NEWS: Elon Musk gives a thorough update after the 4th launch of Starship.

Will we see a catch for Flight 5?

How will Starlink be even better on the next flight?

These are some of the questions Elon answers for us.

I hope this interview informs you about the incredible work SpaceX is doing.

Thank you, @elonmusk for making time to chat.

(please subscribe to support my journalism)

Netflix Q1 2024 Earnings (SUPERCUT) $NFLX

Current Price: $555.12 (as of Friday's Market Closing)

EPS Beat by 16.81% - reported $5.28

Revenue Beat by 0.97% - reported $9.37B

Summary of Netflix Q1 2024 Earnings Call:

Positives:

- #Netflix is evolving its revenue model with the addition of advertising and extra member features, which diversifies its income streams.

- The company is shifting focus to key metrics that matter most for the business, such as revenue, operating income (OI), OI margin, net income, earnings per share (EPS), and free cash flow.

- Netflix has seen significant improvement in member growth, attributed to a consistent release of hit shows, films, and games, as well as success in local unscripted content.

- The company has managed to reaccelerate the business and revenue through improvements in service and new initiatives like paid sharing and launching an ads business.

- Netflix's advertising tier has been scaling rapidly, with a 65% quarter-to-quarter growth, indicating a strong potential for future revenue growth.

- The company is investing in live programming, including sports entertainment, which could drive engagement and advertising opportunities.

- Netflix maintains a disciplined approach to content investment, focusing on variety and quality, and is comfortable with its current level of spending.

- The company has achieved investment-grade status, allowing for more efficient capital allocation and a commitment to returning excess cash to shareholders through share repurchases.

- Engagement trends remain healthy, with steady hours viewed per account in owner households, despite the impact of paid sharing.

Negatives:

- Netflix will stop reporting quarterly membership and ARM data in 2025, which may reduce transparency for analysts and investors.

- Revenue growth is expected to decelerate for the full year, from 15-16% in the first half to 13-15% for the full year, due to tougher comparisons in the second half.

- The company is still in the early stages of building out its advertising business, and monetization has not fully kept up with the growth in inventory.

- There is an acknowledgment that the process of transitioning to paid sharing will impact overall absolute view hours, indicating a potential short-term engagement dip.

- The retirement of the basic plan in some markets, like the U.K. and Canada, could be disruptive for some subscribers, although it is seen as offering more for less.

- Netflix's content spend-to-amortization ratio is expected to remain around 1.1x, which may limit the company's ability to significantly increase content investment in the short term.

Overall, the earnings call reflects a company in transition, focusing on diversifying revenue streams and improving profitability while managing the challenges of a changing business model and competitive landscape.

Tesla FSD 12.3.2.1 Driving from Georgetown to Capitol Hill in Washington, DC

This version is super smooth. It behaves more like a human driver. This version handles DC roundabouts like a champ.

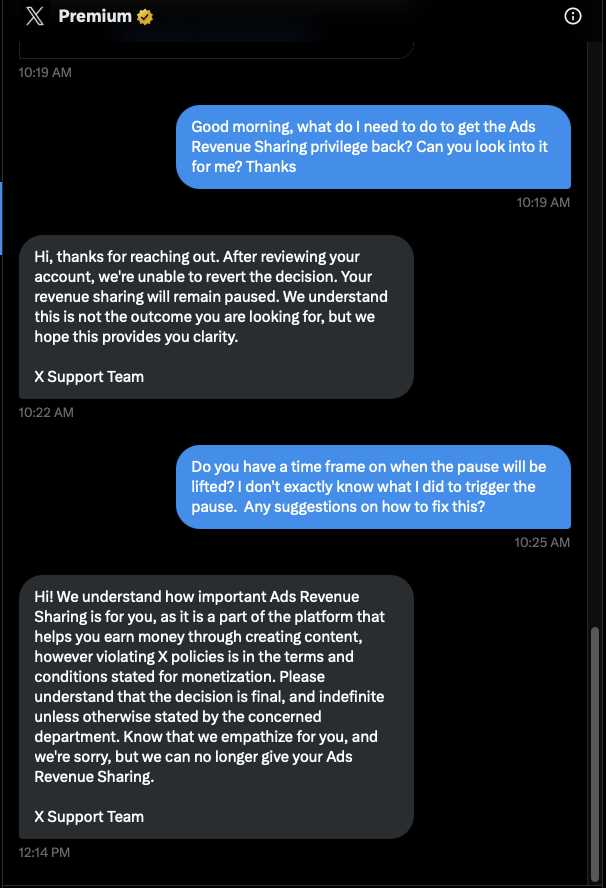

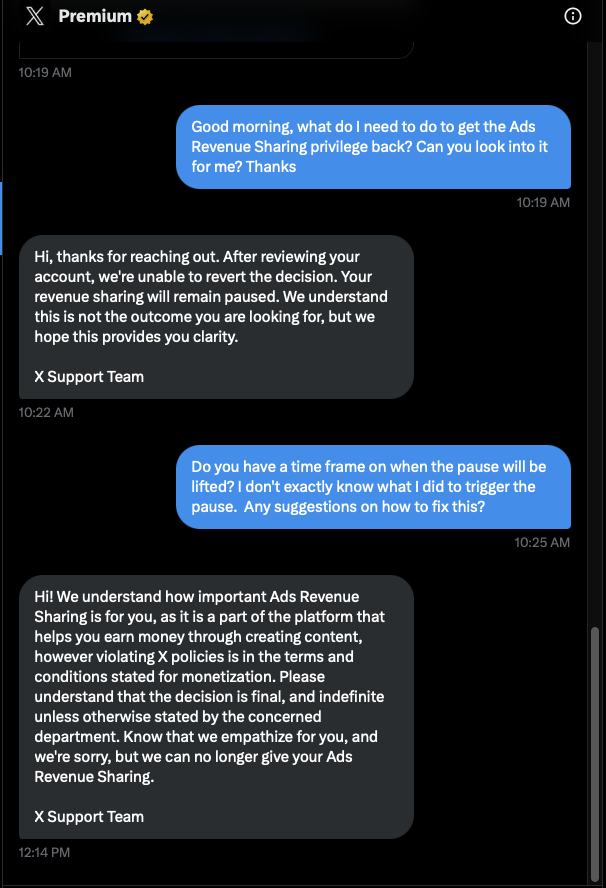

@brockpierson If you all know something, please do share. This was the last interaction with the 𝕏 team as of this morning. I have no idea what I did to trigger the pause.

@monetization_x I don't exactly know what I did to trigger the pause. But this is the last interaction with the 𝕏 team as of this morning. Do I just delete my account and start all over? What are you all doing?