Welcome to The Quantified Universe. 🌌📊

The universe feels chaotic, but the math is always objective. Every day, we strip away the noise and look at the raw numbers behind how everything works—from everyday margins to the edges of the cosmos.

Here is what we break down:

☕ Margin Mondays (Supply Chains & Costs)

💻 Tech Tuesdays (The Digital World)

🗑️ Waste Wednesdays (Inefficiency & Loss)

🎲 Threshold Thursdays (Odds & Probabilities)

🃏 Free-for-All Fridays (Wildcard Numbers)

🚀 Space & Scale Saturdays (Mind-Bending Extremes)

👥 Society Sundays (Crowds & Demographics)

All data is heavily researched. Sources & methodology available upon request.

Follow along to see the matrix. Breakdowns will drop below daily 👇

A claim about ending government fraud requires looking at the historical data of the administration's leadership.

As a numbers account, we don't do political rhetoric. We look at the finalized financial ledger of court judgments.

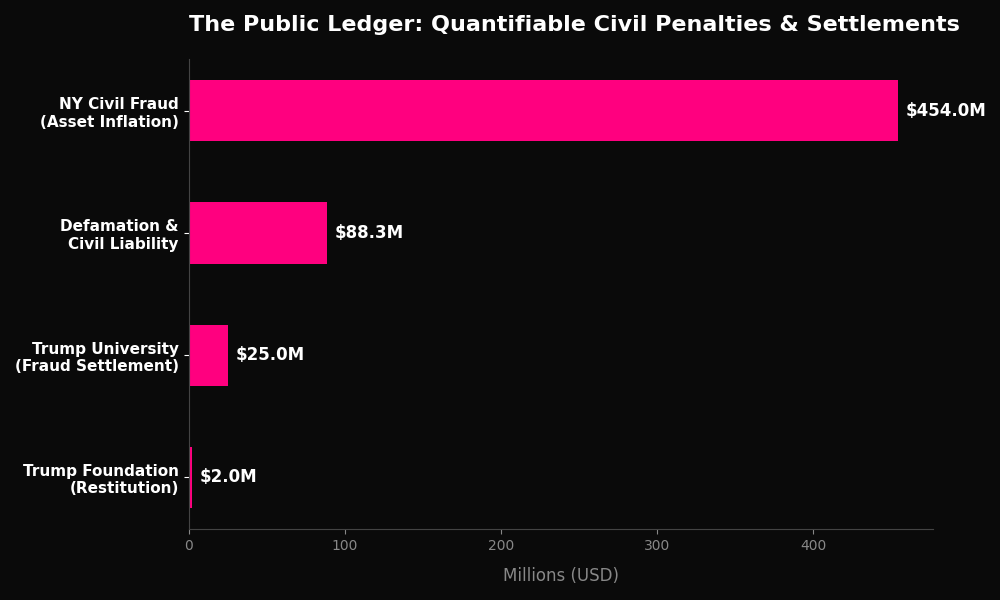

Here is the quantifiable civil penalty data for the President:

New York Civil Fraud Judgment (Asset Inflation): ~$454 Million (w/ interest)

Defamation & Civil Liability Jury Awards: $88.3 Million

Trump University Fraud Settlement: $25 Million

Trump Foundation Restitution (Misuse of Funds): $2 Million

Total quantifiable civil penalties and settlements: ~$569.3 Million.

In data science, a system's historical baseline is the primary variable used to calculate the probability of future outcomes.

The administration just announced $200M to defund green initiatives and build/restart three coal plants.

Let's remove the politics and look purely at the project finance and physics.

First, the math of the funding. $200M is a rounding error in power generation.

A single new 600-megawatt coal plant costs over $2 billion to build.

$200M split three ways barely covers feasibility studies. Private capital must fund the rest.

But Wall Street is not financing new coal because of LCOE (Levelized Cost of Energy).

Coal is currently one of the most expensive ways to build new baseline electricity.

Did the "Green New Deal" fail? It succeeded in building cheap, intermittent solar.

But it failed to provide the 24/7 dispatchable baseload needed for the 2026 AI boom.

The grid absolutely needs hard baseload power to survive.

But the free market has already chosen the winner for that job: Natural Gas.

Gas is cheaper to build, cheaper to fuel, and more efficient than coal. Nuclear may have it beat with zero emissions, but it can't compete on cost.

Energy independence is critical, but capital always flows to the most efficient math.

Treasury Sec. Scott Bessent just testified that 70% of tax filers receiving the new Trump tax cuts earn under $100,000.

The math is 100% accurate, but the framing is a classic "Denominator Illusion."

The administration is measuring the headcount (percentage of total people) rather than the capital distribution (percentage of total dollars saved).

Why does this matter? Because roughly 75% of ALL American taxpayers earn less than $100,000 anyway.

If you pass a broad tax bill that impacts everyone, the recipient list will simply mirror U.S. population demographics. Claiming "70% of the people who got a tax cut make under $100k" sounds like targeted middle-class relief, but mathematically, it just means you gave a tax cut to the general public.

The Treasury analysis deliberately counted who claimed the deductions rather than how much money each income group got back in total. Because the U.S. tax code is progressive (higher earners pay the vast majority of total federal taxes), broad percentage cuts inherently deliver exponentially larger absolute dollar savings to the top 10% of earners.

A middle-class worker might save $815 on overtime, but a high-income earner saves tens of thousands on standard bracket reductions. By counting people instead of capital, you obscure where the actual money is flowing.

The Working Families Tax Cuts delivered real relief via tips and overtime exemptions.

But measuring economic impact by headcount instead of dollar volume is a politician's favorite math trick.

OpenAI is trapped in a low-margin hardware business masquerading as a software company.

Based on recent financial leaks, the company is bleeding billions annually. Top-line revenue is growing, but the cost of server infrastructure and compute is growing faster.

Now add the current macroeconomic reality: severe energy shocks and hardware tariffs. The cost to train and run frontier models has skyrocketed.

Simultaneously, a higher-for-longer rate cycle has frozen the limitless VC capital of the early 2020s. When capital is expensive, burning billions for market share is a death sentence.

Microsoft already provides the compute and owns a massive profit-share. If external funding dries up, Microsoft won’t buy OpenAI at a premium.

They will absorb the IP and talent at a massive discount, wiping out early equity, as you note.

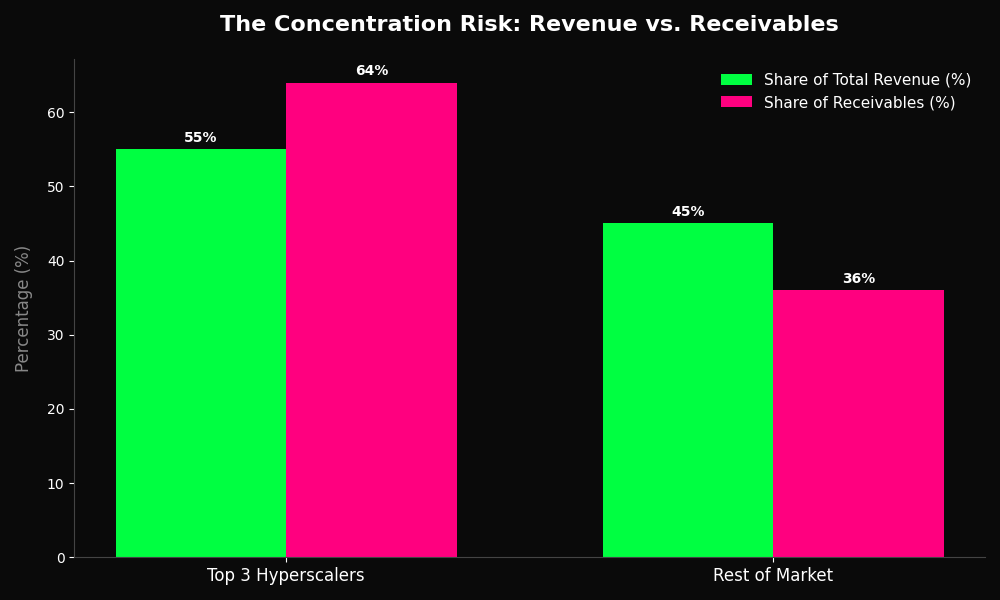

Michael Burry is betting heavily against the AI hardware boom. The bearish thesis relies on three metrics buried in the financial filings.

First is extreme concentration. Three customers account for roughly 64% of unpaid receivables.

Second is payment velocity. Days Sales Outstanding extended from 46 to 53 days.

Third is substitution. The biggest customers are aggressively pivoting to custom in-house silicon.

The prevailing market narrative dismisses this as the natural math of hyper-growth. But Burry is betting on the macroeconomic realities of 2026 to break the cycle.

Big Tech relies on a circular economy: fund an AI startup, sell them cloud compute, buy more GPUs.

Under a higher-for-longer rate cycle, the VC funding keeping those startups alive vanishes.

Add in crippling energy supply shocks that stall new data center deployments.

If end-user demand collapses, the hyperscalers will immediately slash their infrastructure budgets.

We are witnessing a massive geopolitical divergence in Industrial Intelligence.

America holds the compute, the capital, and the code. But the public is actively rejecting it.

Why? Higher-for-longer rates and energy shocks have made AI a shadow tax on the working class.

Tech mega-caps build power-hungry data centers. Everyday Americans pay the surging utility bills.

The public sees concentrated corporate gains, but widespread labor displacement.

Compute is power. But in a democracy, public trust is the ultimate bottleneck to deployment.

The math of surviving a plane crash.

Fear of flying is common, but the numbers don't support it.

Between 1983 and 2000, there were 568 plane crashes in the US. The survival rate of passengers involved in those crashes? 95.7%.

You are safer in the air than in your car.

A 4-day workweek is an incredible idea for societal mental health and work-life balance.

But it completely ignores the mathematical reality of the global economy.

For decades, the West could afford to work 40 hours a week because we had a massive technological advantage. One American engineer with advanced tech could out-produce someone working 80 hours overseas.

That era is over.

Competitors like China operate on a "996" schedule (9 AM to 9 PM, 6 days a week). That is 72 hours of output.

They now possess the same AI, the same robotics, and the same supply chains that we do. The technology gap has closed.

If the technology is equal, the global economy reverts to a pure math equation of raw time. 72 hours will always beat 32 hours (or 40 hours).

We can absolutely choose a 4-day workweek for our own happiness.

But we cannot pretend it is free. We must accept that we are mathematically trading away our global economic supremacy to do it.

If you disagree with something I wrote, try providing sources and I will reply. I'm not a bot, just a retiree putting my research skills to use to keep myself entertained.

Here are my sources for all the posts I have made concerning this topic:

American Society of Plastic Surgeons (ASPS): Post-Weight Loss Body Contouring Statistics (2026).

Bernstein Research: Consumer Sector / Apparel and GLP-1 Windfall Projections ($13 Billion estimate).

Circana: GLP-1 Medication Usage is Impacting the U.S. Apparel Industry (2026 Data).

Circana: "GLP-1 users are changing apparel trends" (March 2026 report tracking the 23% household adoption rate).

Destination XL (DXL) Corporate Earnings Call Transcripts (2025/2026).

Destination XL (DXL) Earnings Call (Retailers reporting extreme volatility in consumer sizing).

Intuitive Surgical / Medtronic Earnings Transcripts: Bariatric Procedure Volume Contraction.

Jefferies Financial Group: "The GLP-1 Airline Fuel Dividend" (Payload and fuel efficiency analysis).

Morgan Stanley Research: The GLP-1 Impact on Food, Beverage, and Tobacco Industries (2025/2026 Projections).

Underoutfit: GLP-1 Intimates Marketing Data (Tracking the 2-to-3 times annual replacement velocity).

Where does a near-trillion-dollar valuation come from for a private AI company?

You just have to reverse-engineer the revenue multiple.

Leaked pre-IPO financials show Anthropic is projecting roughly $14.8 billion in revenue this year.

That means Wall Street is pricing them at a 65x forward revenue multiple. That is historically massive, but standard for the 2026 AI infrastructure super-cycle.

How did they beat OpenAI?

OpenAI won the consumer chatbot war, but Anthropic won the Fortune 500.

Because Anthropic prioritized data security and compliance, banks, defense contractors, and hospitals overwhelmingly chose their Claude models.

Furthermore, Anthropic is deeply integrated into Amazon Web Services (AWS). They effectively collect a tax on global corporate cloud computing.

Wall Street isn't valuing a consumer app. They are valuing a permanent tollbooth on enterprise AI infrastructure.

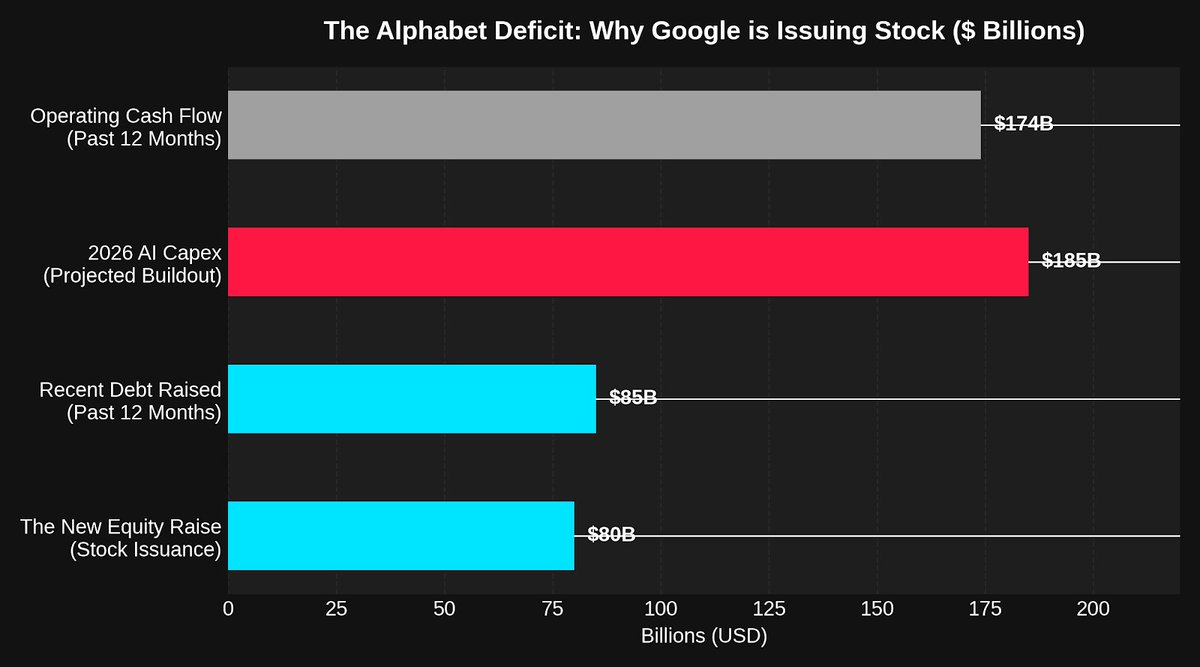

Google is raising $80 billion by issuing new stock.

It is the largest equity raise in corporate history. Why does one of the richest, most cash-flush companies on Earth suddenly need to issue stock to raise money?

Because the math of artificial intelligence is breaking their cash flow (see chart).

Over the last year, Alphabet generated a staggering $174 billion in operating cash flow. But their projected 2026 capital expenditures for AI data centers and compute power is $180 to $190 billion.

They are mathematically spending more on physical infrastructure than their core business generates in cash. Why not just borrow the money? They did. Alphabet took on $85 billion in new debt over the last year.

But in today's high-interest-rate environment, debt is punishing. Taking on another $80 billion in debt would mean billions in annual interest payments, crushing their margins.

Issuing stock is "free" money. The downside is that you dilute your existing shareholders, which usually causes the stock price to tank.

The era of tech giants being capital-light software companies is officially over. They are now heavy infrastructure conglomerates, and the bills are coming due.

#TheMacroScorecard: The Billionaire Tax Trap

The newly proposed ROBINHOOD Act is designed to stop billionaires from avoiding taxes by borrowing against their stock.

It sounds like a massive win for the middle class, but the macroeconomic math reveals it is actually a trap.

The "Buy, Borrow, Die" loophole used to work because borrowing was virtually free. But in today's high-interest-rate environment, the cost of debt is already punishing.

If the government taxes these loans, billionaires won't pay the tax. They will simply stop borrowing.

Instead, they will be forced to systematically sell massive blocks of their mega-cap stock on the open market to raise cash.

If billionaires dump billions of dollars of Amazon, Meta, and Tesla stock every quarter, share prices will mechanically drop.

And who owns the S&P 500? You do.

The S&P 500 is the foundation of almost every 401(k), IRA, and pension in the country.

If this passes, you aren't taxing the billionaires. You are triggering a massive corporate sell-off that will liquidate your own retirement.

This tweet claims that cancer treatments, SSRIs, and vaccines are statistically "worse" than the diseases they treat.

This represents a fundamental failure to understand probability and risk-benefit math.

Medicine operates on a strict mathematical ledger: Does the intervention save more lives than it harms?

If you look at cancer, the math is undeniable (see chart attached).

In the 1970s, prior to modern chemotherapy, a cancer diagnosis was a coin flip. The 5-year survival rate was roughly 50%.

For a child with leukemia, the survival rate was just 10%.

Today, thanks entirely to those "toxic" treatments, a child with leukemia has a 90% chance of survival. Prostate and breast cancer survival rates now push past 90%.

For vaccines, the global ledger is even steeper. The WHO calculates that vaccines mathematically save roughly 5 lives every single minute.

Medical treatments have brutal side effects, and pharmaceutical business models are deeply flawed.

But claiming the treatments are worse than the diseases ignores the millions of people who are mathematically only alive today because they took the trade-off.

That is factually correct, but it is just a tiny fraction of the macroeconomic earthquake currently happening.

The knock-on effects of these weight-loss drugs are rewriting entire sectors of the U.S. economy.

In the medical sector, traditional bariatric surgeries are crashing. Simultaneously, plastic surgeons are booked out for months performing body contouring.

But the biggest blindspot is the "Dopamine Economy."

These drugs don't just slow digestion; they silence the brain's reward centers.

Data shows users don't just stop eating junk food. They actively reduce their consumption of alcohol, tobacco, and gambling.

The snack and beverage industries are terrified because they rely heavily on a small percentage of highly addictive consumers to drive profits.

The math even extends to the laws of physics in commercial aviation.

Wall Street analysts calculate that as the average passenger sheds weight, airlines like United and Delta will save tens of millions of dollars a year in jet fuel costs.

We aren't just altering human waistlines. We are actively restructuring the U.S. GDP.

You are spot on—Victoria's Secret is just the loudest canary in the coal mine.

Whether you buy organic cotton or fast fashion, the structural physics of extreme weight loss dictates you must buy something.

The data for the broader apparel industry is absolutely staggering.

According to 2026 data from Circana, 80% of GLP-1 users anticipate needing a completely new wardrobe, and 55% have already started buying.

Financial analysts project this "Wardrobe Replacement Cycle" will inject up to $13 billion in new, incremental spending into the apparel sector every single year.

At the exact same time, plus-size retailers are getting crushed.

The CEO of DXL recently noted that 25% of his customers are on GLP-1s. They are actively holding off on buying clothes until their weight stabilizes.

This isn't a fashion trend. Biotech just forced a multi-billion dollar cash injection into the global apparel market.

I assume with that reply that you disagree with something I wrote. Please state what specifically and provide sources to refute what I wrote. I (not a bot) will then be able to reply.

Here are my sources:

Circana: "GLP-1 users are changing apparel trends" (March 2026 report tracking the 23% household adoption rate).

Destination XL (DXL) Earnings Call (Retailers reporting extreme volatility in consumer sizing).

Underoutfit: GLP-1 Intimates Marketing Data (Tracking the 2-to-3 times annual replacement velocity).

You're mixing up "political allegiance" with "legal jurisdiction."

This exact argument was actually tested and defeated at the Supreme Court in 1898 (U.S. v. Wong Kim Ark).

Wong Kim Ark's parents were citizens of China who owed allegiance to the Emperor. The Court ruled that it didn't matter. Because they lived here and were bound by U.S. laws, their child was a citizen.

The Court ruled the only exceptions to the 14th Amendment are diplomats with immunity, invading armies, and sovereign tribes. An individual immigrant fits none of those.

Another way to think about it:

If an undocumented immigrant commits a crime on U.S. soil, do we send them to their home country for trial, or do we put them in a U.S. prison?

We put them in a U.S. prison because they are 100% subject to U.S. jurisdiction. Jurisdiction means you are bound by the laws of the land where your feet are planted.

The math of 'Vampire Draw'.

Electronics plugged in but turned off (TVs, microwaves, chargers) still draw power.

This 'vampire draw' accounts for up to 10% of a home's energy use, costing the average household $100-$200 a year for absolutely nothing.

#TheMacroScorecard: The Omission Ledger

This tweet claims a Democratic congressional nominee worked for an Al Qaeda front group and defended a terrorist.

If you look at the raw data, this is a textbook case of Temporal Data Mining.

The poster took two data points from the 1990s, stripped away all chronological context, and completely omitted a decorated U.S. military career.

In 1994, Dr. Adam Hamawy volunteered for a medical charity in Bosnia. That charity was later shut down for terror links. But at the time he was there, the U.S. government was actively praising its humanitarian work.

In 1995, he was subpoenaed to testify under oath at the trial of Omar Abdel-Rahman. He was a witness, never a suspect, and was never accused of any crime.

But here is the massive mathematical omission.

The tweet completely ignores that Dr. Hamawy subsequently enlisted in the U.S. Army Medical Corps.

He served eight years as a combat surgeon. He treated victims of the 9/11 attacks.

During the Iraq War, he saved the life of Senator Tammy Duckworth after her helicopter was shot down, performing emergency vascular surgery to prevent her from becoming a triple amputee.

You can disagree with a politician's platform or their policies.

But taking 30-year-old medical charity work and a subpoenaed testimony to smear a decorated U.S. combat surgeon as an Islamist threat is a historical fraud.

#TheMacroScorecard: The JOLTS Trap

Wall Street was banking on a cooling labor market to force the Federal Reserve to cut interest rates.

Today's JOLTS report just destroyed that narrative.

Job openings violently spiked to 7.6 million, completely shattering the 6.9 million forecast.

But there is a massive illusion hiding inside this data.

A massive percentage of these listings are "ghost jobs."

Many corporations have frozen actual hiring due to tight profit margins.

However, they leave listings open to look financially strong to investors, or to placate burned-out employees by pretending help is coming.

Simultaneously, the administration's new tariffs are forcing domestic factories into a panic-hiring spree to onshore production.

The Federal Reserve cannot cut interest rates even when job openings unexpectedly surge by 700,000 because inflation is refusing to drop.

Good news for the headline labor data is terrible news for the cost of capital. The higher-for-longer rate cycle is here to stay.