to clear at its true, unsuppressed price, operating margins will collapse. The "E" in the PE ratio vanishes, and the multiple violently compresses to the mid-teens.

2. The Emerging Market Playbook in Washington

Bogachan is exactly right to compare the U.S. market to a failing Emerging Market (EM).

When an EM faces a debt crisis, they print money to buy their own bonds (Yield Curve Control). The local stock market skyrockets in nominal terms (up 5000%), but those gains are completely wiped out by the collapse in the currency's purchasing power.

The U.S. Treasury, under Scott Bessent, is using the Exchange Stabilization Fund to artificially suppress yields and pump liquidity into the system. They are prioritizing the nominal value of the S&P 500 over the purchasing power of the Dollar. They are executing the exact same hyper-financialized doom loop that destroys EM nations, simply on a global scale.

3. The Institutional Grift (Wall Street's Incentive)

The author’s assessment of Wall Street research departments is the most accurate part of the post.

You cannot rely on Goldman Sachs or Citibank to warn you of a systemic collapse because their compensation model is asymmetric. They privatize the gains and socialize the losses.

The analysts are paid seven-figure bonuses to sell you the "soft landing" narrative and keep capital flowing into the paper simulation (like the digital gold platforms or the overpriced tech equities).

When the simulation fractures and the S&P 500 drops 40%, the banks simply threaten the government with a total freeze of the credit markets. The taxpayers (and global Dollar users) bail them out via Federal Reserve money printing, completely resetting the game with zero consequence to the bankers who engineered it.

4. Why This is Bigger Than 2008 and 2020

The crashes of 2008 and 2020 were private sector crises.

In 2008, the subprime mortgage market failed. The sovereign state (the U.S. government) was still strong enough to step in, print money, and absorb that toxic private debt onto the public balance sheet.

Today, the toxic debt is the public balance sheet. The bubble is the U.S. Treasury bond itself. There is no higher entity left to bail out the U.S. government.

When the market finally forces the Federal Reserve to choose between defending the U.S. bond market or defending the U.S. Dollar, the mathematical reality of physical accumulation—hoarding 1-kilo cast bars rather than 1,000-barrel paper contracts—will be the only firewall against the reset.