I spent nearly 25 years managing money at hedge funds.

The biggest lesson wasn't about finding the right trade.

It was learning that human discretion is the real risk.

Here's what I do differently now 🧵

Day trading closes the book at 4:00 PM ET so you never lie awake worrying about a war, default, or tariff announcement breaking out before tomorrow's open.

⚡ The Pulse — 06/16/2026 08:33 ET

$GC 15min score shifted from -39.0 to 74.0 — biggest single-timeframe move on the board.

For informational purposes only.

A strategy you can't follow is not a strategy.

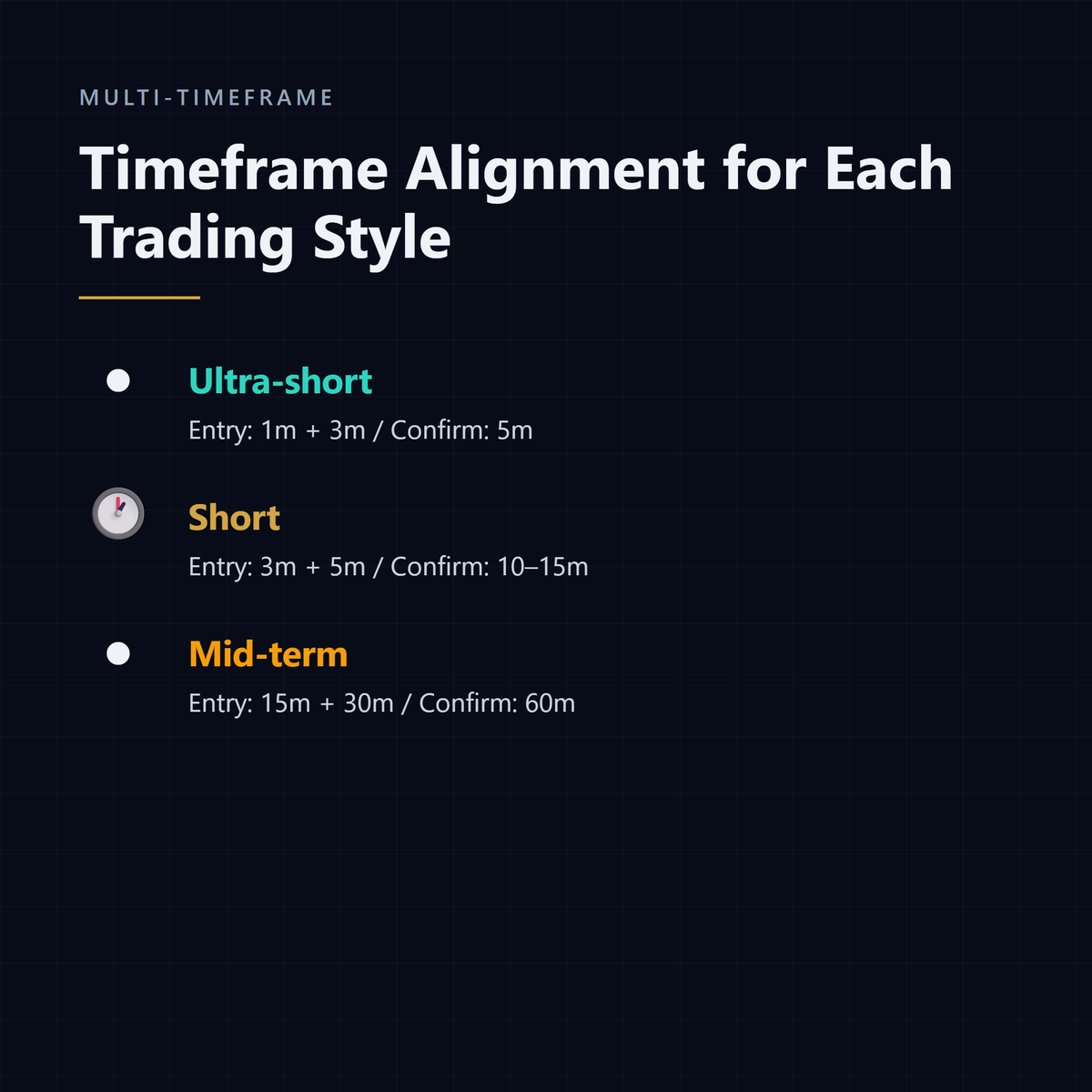

Three filters for design:

— Easy to understand (explain in two sentences)

— Operationally manageable (not 14 hours of screen time)

— Psychologically sustainable (survives a drawdown)

Break any one and you'll abandon the system.

⚡ The Pulse — 06/15/2026 08:33 ET

AAPL daily squeeze fires as tech leaders show three-timeframe green alignment while gold's 60min score slips from green to blue — futures lead the rotation.

For informational purposes only.

TradingView strategies look profitable in backtest, then bleed live. The 5-rule refresh-proof stack:

— barstate.isconfirmed

— process_orders_on_close

— bar-close stops/TPs

— lookahead_off

— close-then-enter on reversals

Skip one and you're trading a different strategy.

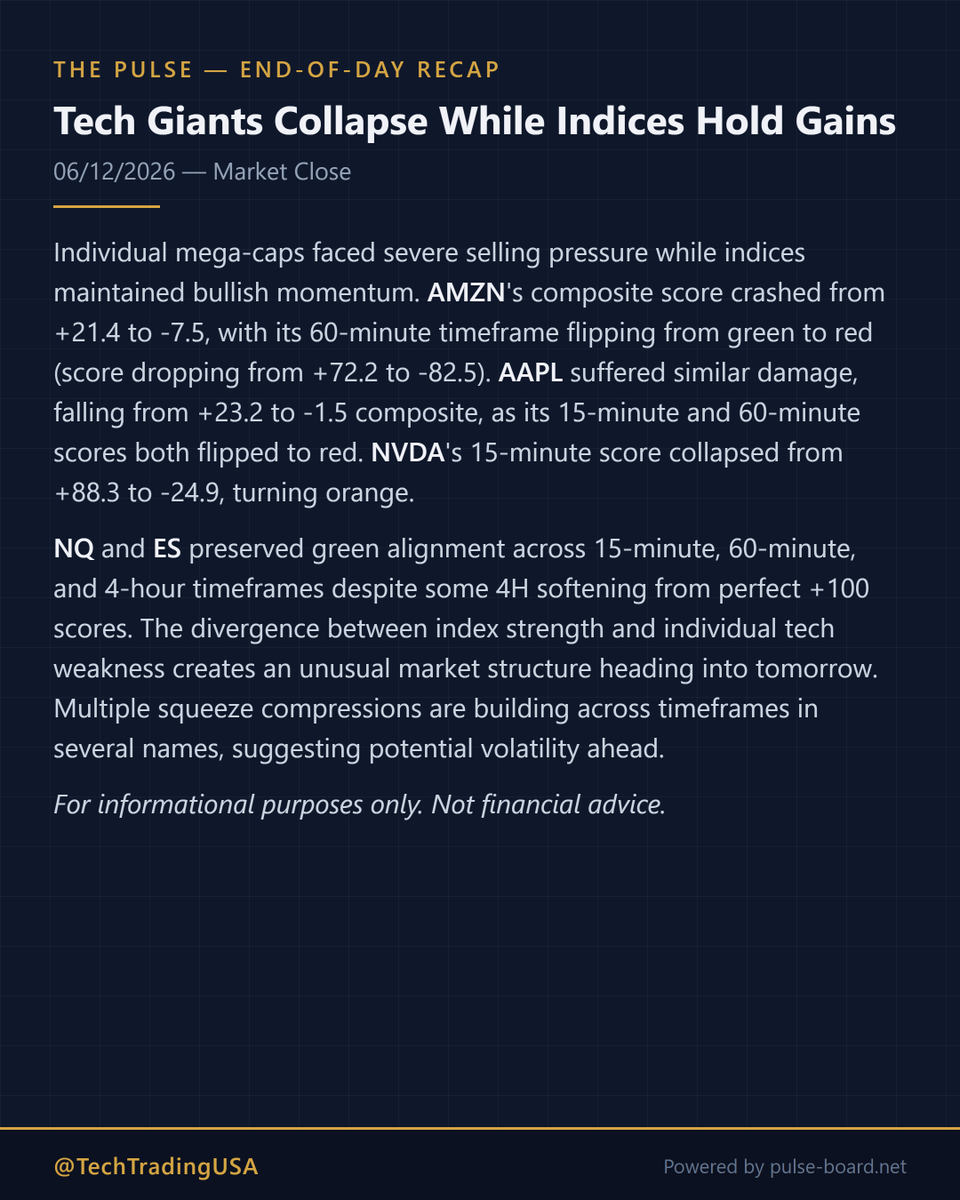

⚡ The Pulse — 06/12/2026 08:33 ET

ES futures fired 4H squeeze with score jumping to 100 as both indices flip green intraday despite red daily reads — compression release begins.

For informational purposes only.

@everythingfxx Simple check I keep coming back to: if your palms are sweating and your heart rate goes up when you enter a position, your size is too big. Fixing the size in advance takes that decision away from the version of me that's mid-trade and emotional.

@pheonix_trader Every extra indicator I added was basically just fitting the strategy to noise — making it "work" on past data while quietly making it worse going forward. Strip it back to price, levels, and hard risk rules and suddenly there's less to hide behind.

@L1vsun No strategy you set and forget. The real work is building a monitoring layer -- rolling metrics that tell you whether the edge is still there, not just whether the P&L looks okay this month.

Strategy testers spit out 20+ metrics. Most are decoration.

Five tell you whether a strategy is real:

— Net Profit

— Win Rate

— Profit Factor (aim > 1.5)

— Max Drawdown

— Total Trades (sample size matters)

If those five look right, the strategy is worth running.

⚡ The Pulse — 06/11/2026 08:33 ET

Gold's 15min score rocketed from -63 to +76 while weekly squeeze fires, creating wild cross-timeframe divergence as metals fragment.

For informational purposes only.

⚡ The Pulse — 06/10/2026 08:33 ET

Gold weekly squeeze fires as GC posts full red alignment across all five timeframes with -85 composite score - metals under pressure

For informational purposes only.

Slippage is such a tricky one to get right. The only way I've found to actually measure it honestly is comparing the price at signal fire to the fill price from the broker -- and that requires a system that logs both reliably. Without that, you're basically guessing, and the guess almost always flatters the backtest.

@ai_trade_pro That gap between backtest and live is brutal. On the equity curve, a drawdown is just a dip before the next leg up — you can see the whole thing at once. In real time you're standing inside it with no idea how deep it goes or when it ends.