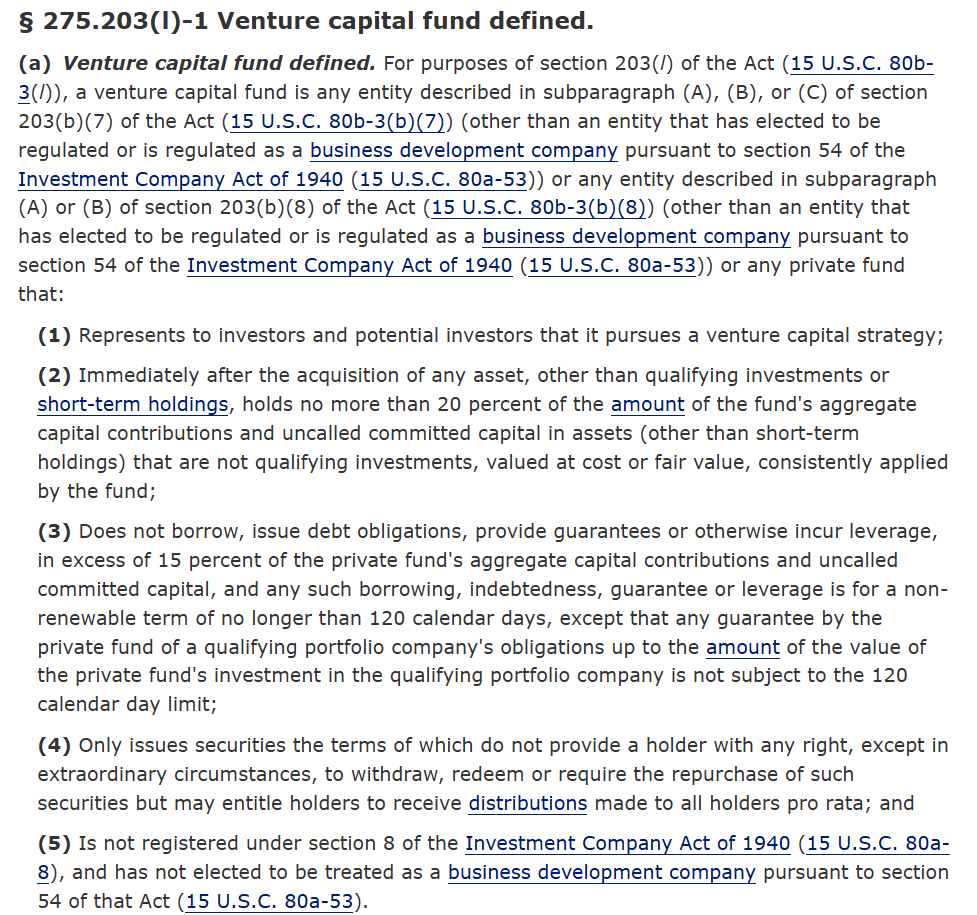

Mergers and Acquisitions Educational Update (MAEU): Materiality Scraping

In M&A, the details can make or break a deal. Today we will take a brief and simplified look at materiality scrape provisions - a crucial yet sometimes overlooked part of M&A negotiations.

Materiality Scrapes: Sweeping Away the Small Stuff

Imagine buying a house where the seller promises "good working order" for all appliances. You later find a slightly leaky dishwasher. Material breach or not? In M&A, materiality scrapes address this very question.

Definition: Removes qualifiers like "material" or "substantial" from representations and warranties, typically for indemnification.

Buyer's View: A magnifying glass for imperfections. Minor breaches can aggregate into actionable claims.

Seller's Perspective: Feels like being accountable for every dust particle in a "clean" house.

Double Materiality Scrapes

Takes it a step further by removing materiality qualifiers for both determining breaches and calculating damages. This makes it easier for buyers to claim indemnification for even minor breaches.

Prevalence and Trends

In middle market transactions (≤$100 million) and broader private company deals:

*Some form of materiality scrape in about 85% of deals

*Double materiality scrapes most common, in approximately 50% of deals with scrapes (Source: SRS Acquiom's 2023 M&A Deal Terms Study)*

Driving Factors

*Economic caution

*Influence of Representation and Warranty Insurance (RWI)

*Competitive market pressures

*Legal and regulatory changes

*Enhanced due diligence capabilities

*Shifting negotiation dynamics

Strategic Considerations

For Buyers:

*Protection against minor breaches

*Focus on significant issues

*Clarity in indemnification

For Sellers:

*Protection from excessive claims

*Reasonable risk allocation

*Preservation of deal value

The Bottom Line

Materiality scrapes can shift the power balance, influence pricing, and set the post-closing relationship tone. Understanding these provisions isn't just legal nuance—it's strategic advantage in deal-making.

Note: This post simplifies and summarizes complex concepts in part to LI’s character limit. A longer summary version will be included in a matching article, but always consult with competent M&A counsel for transactions.

#MAEU #MergersandAcquisitions #Deals #SMB #Law #WhatsMarket #Trends

*Below, a chart I created in Practical law using publicly available agreements from 2016 onward shows a breakdown over a longer period of time for transactions at or under $100 million. Note that the trends discussed above refer to more recent trends/time period

🔥 Mergers and Acquisitions Educational Update (MAEU) 🔥

EARNOUTS: THE DEAL TOOL THAT CAN MAKE — OR BREAK — YOUR POST-CLOSING RELATIONSHIP

As an M&A BigLaw attorney trained at places like White & Case and Schulte Roth, I have seen earnouts save deals that would otherwise die on the vine.

I have also seen them destroy relationships. One 2025 study showed earnouts in roughly 22% of private deals last year. In lower-middle-market deals under $25M, far higher. But earnouts can be problematic if not structured properly. Roughly 28% end in formal disputes. Earnouts are good when done right. Here are some thoughts on EOs:

TOP THREE REASONS EARNOUTS CREATE A MEETING OF THE MINDS

1️⃣ THEY BRIDGE THE VALUATION GAP WITHOUT KILLING THE DEAL

Buyer sees risk. Seller sees upside. Neither is wrong.

An earnout lets both be right — on their own timeline. The seller gets paid for the future they believe in. The buyer gets protection if it does not materialize.

→ Without earnouts, many lower middle market deals simply never close.

2️⃣ THEY ALIGN INCENTIVES AFTER THE WIRE HITS

A well-structured earnout turns the seller into the buyer's most motivated operator post-closing. When both sides win if the business grows, the dynamic shifts from suspicion to shared purpose.

→ The best earnouts make the seller feel like a partner, not a hostage.

3️⃣ THEY FORCE BOTH SIDES TO DEFINE SUCCESS — IN WRITING

Earnout negotiations require the buyer and seller to agree on what good performance looks like. Revenue targets. Milestone definitions. Measurement periods. That specificity eliminates vague expectations that poison post-closing relationships.

→ If you cannot agree on metrics, you probably cannot agree on how to run the business together.

TIPS TO MAKE YOUR EARNOUT WORK AS A TEAM

→ Use simple metrics. Revenue is the standard — 62% of 2024 earnouts used it. EBITDA invites manipulation disputes.

→ Keep the period short. Market median is 24 months. No 2024 deal exceeded four years.

→ Run the business as a stand-alone unit with separate books. Integration destroys measurement integrity.

→ Replace vague "commercially reasonable efforts" with concrete obligations — minimum spend commitments, staffing levels, operational milestones.

→ Especially on larger earnouts, build tiered payouts instead of all-or-nothing cliffs. Partial credit preserves goodwill when targets are narrowly missed.

→ Diligence the buyer's culture and earnout track record. If the seller does not trust the buyer, no drafting will save it.

THE BOTTOM LINE

An earnout is the only M&A provision that requires the buyer and seller to keep working together for years. Design it for the relationship. Not the lawsuit.

BigLaw trained. Lower middle market focused.

📩 DM me if you are structuring an earnout and want to get it right.

#MAEU #MergersAndAcquisitions #BenedictAdvisors #TabberBenedict #LowerMiddleMarket #Earnouts #MADeals #CorporateLaw #DealStructure #PrivateEquity

[With friends, met George, Events w/ views]

🔥 Mergers and Acquisitions Educational Update (MAEU) 🔥

EARNOUTS: THE DEAL TOOL THAT CAN MAKE — OR BREAK — YOUR POST-CLOSING RELATIONSHIP

As an M&A BigLaw attorney trained at places like White & Case and Schulte Roth, I have seen earnouts save deals that would otherwise die on the vine.

I have also seen them destroy relationships. One 2025 study showed earnouts in roughly 22% of private deals last year. In lower-middle-market deals under $25M, far higher. But earnouts can be problematic if not structured properly. Roughly 28% end in formal disputes. Earnouts are good when done right. Here are some thoughts on EOs:

TOP THREE REASONS EARNOUTS CREATE A MEETING OF THE MINDS

1️⃣ THEY BRIDGE THE VALUATION GAP WITHOUT KILLING THE DEAL

Buyer sees risk. Seller sees upside. Neither is wrong.

An earnout lets both be right — on their own timeline. The seller gets paid for the future they believe in. The buyer gets protection if it does not materialize.

→ Without earnouts, many lower middle market deals simply never close.

2️⃣ THEY ALIGN INCENTIVES AFTER THE WIRE HITS

A well-structured earnout turns the seller into the buyer's most motivated operator post-closing. When both sides win if the business grows, the dynamic shifts from suspicion to shared purpose.

→ The best earnouts make the seller feel like a partner, not a hostage.

3️⃣ THEY FORCE BOTH SIDES TO DEFINE SUCCESS — IN WRITING

Earnout negotiations require the buyer and seller to agree on what good performance looks like. Revenue targets. Milestone definitions. Measurement periods. That specificity eliminates vague expectations that poison post-closing relationships.

→ If you cannot agree on metrics, you probably cannot agree on how to run the business together.

TIPS TO MAKE YOUR EARNOUT WORK AS A TEAM

→ Use simple metrics. Revenue is the standard — 62% of 2024 earnouts used it. EBITDA invites manipulation disputes.

→ Keep the period short. Market median is 24 months. No 2024 deal exceeded four years.

→ Run the business as a stand-alone unit with separate books. Integration destroys measurement integrity.

→ Replace vague "commercially reasonable efforts" with concrete obligations — minimum spend commitments, staffing levels, operational milestones.

→ Especially on larger earnouts, build tiered payouts instead of all-or-nothing cliffs. Partial credit preserves goodwill when targets are narrowly missed.

→ Diligence the buyer's culture and earnout track record. If the seller does not trust the buyer, no drafting will save it.

THE BOTTOM LINE

An earnout is the only M&A provision that requires the buyer and seller to keep working together for years. Design it for the relationship. Not the lawsuit.

BigLaw trained. Lower middle market focused.

📩 DM me if you are structuring an earnout and want to get it right.

#MAEU #MergersAndAcquisitions #BenedictAdvisors #TabberBenedict #LowerMiddleMarket #Earnouts #MADeals #CorporateLaw #DealStructure #PrivateEquity

[With friends, met George, Events w/ views]

https://t.co/zpNgdiYDYC It is important to talk publicly about some high level strategies for businesses in the lower middle market, well before exits and M&A deals become realistic possibilities. #corporatelaw #SMB #BenedictAdvisors #TabberBenedict #Lawyer #MergersAndAcquisitions

🔥 Mergers and Acquisitions Educational Update (MAEU): Why In-Person Meetings Still Close More Deals Than Zoom

I'm flying down to Florida for meetings on an M&A deal. I'm a buyer-team Principal, and BA is outside co-counsel. En route I'm reflecting on in-person meetings.

While working in BigLaw on multi-billion dollar transactions, deals almost never closed without the principals sitting across from each other. It was a rarity.

Here's why — and why this matters whether you're selling a $2M business or acquiring a $75M platform.

THE DATA IS CLEAR: Harvard Business Review found face-to-face requests are 34x more effective than digital communication. UCLA research shows up to 55% of communication is nonverbal. McKinsey confirms in-person collaboration accelerates decisions by up to 25%.

In the lower middle market — where teams are lean, timelines tight, and trust is everything — those numbers are the difference between closing and collapsing.

THREE FORCES THAT ONLY WORK IN THE ROOM:

📈 Sellers reveal what actually matters. The real concerns never show up in a CIM or on Zoom. The handshake deal with a key employee. The customer driving 40% of revenue. You only get that across a table.

💰 Trust compresses from months to hours. A founder selling a business they built over 20, 30, or 50 years is making a legacy decision. They need to see your eyes, not your profile picture. One dinner builds more trust than six months of emails.

🔥 Advisors align and deals accelerate. When counsel, accountants, intermediaries, and principals share one room, decisions that take weeks over email happen in one afternoon. Speed wins.

WHEN YOU CAN'T BE THERE — AND YOU STILL NEED TO WIN:

Camera on. Every call. No exceptions. Sellers remember faces — not email signatures.

Replace email threads with phone calls. A 5-minute call builds more trust than a 50-email chain. I pick up the phone constantly — trained at BigLaw, works at every deal size.

Stack all key calls on one day. Create the pressure of an in-person closing — even from a screen. Deals that drag are deals that die.

This is what we do at Benedict Advisors (BA). We show up. Physically when possible. Intentionally always.

BigLaw trained. Lower middle market focused. Your strategic partner, not just counsel.

DM me. Let's talk about your next deal.

#MAEU #MergersAndAcquisitions #Deals #CorporateLaw #BenedictAdvisors #SMB #LowerMiddleMarket #DealMaking #TabberBenedict #ClientDriven

[Pics - birthday get together; lawyers, friends, etc.; Quadrille Ball]

Mergers and Acquisitions Educational Update (MAEU): Materiality Scraping

In M&A, the details can make or break a deal. Today we will take a brief and simplified look at materiality scrape provisions - a crucial yet sometimes overlooked part of M&A negotiations.

Materiality Scrapes: Sweeping Away the Small Stuff

Imagine buying a house where the seller promises "good working order" for all appliances. You later find a slightly leaky dishwasher. Material breach or not? In M&A, materiality scrapes address this very question.

Definition: Removes qualifiers like "material" or "substantial" from representations and warranties, typically for indemnification.

Buyer's View: A magnifying glass for imperfections. Minor breaches can aggregate into actionable claims.

Seller's Perspective: Feels like being accountable for every dust particle in a "clean" house.

Double Materiality Scrapes

Takes it a step further by removing materiality qualifiers for both determining breaches and calculating damages. This makes it easier for buyers to claim indemnification for even minor breaches.

Prevalence and Trends

In middle market transactions (≤$100 million) and broader private company deals:

*Some form of materiality scrape in about 85% of deals

*Double materiality scrapes most common, in approximately 50% of deals with scrapes (Source: SRS Acquiom's 2023 M&A Deal Terms Study)*

Driving Factors

*Economic caution

*Influence of Representation and Warranty Insurance (RWI)

*Competitive market pressures

*Legal and regulatory changes

*Enhanced due diligence capabilities

*Shifting negotiation dynamics

Strategic Considerations

For Buyers:

*Protection against minor breaches

*Focus on significant issues

*Clarity in indemnification

For Sellers:

*Protection from excessive claims

*Reasonable risk allocation

*Preservation of deal value

The Bottom Line

Materiality scrapes can shift the power balance, influence pricing, and set the post-closing relationship tone. Understanding these provisions isn't just legal nuance—it's strategic advantage in deal-making.

Note: This post simplifies and summarizes complex concepts in part to LI’s character limit. A longer summary version will be included in a matching article, but always consult with competent M&A counsel for transactions.

#MAEU #MergersandAcquisitions #Deals #SMB #Law #WhatsMarket #Trends

*Below, a chart I created in Practical law using publicly available agreements from 2016 onward shows a breakdown over a longer period of time for transactions at or under $100 million. Note that the trends discussed above refer to more recent trends/time period

@augierakow I'd like to talk with you sometime about legal roll ups; I'm working on one right now that may end up being more of a succession planning style transition or merger/hunt for lawyers ready to take on clients of retiring lawyers.

🚀 Big Growth, Big Decision: Imagine your early-stage company is skyrocketing – on track to reach 3–5× its current value. You need $50 million to get there.

Do you: Raise $50M in equity at today’s valuation (surrendering a large chunk of ownership now), or Secure a $50M credit facility at ~10–13% interest (borrowing only what you need)?

Option 1 – Equity: Raising this capital via equity means heavy dilution. You’d give away a big slice of your company at a relatively low valuation. When the company’s value multiplies, that slice could be worth far more – value that early shareholders won’t get to keep. Plus, new equity often brings new decision-makers (board seats, veto rights), further diluting your control.

Option 2 – Debt: A credit facility is non-dilutive – you keep 100% of your equity. You borrow what you need, when you need it, and pay interest (~10%) on just that. This interest is a finite, predictable cost, often trivial compared to the long-term price of giving up equity. As one venture insider says, “debt is cheaper than equity, and it always will be.” By using debt, you preserve the full upside when the company reaches a higher valuation – meaning the founders and early investors enjoy the payoff of that growth, not new investors.

From a fiduciary duty perspective, the debt route can be the more responsible choice. If massive growth is ahead, a reasonable loan can better protect current owners’ and other investors' stakes in the company than an underpriced equity round.

Good governance means considering options that minimize dilution and maximize shareholder value. Why dilute early backers unnecessarily if you believe in the trajectory?

Bottom line: In this scenario, debt financing seems to be the winner. It provides the $50M growth capital without forcing you to surrender equity. The company can reach that 3–5× valuation while preserving the founders’ ownership for the big payday. It’s a win-win – fuel growth now, reap maximum value later – all at a lower cost of capital than equity.

For many lower-middle-market companies, this strategy is a game-changer: fuel growth wisely without giving up equity. That can make all the difference in sub-$100M M&A deals.

What has been your experience in the lower middle market in comparing equity versus debt solutions? I really want to know!

*This is not legal advice, at all. It is a simplified look at what successful growing companies often must consider when seeking growth capital. We advice you to work with competent counsel when raising money or doing M&A deals.*

👉 Next up: how debt financing can help lower-middle-market M&A players accelerate growth and expand their reach in upcoming deals.

#DebtFinancing #NonDilutive #GrowthStrategy #FiduciaryDuty #StartupFinance #MergersAndAcquisitions #LowerMiddleMarket #CorporateFinance

[Pics other than the obvious explained; Our officemate Oliver; Building near our offices]

Small But Mighty: Five Days. Ten Million Dollars. One Relentless Team. **First CLOSING of 2026!**

Last Friday at 4:00 PM, my phone rang. A strategic partner explained that a profitable technology company needed capital—urgently. Not in weeks. Not in days. Now.

They didn't hire Benedict Advisors (BA) to be their counsel. They hired us for one reason: our business network, developed over the last 30 years.

What happened next was a masterclass in execution under pressure.

The Challenge:

**Secure debt capital immediately

**No existing lender relationships

**Clock ticking on critical business needs

**Every hour mattered

The Result:

**4.5 business days to signing

**5 business days to $8M wired and in their account

**Another $2M committed and coming soon (we are on it!)

Total loan: $8M closed and in their bank account before most deals even get a first call scheduled Let me be clear—this wasn't just fast. This was impossibly fast by industry standards.

Getting a $8M commitment signed and funded in five business days required every ounce of skill, relationships, and sheer determination our team could muster. There were intense moments. Stressful calls. Late nights. But there was also something beautiful: watching professionals operate at the highest level when it matters most.

Gratitude where it's due:

**To our strategic partner who had the confidence to bring us this opportunity—thank you for trusting Benedict Advisors to deliver when the stakes were highest.

**To our debt financing partners—your professionalism, humility, and work ethic, even in the most challenging moments, made this possible. You're the best in the business.

**To our team—this is what we do. Our first closing of 2026, and what a way to start.

But we're not done.

We're already working in parallel on:

**Securing the remaining $2M immediately

**Structuring a more cost-effective $30M credit facility to take out the more expensive and urgently obtained debt and fuel this company's next phase of growth

The goal? Help them potentially exceed $200M in gross revenue this year.

This is why Benedict Advisors exists. Not to be the biggest. To be the fastest, most connected, and most relentless when our clients need us most.

If you're a founder, operator, or investor working on deals in the $100K to $100M range and you need capital or strategic M&A support—speed and network matter.

Congratulations to everyone who made this happen and to the client. And now on to close the $2 million ASAP and $30 million credit facility to complete the establishment of an important debt capital partner for this impressive company!

hashtag#Financings hashtag#Capital hashtag#CorporateLaw hashtag#M&A hashtag#BenedictAdvisors hashtag#BusinessPartners hashtag#Teamwork

[Pics, NYSBA 150 Anniversary and Annual Meeting with President Elect of NYSBA; NYSBA Presidential Gala; Even Corporate and M&A attorneys stay safe on the streets of NYC. It was brutally cold]

Mergers and Acquisitions Educational Update (MAEU): Rollover Equity – Still a Second Bite, But Now With Sharper Teeth (2025)

We are advising seller-founders on a $30 million sale to a Private Equity fund involving a massive, 40% seller rollover. This morning I was discussing with a seller of a $3 million business in NY the need to be a little flexible on this. It got me thinking about the trends and increasingly buyer-friendly terms of seller rollovers. This post considers how common they have become and rehashes some obvious considerations. Part 2 will consider the "sharper teeth" (buyer-friendly terms like forfeiture and clawbacks).

Rollover equity is common in the lower middle market, giving sellers a chance at a “second bite of the apple.” Recent data shows roughly 60–65% of sub-$100M deals now include a seller equity rollover. Private equity (PE) buyers typically require 10–40% of equity to be rolled, with ~20% being the common midpoint. By contrast, strategic buyers (operating companies) are less likely to use rollovers, and if they do, it’s usually more modest (often 5–20% or less).

Buyer Benefits:

Aligned incentives & continuity: Rollover equity keeps the seller invested alongside the buyer. Sellers who retain a stake signal confidence in the company’s future, ensuring their “skin in the game” aligns interests and aids a smooth transition. Key managers are more likely to stay on post-deal, driven to grow value for that eventual second payout.

Lower cash outlay: Having sellers roll a portion of equity reduces the upfront cash the buyer must deliver. In essence, the rollover acts as seller financing, meaning the PE firm can put in less consideration at closing. This structure de-risks the deal financing for potentially allowing a higher overall price by deferring part of the payment into the future.

Seller Concerns:

Minority stake & control: Once equity is rolled, the seller becomes a minority shareholder with limited control. Important decisions and timing of the final exit are now mainly in the buyer’s hands. Sellers must trust the Buyer's strategy. They no longer have veto power on major moves.

Illiquidity & risk exposure: Any rolled equity is locked up until a future exit, which could be years. There’s no guarantee of a successful “second bite” – if the company underperforms or market conditions worsen, the rolled portion’s value can erode/vanish. Sellers re-invest in their own business’s next chapter, with all the accompanying market and performance risks.

Simply put, rollover equity can be a win-win deal enhancer – aligning goals and boosting long-term returns. In 2025-2026 expect it to come with sharper teeth. Look for future posts to focus on buyer-friendly deal terms that have become more common.

#MergersAndAcquisitions #PrivateEquity #DealStructure #LMM #BenedictAdvisors #MAEU #SMB

[Pics- NYE Celebrations, Big M&A explodes, Impromptu HS Reunion East Greenbush NY]

Why do people like venture capital?

The majority of the top 10 companies in the US are tech companies that were funded by VCs.

It’s true that many venture investments are a total loss, but the winners can be massive.

Plus, you get a front-row seat to how the future is being built. Many investors value the information as much as (or more than) the pure financial returns.

In biglaw, we had a "venture capital" client who came to us after they had formed several SPVs.

☠️They had unknowingly blown their "VC exemption" under the Advisers Act.

If you're a "VC" you can't have *any* funds or SPVs under management that are more than 20% secondaries, fund-of-funds investments, or anything other than primary investments into operating businesses.

Even *one* secondaries SPV blows your exemption.

Don't let this happen to you!

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU) 🔥

EARNOUTS: THE DEAL TOOL THAT CAN MAKE — OR BREAK — YOUR POST-CLOSING RELATIONSHIP

As an M&A BigLaw attorney trained at places like White & Case and Schulte Roth, I have seen earnouts save deals that would otherwise die on the vine.

I have also seen them destroy relationships. One 2025 study showed earnouts in roughly 22% of private deals last year. In lower-middle-market deals under $25M, far higher. But earnouts can be problematic if not structured properly. Roughly 28% end in formal disputes. Earnouts are good when done right. Here are some thoughts on EOs:

TOP THREE REASONS EARNOUTS CREATE A MEETING OF THE MINDS

1️⃣ THEY BRIDGE THE VALUATION GAP WITHOUT KILLING THE DEAL

Buyer sees risk. Seller sees upside. Neither is wrong.

An earnout lets both be right — on their own timeline. The seller gets paid for the future they believe in. The buyer gets protection if it does not materialize.

→ Without earnouts, many lower middle market deals simply never close.

2️⃣ THEY ALIGN INCENTIVES AFTER THE WIRE HITS

A well-structured earnout turns the seller into the buyer's most motivated operator post-closing. When both sides win if the business grows, the dynamic shifts from suspicion to shared purpose.

→ The best earnouts make the seller feel like a partner, not a hostage.

3️⃣ THEY FORCE BOTH SIDES TO DEFINE SUCCESS — IN WRITING

Earnout negotiations require the buyer and seller to agree on what good performance looks like. Revenue targets. Milestone definitions. Measurement periods. That specificity eliminates vague expectations that poison post-closing relationships.

→ If you cannot agree on metrics, you probably cannot agree on how to run the business together.

TIPS TO MAKE YOUR EARNOUT WORK AS A TEAM

→ Use simple metrics. Revenue is the standard — 62% of 2024 earnouts used it. EBITDA invites manipulation disputes.

→ Keep the period short. Market median is 24 months. No 2024 deal exceeded four years.

→ Run the business as a stand-alone unit with separate books. Integration destroys measurement integrity.

→ Replace vague "commercially reasonable efforts" with concrete obligations — minimum spend commitments, staffing levels, operational milestones.

→ Especially on larger earnouts, build tiered payouts instead of all-or-nothing cliffs. Partial credit preserves goodwill when targets are narrowly missed.

→ Diligence the buyer's culture and earnout track record. If the seller does not trust the buyer, no drafting will save it.

THE BOTTOM LINE

An earnout is the only M&A provision that requires the buyer and seller to keep working together for years. Design it for the relationship. Not the lawsuit.

BigLaw trained. Lower middle market focused.

📩 DM me if you are structuring an earnout and want to get it right.

#MAEU #MergersAndAcquisitions #BenedictAdvisors #TabberBenedict #LowerMiddleMarket #Earnouts #MADeals #CorporateLaw #DealStructure #PrivateEquity

[With friends, met George, Events w/ views]](https://pbs.twimg.com/media/HHr4J8DXYAAXoH3.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU) 🔥

EARNOUTS: THE DEAL TOOL THAT CAN MAKE — OR BREAK — YOUR POST-CLOSING RELATIONSHIP

As an M&A BigLaw attorney trained at places like White & Case and Schulte Roth, I have seen earnouts save deals that would otherwise die on the vine.

I have also seen them destroy relationships. One 2025 study showed earnouts in roughly 22% of private deals last year. In lower-middle-market deals under $25M, far higher. But earnouts can be problematic if not structured properly. Roughly 28% end in formal disputes. Earnouts are good when done right. Here are some thoughts on EOs:

TOP THREE REASONS EARNOUTS CREATE A MEETING OF THE MINDS

1️⃣ THEY BRIDGE THE VALUATION GAP WITHOUT KILLING THE DEAL

Buyer sees risk. Seller sees upside. Neither is wrong.

An earnout lets both be right — on their own timeline. The seller gets paid for the future they believe in. The buyer gets protection if it does not materialize.

→ Without earnouts, many lower middle market deals simply never close.

2️⃣ THEY ALIGN INCENTIVES AFTER THE WIRE HITS

A well-structured earnout turns the seller into the buyer's most motivated operator post-closing. When both sides win if the business grows, the dynamic shifts from suspicion to shared purpose.

→ The best earnouts make the seller feel like a partner, not a hostage.

3️⃣ THEY FORCE BOTH SIDES TO DEFINE SUCCESS — IN WRITING

Earnout negotiations require the buyer and seller to agree on what good performance looks like. Revenue targets. Milestone definitions. Measurement periods. That specificity eliminates vague expectations that poison post-closing relationships.

→ If you cannot agree on metrics, you probably cannot agree on how to run the business together.

TIPS TO MAKE YOUR EARNOUT WORK AS A TEAM

→ Use simple metrics. Revenue is the standard — 62% of 2024 earnouts used it. EBITDA invites manipulation disputes.

→ Keep the period short. Market median is 24 months. No 2024 deal exceeded four years.

→ Run the business as a stand-alone unit with separate books. Integration destroys measurement integrity.

→ Replace vague "commercially reasonable efforts" with concrete obligations — minimum spend commitments, staffing levels, operational milestones.

→ Especially on larger earnouts, build tiered payouts instead of all-or-nothing cliffs. Partial credit preserves goodwill when targets are narrowly missed.

→ Diligence the buyer's culture and earnout track record. If the seller does not trust the buyer, no drafting will save it.

THE BOTTOM LINE

An earnout is the only M&A provision that requires the buyer and seller to keep working together for years. Design it for the relationship. Not the lawsuit.

BigLaw trained. Lower middle market focused.

📩 DM me if you are structuring an earnout and want to get it right.

#MAEU #MergersAndAcquisitions #BenedictAdvisors #TabberBenedict #LowerMiddleMarket #Earnouts #MADeals #CorporateLaw #DealStructure #PrivateEquity

[With friends, met George, Events w/ views]](https://pbs.twimg.com/media/HHr4IRwXIAIBmup.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU) 🔥

EARNOUTS: THE DEAL TOOL THAT CAN MAKE — OR BREAK — YOUR POST-CLOSING RELATIONSHIP

As an M&A BigLaw attorney trained at places like White & Case and Schulte Roth, I have seen earnouts save deals that would otherwise die on the vine.

I have also seen them destroy relationships. One 2025 study showed earnouts in roughly 22% of private deals last year. In lower-middle-market deals under $25M, far higher. But earnouts can be problematic if not structured properly. Roughly 28% end in formal disputes. Earnouts are good when done right. Here are some thoughts on EOs:

TOP THREE REASONS EARNOUTS CREATE A MEETING OF THE MINDS

1️⃣ THEY BRIDGE THE VALUATION GAP WITHOUT KILLING THE DEAL

Buyer sees risk. Seller sees upside. Neither is wrong.

An earnout lets both be right — on their own timeline. The seller gets paid for the future they believe in. The buyer gets protection if it does not materialize.

→ Without earnouts, many lower middle market deals simply never close.

2️⃣ THEY ALIGN INCENTIVES AFTER THE WIRE HITS

A well-structured earnout turns the seller into the buyer's most motivated operator post-closing. When both sides win if the business grows, the dynamic shifts from suspicion to shared purpose.

→ The best earnouts make the seller feel like a partner, not a hostage.

3️⃣ THEY FORCE BOTH SIDES TO DEFINE SUCCESS — IN WRITING

Earnout negotiations require the buyer and seller to agree on what good performance looks like. Revenue targets. Milestone definitions. Measurement periods. That specificity eliminates vague expectations that poison post-closing relationships.

→ If you cannot agree on metrics, you probably cannot agree on how to run the business together.

TIPS TO MAKE YOUR EARNOUT WORK AS A TEAM

→ Use simple metrics. Revenue is the standard — 62% of 2024 earnouts used it. EBITDA invites manipulation disputes.

→ Keep the period short. Market median is 24 months. No 2024 deal exceeded four years.

→ Run the business as a stand-alone unit with separate books. Integration destroys measurement integrity.

→ Replace vague "commercially reasonable efforts" with concrete obligations — minimum spend commitments, staffing levels, operational milestones.

→ Especially on larger earnouts, build tiered payouts instead of all-or-nothing cliffs. Partial credit preserves goodwill when targets are narrowly missed.

→ Diligence the buyer's culture and earnout track record. If the seller does not trust the buyer, no drafting will save it.

THE BOTTOM LINE

An earnout is the only M&A provision that requires the buyer and seller to keep working together for years. Design it for the relationship. Not the lawsuit.

BigLaw trained. Lower middle market focused.

📩 DM me if you are structuring an earnout and want to get it right.

#MAEU #MergersAndAcquisitions #BenedictAdvisors #TabberBenedict #LowerMiddleMarket #Earnouts #MADeals #CorporateLaw #DealStructure #PrivateEquity

[With friends, met George, Events w/ views]](https://pbs.twimg.com/media/HHr39BiW0AE-vIQ.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU): Why In-Person Meetings Still Close More Deals Than Zoom

I'm flying down to Florida for meetings on an M&A deal. I'm a buyer-team Principal, and BA is outside co-counsel. En route I'm reflecting on in-person meetings.

While working in BigLaw on multi-billion dollar transactions, deals almost never closed without the principals sitting across from each other. It was a rarity.

Here's why — and why this matters whether you're selling a $2M business or acquiring a $75M platform.

THE DATA IS CLEAR: Harvard Business Review found face-to-face requests are 34x more effective than digital communication. UCLA research shows up to 55% of communication is nonverbal. McKinsey confirms in-person collaboration accelerates decisions by up to 25%.

In the lower middle market — where teams are lean, timelines tight, and trust is everything — those numbers are the difference between closing and collapsing.

THREE FORCES THAT ONLY WORK IN THE ROOM:

📈 Sellers reveal what actually matters. The real concerns never show up in a CIM or on Zoom. The handshake deal with a key employee. The customer driving 40% of revenue. You only get that across a table.

💰 Trust compresses from months to hours. A founder selling a business they built over 20, 30, or 50 years is making a legacy decision. They need to see your eyes, not your profile picture. One dinner builds more trust than six months of emails.

🔥 Advisors align and deals accelerate. When counsel, accountants, intermediaries, and principals share one room, decisions that take weeks over email happen in one afternoon. Speed wins.

WHEN YOU CAN'T BE THERE — AND YOU STILL NEED TO WIN:

Camera on. Every call. No exceptions. Sellers remember faces — not email signatures.

Replace email threads with phone calls. A 5-minute call builds more trust than a 50-email chain. I pick up the phone constantly — trained at BigLaw, works at every deal size.

Stack all key calls on one day. Create the pressure of an in-person closing — even from a screen. Deals that drag are deals that die.

This is what we do at Benedict Advisors (BA). We show up. Physically when possible. Intentionally always.

BigLaw trained. Lower middle market focused. Your strategic partner, not just counsel.

DM me. Let's talk about your next deal.

#MAEU #MergersAndAcquisitions #Deals #CorporateLaw #BenedictAdvisors #SMB #LowerMiddleMarket #DealMaking #TabberBenedict #ClientDriven

[Pics - birthday get together; lawyers, friends, etc.; Quadrille Ball]](https://pbs.twimg.com/media/HDkmGudXEAAyrte.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU): Why In-Person Meetings Still Close More Deals Than Zoom

I'm flying down to Florida for meetings on an M&A deal. I'm a buyer-team Principal, and BA is outside co-counsel. En route I'm reflecting on in-person meetings.

While working in BigLaw on multi-billion dollar transactions, deals almost never closed without the principals sitting across from each other. It was a rarity.

Here's why — and why this matters whether you're selling a $2M business or acquiring a $75M platform.

THE DATA IS CLEAR: Harvard Business Review found face-to-face requests are 34x more effective than digital communication. UCLA research shows up to 55% of communication is nonverbal. McKinsey confirms in-person collaboration accelerates decisions by up to 25%.

In the lower middle market — where teams are lean, timelines tight, and trust is everything — those numbers are the difference between closing and collapsing.

THREE FORCES THAT ONLY WORK IN THE ROOM:

📈 Sellers reveal what actually matters. The real concerns never show up in a CIM or on Zoom. The handshake deal with a key employee. The customer driving 40% of revenue. You only get that across a table.

💰 Trust compresses from months to hours. A founder selling a business they built over 20, 30, or 50 years is making a legacy decision. They need to see your eyes, not your profile picture. One dinner builds more trust than six months of emails.

🔥 Advisors align and deals accelerate. When counsel, accountants, intermediaries, and principals share one room, decisions that take weeks over email happen in one afternoon. Speed wins.

WHEN YOU CAN'T BE THERE — AND YOU STILL NEED TO WIN:

Camera on. Every call. No exceptions. Sellers remember faces — not email signatures.

Replace email threads with phone calls. A 5-minute call builds more trust than a 50-email chain. I pick up the phone constantly — trained at BigLaw, works at every deal size.

Stack all key calls on one day. Create the pressure of an in-person closing — even from a screen. Deals that drag are deals that die.

This is what we do at Benedict Advisors (BA). We show up. Physically when possible. Intentionally always.

BigLaw trained. Lower middle market focused. Your strategic partner, not just counsel.

DM me. Let's talk about your next deal.

#MAEU #MergersAndAcquisitions #Deals #CorporateLaw #BenedictAdvisors #SMB #LowerMiddleMarket #DealMaking #TabberBenedict #ClientDriven

[Pics - birthday get together; lawyers, friends, etc.; Quadrille Ball]](https://pbs.twimg.com/media/HDkmGsqWUAEjN5G.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU): Why In-Person Meetings Still Close More Deals Than Zoom

I'm flying down to Florida for meetings on an M&A deal. I'm a buyer-team Principal, and BA is outside co-counsel. En route I'm reflecting on in-person meetings.

While working in BigLaw on multi-billion dollar transactions, deals almost never closed without the principals sitting across from each other. It was a rarity.

Here's why — and why this matters whether you're selling a $2M business or acquiring a $75M platform.

THE DATA IS CLEAR: Harvard Business Review found face-to-face requests are 34x more effective than digital communication. UCLA research shows up to 55% of communication is nonverbal. McKinsey confirms in-person collaboration accelerates decisions by up to 25%.

In the lower middle market — where teams are lean, timelines tight, and trust is everything — those numbers are the difference between closing and collapsing.

THREE FORCES THAT ONLY WORK IN THE ROOM:

📈 Sellers reveal what actually matters. The real concerns never show up in a CIM or on Zoom. The handshake deal with a key employee. The customer driving 40% of revenue. You only get that across a table.

💰 Trust compresses from months to hours. A founder selling a business they built over 20, 30, or 50 years is making a legacy decision. They need to see your eyes, not your profile picture. One dinner builds more trust than six months of emails.

🔥 Advisors align and deals accelerate. When counsel, accountants, intermediaries, and principals share one room, decisions that take weeks over email happen in one afternoon. Speed wins.

WHEN YOU CAN'T BE THERE — AND YOU STILL NEED TO WIN:

Camera on. Every call. No exceptions. Sellers remember faces — not email signatures.

Replace email threads with phone calls. A 5-minute call builds more trust than a 50-email chain. I pick up the phone constantly — trained at BigLaw, works at every deal size.

Stack all key calls on one day. Create the pressure of an in-person closing — even from a screen. Deals that drag are deals that die.

This is what we do at Benedict Advisors (BA). We show up. Physically when possible. Intentionally always.

BigLaw trained. Lower middle market focused. Your strategic partner, not just counsel.

DM me. Let's talk about your next deal.

#MAEU #MergersAndAcquisitions #Deals #CorporateLaw #BenedictAdvisors #SMB #LowerMiddleMarket #DealMaking #TabberBenedict #ClientDriven

[Pics - birthday get together; lawyers, friends, etc.; Quadrille Ball]](https://pbs.twimg.com/media/HDkmGqfWYAAUWif.jpg)

![TabberBenedict's tweet photo. 🚀 Big Growth, Big Decision: Imagine your early-stage company is skyrocketing – on track to reach 3–5× its current value. You need $50 million to get there.

Do you: Raise $50M in equity at today’s valuation (surrendering a large chunk of ownership now), or Secure a $50M credit facility at ~10–13% interest (borrowing only what you need)?

Option 1 – Equity: Raising this capital via equity means heavy dilution. You’d give away a big slice of your company at a relatively low valuation. When the company’s value multiplies, that slice could be worth far more – value that early shareholders won’t get to keep. Plus, new equity often brings new decision-makers (board seats, veto rights), further diluting your control.

Option 2 – Debt: A credit facility is non-dilutive – you keep 100% of your equity. You borrow what you need, when you need it, and pay interest (~10%) on just that. This interest is a finite, predictable cost, often trivial compared to the long-term price of giving up equity. As one venture insider says, “debt is cheaper than equity, and it always will be.” By using debt, you preserve the full upside when the company reaches a higher valuation – meaning the founders and early investors enjoy the payoff of that growth, not new investors.

From a fiduciary duty perspective, the debt route can be the more responsible choice. If massive growth is ahead, a reasonable loan can better protect current owners’ and other investors' stakes in the company than an underpriced equity round.

Good governance means considering options that minimize dilution and maximize shareholder value. Why dilute early backers unnecessarily if you believe in the trajectory?

Bottom line: In this scenario, debt financing seems to be the winner. It provides the $50M growth capital without forcing you to surrender equity. The company can reach that 3–5× valuation while preserving the founders’ ownership for the big payday. It’s a win-win – fuel growth now, reap maximum value later – all at a lower cost of capital than equity.

For many lower-middle-market companies, this strategy is a game-changer: fuel growth wisely without giving up equity. That can make all the difference in sub-$100M M&A deals.

What has been your experience in the lower middle market in comparing equity versus debt solutions? I really want to know!

*This is not legal advice, at all. It is a simplified look at what successful growing companies often must consider when seeking growth capital. We advice you to work with competent counsel when raising money or doing M&A deals.*

👉 Next up: how debt financing can help lower-middle-market M&A players accelerate growth and expand their reach in upcoming deals.

#DebtFinancing #NonDilutive #GrowthStrategy #FiduciaryDuty #StartupFinance #MergersAndAcquisitions #LowerMiddleMarket #CorporateFinance

[Pics other than the obvious explained; Our officemate Oliver; Building near our offices]](https://pbs.twimg.com/media/G_bPYtJX0AAc6XQ.jpg)

![TabberBenedict's tweet photo. 🚀 Big Growth, Big Decision: Imagine your early-stage company is skyrocketing – on track to reach 3–5× its current value. You need $50 million to get there.

Do you: Raise $50M in equity at today’s valuation (surrendering a large chunk of ownership now), or Secure a $50M credit facility at ~10–13% interest (borrowing only what you need)?

Option 1 – Equity: Raising this capital via equity means heavy dilution. You’d give away a big slice of your company at a relatively low valuation. When the company’s value multiplies, that slice could be worth far more – value that early shareholders won’t get to keep. Plus, new equity often brings new decision-makers (board seats, veto rights), further diluting your control.

Option 2 – Debt: A credit facility is non-dilutive – you keep 100% of your equity. You borrow what you need, when you need it, and pay interest (~10%) on just that. This interest is a finite, predictable cost, often trivial compared to the long-term price of giving up equity. As one venture insider says, “debt is cheaper than equity, and it always will be.” By using debt, you preserve the full upside when the company reaches a higher valuation – meaning the founders and early investors enjoy the payoff of that growth, not new investors.

From a fiduciary duty perspective, the debt route can be the more responsible choice. If massive growth is ahead, a reasonable loan can better protect current owners’ and other investors' stakes in the company than an underpriced equity round.

Good governance means considering options that minimize dilution and maximize shareholder value. Why dilute early backers unnecessarily if you believe in the trajectory?

Bottom line: In this scenario, debt financing seems to be the winner. It provides the $50M growth capital without forcing you to surrender equity. The company can reach that 3–5× valuation while preserving the founders’ ownership for the big payday. It’s a win-win – fuel growth now, reap maximum value later – all at a lower cost of capital than equity.

For many lower-middle-market companies, this strategy is a game-changer: fuel growth wisely without giving up equity. That can make all the difference in sub-$100M M&A deals.

What has been your experience in the lower middle market in comparing equity versus debt solutions? I really want to know!

*This is not legal advice, at all. It is a simplified look at what successful growing companies often must consider when seeking growth capital. We advice you to work with competent counsel when raising money or doing M&A deals.*

👉 Next up: how debt financing can help lower-middle-market M&A players accelerate growth and expand their reach in upcoming deals.

#DebtFinancing #NonDilutive #GrowthStrategy #FiduciaryDuty #StartupFinance #MergersAndAcquisitions #LowerMiddleMarket #CorporateFinance

[Pics other than the obvious explained; Our officemate Oliver; Building near our offices]](https://pbs.twimg.com/media/G_bPYsUXoAAr9Ez.jpg)

![TabberBenedict's tweet photo. Small But Mighty: Five Days. Ten Million Dollars. One Relentless Team. **First CLOSING of 2026!**

Last Friday at 4:00 PM, my phone rang. A strategic partner explained that a profitable technology company needed capital—urgently. Not in weeks. Not in days. Now.

They didn't hire Benedict Advisors (BA) to be their counsel. They hired us for one reason: our business network, developed over the last 30 years.

What happened next was a masterclass in execution under pressure.

The Challenge:

**Secure debt capital immediately

**No existing lender relationships

**Clock ticking on critical business needs

**Every hour mattered

The Result:

**4.5 business days to signing

**5 business days to $8M wired and in their account

**Another $2M committed and coming soon (we are on it!)

Total loan: $8M closed and in their bank account before most deals even get a first call scheduled Let me be clear—this wasn't just fast. This was impossibly fast by industry standards.

Getting a $8M commitment signed and funded in five business days required every ounce of skill, relationships, and sheer determination our team could muster. There were intense moments. Stressful calls. Late nights. But there was also something beautiful: watching professionals operate at the highest level when it matters most.

Gratitude where it's due:

**To our strategic partner who had the confidence to bring us this opportunity—thank you for trusting Benedict Advisors to deliver when the stakes were highest.

**To our debt financing partners—your professionalism, humility, and work ethic, even in the most challenging moments, made this possible. You're the best in the business.

**To our team—this is what we do. Our first closing of 2026, and what a way to start.

But we're not done.

We're already working in parallel on:

**Securing the remaining $2M immediately

**Structuring a more cost-effective $30M credit facility to take out the more expensive and urgently obtained debt and fuel this company's next phase of growth

The goal? Help them potentially exceed $200M in gross revenue this year.

This is why Benedict Advisors exists. Not to be the biggest. To be the fastest, most connected, and most relentless when our clients need us most.

If you're a founder, operator, or investor working on deals in the $100K to $100M range and you need capital or strategic M&A support—speed and network matter.

Congratulations to everyone who made this happen and to the client. And now on to close the $2 million ASAP and $30 million credit facility to complete the establishment of an important debt capital partner for this impressive company!

hashtag#Financings hashtag#Capital hashtag#CorporateLaw hashtag#M&A hashtag#BenedictAdvisors hashtag#BusinessPartners hashtag#Teamwork

[Pics, NYSBA 150 Anniversary and Annual Meeting with President Elect of NYSBA; NYSBA Presidential Gala; Even Corporate and M&A attorneys stay safe on the streets of NYC. It was brutally cold]](https://pbs.twimg.com/media/G-4DcSaXEAAerac.jpg)

![TabberBenedict's tweet photo. Small But Mighty: Five Days. Ten Million Dollars. One Relentless Team. **First CLOSING of 2026!**

Last Friday at 4:00 PM, my phone rang. A strategic partner explained that a profitable technology company needed capital—urgently. Not in weeks. Not in days. Now.

They didn't hire Benedict Advisors (BA) to be their counsel. They hired us for one reason: our business network, developed over the last 30 years.

What happened next was a masterclass in execution under pressure.

The Challenge:

**Secure debt capital immediately

**No existing lender relationships

**Clock ticking on critical business needs

**Every hour mattered

The Result:

**4.5 business days to signing

**5 business days to $8M wired and in their account

**Another $2M committed and coming soon (we are on it!)

Total loan: $8M closed and in their bank account before most deals even get a first call scheduled Let me be clear—this wasn't just fast. This was impossibly fast by industry standards.

Getting a $8M commitment signed and funded in five business days required every ounce of skill, relationships, and sheer determination our team could muster. There were intense moments. Stressful calls. Late nights. But there was also something beautiful: watching professionals operate at the highest level when it matters most.

Gratitude where it's due:

**To our strategic partner who had the confidence to bring us this opportunity—thank you for trusting Benedict Advisors to deliver when the stakes were highest.

**To our debt financing partners—your professionalism, humility, and work ethic, even in the most challenging moments, made this possible. You're the best in the business.

**To our team—this is what we do. Our first closing of 2026, and what a way to start.

But we're not done.

We're already working in parallel on:

**Securing the remaining $2M immediately

**Structuring a more cost-effective $30M credit facility to take out the more expensive and urgently obtained debt and fuel this company's next phase of growth

The goal? Help them potentially exceed $200M in gross revenue this year.

This is why Benedict Advisors exists. Not to be the biggest. To be the fastest, most connected, and most relentless when our clients need us most.

If you're a founder, operator, or investor working on deals in the $100K to $100M range and you need capital or strategic M&A support—speed and network matter.

Congratulations to everyone who made this happen and to the client. And now on to close the $2 million ASAP and $30 million credit facility to complete the establishment of an important debt capital partner for this impressive company!

hashtag#Financings hashtag#Capital hashtag#CorporateLaw hashtag#M&A hashtag#BenedictAdvisors hashtag#BusinessPartners hashtag#Teamwork

[Pics, NYSBA 150 Anniversary and Annual Meeting with President Elect of NYSBA; NYSBA Presidential Gala; Even Corporate and M&A attorneys stay safe on the streets of NYC. It was brutally cold]](https://pbs.twimg.com/media/G-4DYzQXAAEwT0f.jpg)

![TabberBenedict's tweet photo. Small But Mighty: Five Days. Ten Million Dollars. One Relentless Team. **First CLOSING of 2026!**

Last Friday at 4:00 PM, my phone rang. A strategic partner explained that a profitable technology company needed capital—urgently. Not in weeks. Not in days. Now.

They didn't hire Benedict Advisors (BA) to be their counsel. They hired us for one reason: our business network, developed over the last 30 years.

What happened next was a masterclass in execution under pressure.

The Challenge:

**Secure debt capital immediately

**No existing lender relationships

**Clock ticking on critical business needs

**Every hour mattered

The Result:

**4.5 business days to signing

**5 business days to $8M wired and in their account

**Another $2M committed and coming soon (we are on it!)

Total loan: $8M closed and in their bank account before most deals even get a first call scheduled Let me be clear—this wasn't just fast. This was impossibly fast by industry standards.

Getting a $8M commitment signed and funded in five business days required every ounce of skill, relationships, and sheer determination our team could muster. There were intense moments. Stressful calls. Late nights. But there was also something beautiful: watching professionals operate at the highest level when it matters most.

Gratitude where it's due:

**To our strategic partner who had the confidence to bring us this opportunity—thank you for trusting Benedict Advisors to deliver when the stakes were highest.

**To our debt financing partners—your professionalism, humility, and work ethic, even in the most challenging moments, made this possible. You're the best in the business.

**To our team—this is what we do. Our first closing of 2026, and what a way to start.

But we're not done.

We're already working in parallel on:

**Securing the remaining $2M immediately

**Structuring a more cost-effective $30M credit facility to take out the more expensive and urgently obtained debt and fuel this company's next phase of growth

The goal? Help them potentially exceed $200M in gross revenue this year.

This is why Benedict Advisors exists. Not to be the biggest. To be the fastest, most connected, and most relentless when our clients need us most.

If you're a founder, operator, or investor working on deals in the $100K to $100M range and you need capital or strategic M&A support—speed and network matter.

Congratulations to everyone who made this happen and to the client. And now on to close the $2 million ASAP and $30 million credit facility to complete the establishment of an important debt capital partner for this impressive company!

hashtag#Financings hashtag#Capital hashtag#CorporateLaw hashtag#M&A hashtag#BenedictAdvisors hashtag#BusinessPartners hashtag#Teamwork

[Pics, NYSBA 150 Anniversary and Annual Meeting with President Elect of NYSBA; NYSBA Presidential Gala; Even Corporate and M&A attorneys stay safe on the streets of NYC. It was brutally cold]](https://pbs.twimg.com/media/G-4DXIPWAAAIKPM.jpg)

![TabberBenedict's tweet photo. Mergers and Acquisitions Educational Update (MAEU): Rollover Equity – Still a Second Bite, But Now With Sharper Teeth (2025)

We are advising seller-founders on a $30 million sale to a Private Equity fund involving a massive, 40% seller rollover. This morning I was discussing with a seller of a $3 million business in NY the need to be a little flexible on this. It got me thinking about the trends and increasingly buyer-friendly terms of seller rollovers. This post considers how common they have become and rehashes some obvious considerations. Part 2 will consider the "sharper teeth" (buyer-friendly terms like forfeiture and clawbacks).

Rollover equity is common in the lower middle market, giving sellers a chance at a “second bite of the apple.” Recent data shows roughly 60–65% of sub-$100M deals now include a seller equity rollover. Private equity (PE) buyers typically require 10–40% of equity to be rolled, with ~20% being the common midpoint. By contrast, strategic buyers (operating companies) are less likely to use rollovers, and if they do, it’s usually more modest (often 5–20% or less).

Buyer Benefits:

Aligned incentives & continuity: Rollover equity keeps the seller invested alongside the buyer. Sellers who retain a stake signal confidence in the company’s future, ensuring their “skin in the game” aligns interests and aids a smooth transition. Key managers are more likely to stay on post-deal, driven to grow value for that eventual second payout.

Lower cash outlay: Having sellers roll a portion of equity reduces the upfront cash the buyer must deliver. In essence, the rollover acts as seller financing, meaning the PE firm can put in less consideration at closing. This structure de-risks the deal financing for potentially allowing a higher overall price by deferring part of the payment into the future.

Seller Concerns:

Minority stake & control: Once equity is rolled, the seller becomes a minority shareholder with limited control. Important decisions and timing of the final exit are now mainly in the buyer’s hands. Sellers must trust the Buyer's strategy. They no longer have veto power on major moves.

Illiquidity & risk exposure: Any rolled equity is locked up until a future exit, which could be years. There’s no guarantee of a successful “second bite” – if the company underperforms or market conditions worsen, the rolled portion’s value can erode/vanish. Sellers re-invest in their own business’s next chapter, with all the accompanying market and performance risks.

Simply put, rollover equity can be a win-win deal enhancer – aligning goals and boosting long-term returns. In 2025-2026 expect it to come with sharper teeth. Look for future posts to focus on buyer-friendly deal terms that have become more common.

#MergersAndAcquisitions #PrivateEquity #DealStructure #LMM #BenedictAdvisors #MAEU #SMB

[Pics- NYE Celebrations, Big M&A explodes, Impromptu HS Reunion East Greenbush NY]](https://pbs.twimg.com/media/G-D8ixLXoAAiWyu.jpg)

![TabberBenedict's tweet photo. Mergers and Acquisitions Educational Update (MAEU): Rollover Equity – Still a Second Bite, But Now With Sharper Teeth (2025)

We are advising seller-founders on a $30 million sale to a Private Equity fund involving a massive, 40% seller rollover. This morning I was discussing with a seller of a $3 million business in NY the need to be a little flexible on this. It got me thinking about the trends and increasingly buyer-friendly terms of seller rollovers. This post considers how common they have become and rehashes some obvious considerations. Part 2 will consider the "sharper teeth" (buyer-friendly terms like forfeiture and clawbacks).

Rollover equity is common in the lower middle market, giving sellers a chance at a “second bite of the apple.” Recent data shows roughly 60–65% of sub-$100M deals now include a seller equity rollover. Private equity (PE) buyers typically require 10–40% of equity to be rolled, with ~20% being the common midpoint. By contrast, strategic buyers (operating companies) are less likely to use rollovers, and if they do, it’s usually more modest (often 5–20% or less).

Buyer Benefits:

Aligned incentives & continuity: Rollover equity keeps the seller invested alongside the buyer. Sellers who retain a stake signal confidence in the company’s future, ensuring their “skin in the game” aligns interests and aids a smooth transition. Key managers are more likely to stay on post-deal, driven to grow value for that eventual second payout.

Lower cash outlay: Having sellers roll a portion of equity reduces the upfront cash the buyer must deliver. In essence, the rollover acts as seller financing, meaning the PE firm can put in less consideration at closing. This structure de-risks the deal financing for potentially allowing a higher overall price by deferring part of the payment into the future.

Seller Concerns:

Minority stake & control: Once equity is rolled, the seller becomes a minority shareholder with limited control. Important decisions and timing of the final exit are now mainly in the buyer’s hands. Sellers must trust the Buyer's strategy. They no longer have veto power on major moves.

Illiquidity & risk exposure: Any rolled equity is locked up until a future exit, which could be years. There’s no guarantee of a successful “second bite” – if the company underperforms or market conditions worsen, the rolled portion’s value can erode/vanish. Sellers re-invest in their own business’s next chapter, with all the accompanying market and performance risks.

Simply put, rollover equity can be a win-win deal enhancer – aligning goals and boosting long-term returns. In 2025-2026 expect it to come with sharper teeth. Look for future posts to focus on buyer-friendly deal terms that have become more common.

#MergersAndAcquisitions #PrivateEquity #DealStructure #LMM #BenedictAdvisors #MAEU #SMB

[Pics- NYE Celebrations, Big M&A explodes, Impromptu HS Reunion East Greenbush NY]](https://pbs.twimg.com/media/G-D8iwlWEAAOexp.jpg)

![TabberBenedict's tweet photo. Mergers and Acquisitions Educational Update (MAEU): Rollover Equity – Still a Second Bite, But Now With Sharper Teeth (2025)

We are advising seller-founders on a $30 million sale to a Private Equity fund involving a massive, 40% seller rollover. This morning I was discussing with a seller of a $3 million business in NY the need to be a little flexible on this. It got me thinking about the trends and increasingly buyer-friendly terms of seller rollovers. This post considers how common they have become and rehashes some obvious considerations. Part 2 will consider the "sharper teeth" (buyer-friendly terms like forfeiture and clawbacks).

Rollover equity is common in the lower middle market, giving sellers a chance at a “second bite of the apple.” Recent data shows roughly 60–65% of sub-$100M deals now include a seller equity rollover. Private equity (PE) buyers typically require 10–40% of equity to be rolled, with ~20% being the common midpoint. By contrast, strategic buyers (operating companies) are less likely to use rollovers, and if they do, it’s usually more modest (often 5–20% or less).

Buyer Benefits:

Aligned incentives & continuity: Rollover equity keeps the seller invested alongside the buyer. Sellers who retain a stake signal confidence in the company’s future, ensuring their “skin in the game” aligns interests and aids a smooth transition. Key managers are more likely to stay on post-deal, driven to grow value for that eventual second payout.

Lower cash outlay: Having sellers roll a portion of equity reduces the upfront cash the buyer must deliver. In essence, the rollover acts as seller financing, meaning the PE firm can put in less consideration at closing. This structure de-risks the deal financing for potentially allowing a higher overall price by deferring part of the payment into the future.

Seller Concerns:

Minority stake & control: Once equity is rolled, the seller becomes a minority shareholder with limited control. Important decisions and timing of the final exit are now mainly in the buyer’s hands. Sellers must trust the Buyer's strategy. They no longer have veto power on major moves.

Illiquidity & risk exposure: Any rolled equity is locked up until a future exit, which could be years. There’s no guarantee of a successful “second bite” – if the company underperforms or market conditions worsen, the rolled portion’s value can erode/vanish. Sellers re-invest in their own business’s next chapter, with all the accompanying market and performance risks.

Simply put, rollover equity can be a win-win deal enhancer – aligning goals and boosting long-term returns. In 2025-2026 expect it to come with sharper teeth. Look for future posts to focus on buyer-friendly deal terms that have become more common.

#MergersAndAcquisitions #PrivateEquity #DealStructure #LMM #BenedictAdvisors #MAEU #SMB

[Pics- NYE Celebrations, Big M&A explodes, Impromptu HS Reunion East Greenbush NY]](https://pbs.twimg.com/media/G-D8iwjWgAAzqpA.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU) 🔥

EARNOUTS: THE DEAL TOOL THAT CAN MAKE — OR BREAK — YOUR POST-CLOSING RELATIONSHIP

As an M&A BigLaw attorney trained at places like White & Case and Schulte Roth, I have seen earnouts save deals that would otherwise die on the vine.

I have also seen them destroy relationships. One 2025 study showed earnouts in roughly 22% of private deals last year. In lower-middle-market deals under $25M, far higher. But earnouts can be problematic if not structured properly. Roughly 28% end in formal disputes. Earnouts are good when done right. Here are some thoughts on EOs:

TOP THREE REASONS EARNOUTS CREATE A MEETING OF THE MINDS

1️⃣ THEY BRIDGE THE VALUATION GAP WITHOUT KILLING THE DEAL

Buyer sees risk. Seller sees upside. Neither is wrong.

An earnout lets both be right — on their own timeline. The seller gets paid for the future they believe in. The buyer gets protection if it does not materialize.

→ Without earnouts, many lower middle market deals simply never close.

2️⃣ THEY ALIGN INCENTIVES AFTER THE WIRE HITS

A well-structured earnout turns the seller into the buyer's most motivated operator post-closing. When both sides win if the business grows, the dynamic shifts from suspicion to shared purpose.

→ The best earnouts make the seller feel like a partner, not a hostage.

3️⃣ THEY FORCE BOTH SIDES TO DEFINE SUCCESS — IN WRITING

Earnout negotiations require the buyer and seller to agree on what good performance looks like. Revenue targets. Milestone definitions. Measurement periods. That specificity eliminates vague expectations that poison post-closing relationships.

→ If you cannot agree on metrics, you probably cannot agree on how to run the business together.

TIPS TO MAKE YOUR EARNOUT WORK AS A TEAM

→ Use simple metrics. Revenue is the standard — 62% of 2024 earnouts used it. EBITDA invites manipulation disputes.

→ Keep the period short. Market median is 24 months. No 2024 deal exceeded four years.

→ Run the business as a stand-alone unit with separate books. Integration destroys measurement integrity.

→ Replace vague "commercially reasonable efforts" with concrete obligations — minimum spend commitments, staffing levels, operational milestones.

→ Especially on larger earnouts, build tiered payouts instead of all-or-nothing cliffs. Partial credit preserves goodwill when targets are narrowly missed.

→ Diligence the buyer's culture and earnout track record. If the seller does not trust the buyer, no drafting will save it.

THE BOTTOM LINE

An earnout is the only M&A provision that requires the buyer and seller to keep working together for years. Design it for the relationship. Not the lawsuit.

BigLaw trained. Lower middle market focused.

📩 DM me if you are structuring an earnout and want to get it right.

#MAEU #MergersAndAcquisitions #BenedictAdvisors #TabberBenedict #LowerMiddleMarket #Earnouts #MADeals #CorporateLaw #DealStructure #PrivateEquity

[With friends, met George, Events w/ views]](https://pbs.twimg.com/media/HHr4P5oWwAMqLrl.jpg)

![TabberBenedict's tweet photo. 🔥 Mergers and Acquisitions Educational Update (MAEU): Why In-Person Meetings Still Close More Deals Than Zoom

I'm flying down to Florida for meetings on an M&A deal. I'm a buyer-team Principal, and BA is outside co-counsel. En route I'm reflecting on in-person meetings.

While working in BigLaw on multi-billion dollar transactions, deals almost never closed without the principals sitting across from each other. It was a rarity.

Here's why — and why this matters whether you're selling a $2M business or acquiring a $75M platform.

THE DATA IS CLEAR: Harvard Business Review found face-to-face requests are 34x more effective than digital communication. UCLA research shows up to 55% of communication is nonverbal. McKinsey confirms in-person collaboration accelerates decisions by up to 25%.

In the lower middle market — where teams are lean, timelines tight, and trust is everything — those numbers are the difference between closing and collapsing.

THREE FORCES THAT ONLY WORK IN THE ROOM:

📈 Sellers reveal what actually matters. The real concerns never show up in a CIM or on Zoom. The handshake deal with a key employee. The customer driving 40% of revenue. You only get that across a table.

💰 Trust compresses from months to hours. A founder selling a business they built over 20, 30, or 50 years is making a legacy decision. They need to see your eyes, not your profile picture. One dinner builds more trust than six months of emails.

🔥 Advisors align and deals accelerate. When counsel, accountants, intermediaries, and principals share one room, decisions that take weeks over email happen in one afternoon. Speed wins.

WHEN YOU CAN'T BE THERE — AND YOU STILL NEED TO WIN:

Camera on. Every call. No exceptions. Sellers remember faces — not email signatures.

Replace email threads with phone calls. A 5-minute call builds more trust than a 50-email chain. I pick up the phone constantly — trained at BigLaw, works at every deal size.

Stack all key calls on one day. Create the pressure of an in-person closing — even from a screen. Deals that drag are deals that die.

This is what we do at Benedict Advisors (BA). We show up. Physically when possible. Intentionally always.

BigLaw trained. Lower middle market focused. Your strategic partner, not just counsel.

DM me. Let's talk about your next deal.

#MAEU #MergersAndAcquisitions #Deals #CorporateLaw #BenedictAdvisors #SMB #LowerMiddleMarket #DealMaking #TabberBenedict #ClientDriven

[Pics - birthday get together; lawyers, friends, etc.; Quadrille Ball]](https://pbs.twimg.com/media/HDkmGx-aEAAzvje.jpg)

![TabberBenedict's tweet photo. 🚀 Big Growth, Big Decision: Imagine your early-stage company is skyrocketing – on track to reach 3–5× its current value. You need $50 million to get there.

Do you: Raise $50M in equity at today’s valuation (surrendering a large chunk of ownership now), or Secure a $50M credit facility at ~10–13% interest (borrowing only what you need)?

Option 1 – Equity: Raising this capital via equity means heavy dilution. You’d give away a big slice of your company at a relatively low valuation. When the company’s value multiplies, that slice could be worth far more – value that early shareholders won’t get to keep. Plus, new equity often brings new decision-makers (board seats, veto rights), further diluting your control.

Option 2 – Debt: A credit facility is non-dilutive – you keep 100% of your equity. You borrow what you need, when you need it, and pay interest (~10%) on just that. This interest is a finite, predictable cost, often trivial compared to the long-term price of giving up equity. As one venture insider says, “debt is cheaper than equity, and it always will be.” By using debt, you preserve the full upside when the company reaches a higher valuation – meaning the founders and early investors enjoy the payoff of that growth, not new investors.

From a fiduciary duty perspective, the debt route can be the more responsible choice. If massive growth is ahead, a reasonable loan can better protect current owners’ and other investors' stakes in the company than an underpriced equity round.

Good governance means considering options that minimize dilution and maximize shareholder value. Why dilute early backers unnecessarily if you believe in the trajectory?

Bottom line: In this scenario, debt financing seems to be the winner. It provides the $50M growth capital without forcing you to surrender equity. The company can reach that 3–5× valuation while preserving the founders’ ownership for the big payday. It’s a win-win – fuel growth now, reap maximum value later – all at a lower cost of capital than equity.

For many lower-middle-market companies, this strategy is a game-changer: fuel growth wisely without giving up equity. That can make all the difference in sub-$100M M&A deals.

What has been your experience in the lower middle market in comparing equity versus debt solutions? I really want to know!

*This is not legal advice, at all. It is a simplified look at what successful growing companies often must consider when seeking growth capital. We advice you to work with competent counsel when raising money or doing M&A deals.*

👉 Next up: how debt financing can help lower-middle-market M&A players accelerate growth and expand their reach in upcoming deals.

#DebtFinancing #NonDilutive #GrowthStrategy #FiduciaryDuty #StartupFinance #MergersAndAcquisitions #LowerMiddleMarket #CorporateFinance

[Pics other than the obvious explained; Our officemate Oliver; Building near our offices]](https://pbs.twimg.com/media/G_bPYtZXEAAq09l.jpg)

![TabberBenedict's tweet photo. Small But Mighty: Five Days. Ten Million Dollars. One Relentless Team. **First CLOSING of 2026!**

Last Friday at 4:00 PM, my phone rang. A strategic partner explained that a profitable technology company needed capital—urgently. Not in weeks. Not in days. Now.

They didn't hire Benedict Advisors (BA) to be their counsel. They hired us for one reason: our business network, developed over the last 30 years.

What happened next was a masterclass in execution under pressure.

The Challenge:

**Secure debt capital immediately

**No existing lender relationships

**Clock ticking on critical business needs

**Every hour mattered

The Result:

**4.5 business days to signing

**5 business days to $8M wired and in their account

**Another $2M committed and coming soon (we are on it!)

Total loan: $8M closed and in their bank account before most deals even get a first call scheduled Let me be clear—this wasn't just fast. This was impossibly fast by industry standards.

Getting a $8M commitment signed and funded in five business days required every ounce of skill, relationships, and sheer determination our team could muster. There were intense moments. Stressful calls. Late nights. But there was also something beautiful: watching professionals operate at the highest level when it matters most.

Gratitude where it's due:

**To our strategic partner who had the confidence to bring us this opportunity—thank you for trusting Benedict Advisors to deliver when the stakes were highest.

**To our debt financing partners—your professionalism, humility, and work ethic, even in the most challenging moments, made this possible. You're the best in the business.

**To our team—this is what we do. Our first closing of 2026, and what a way to start.

But we're not done.

We're already working in parallel on:

**Securing the remaining $2M immediately

**Structuring a more cost-effective $30M credit facility to take out the more expensive and urgently obtained debt and fuel this company's next phase of growth

The goal? Help them potentially exceed $200M in gross revenue this year.

This is why Benedict Advisors exists. Not to be the biggest. To be the fastest, most connected, and most relentless when our clients need us most.

If you're a founder, operator, or investor working on deals in the $100K to $100M range and you need capital or strategic M&A support—speed and network matter.

Congratulations to everyone who made this happen and to the client. And now on to close the $2 million ASAP and $30 million credit facility to complete the establishment of an important debt capital partner for this impressive company!

hashtag#Financings hashtag#Capital hashtag#CorporateLaw hashtag#M&A hashtag#BenedictAdvisors hashtag#BusinessPartners hashtag#Teamwork