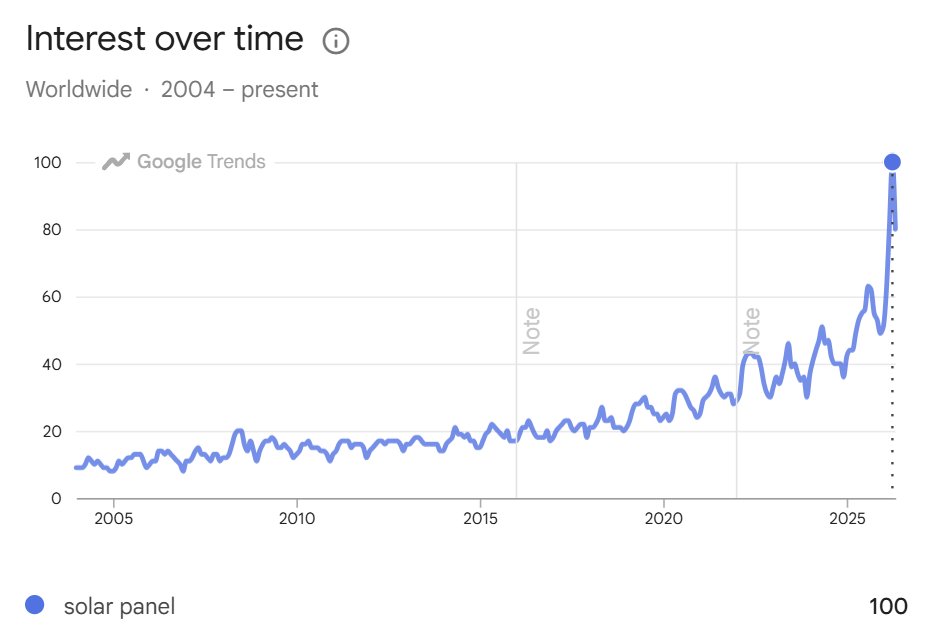

Like so many tech revolutions that precede our times, the AI race is secretly an energy race.

China is building power/infra capacity at a speed the US hasn't seen since the interstate highway system. Solar + storage is the only thing that scales fast enough to match it. It's the NOW solution.

America needs to get past debating permits and realize it's AI ambitions are only as big as its grid.

Right now, China is building new energy capacity at breathtaking speed.

America needs to keep up.

Only solar + storage are able to meet rising demands on time. We'll lose the AI race if we don't.

Like so many tech revolutions that precede our times, the AI race is secretly an energy race.

China is building power capacity at a speed the US hasn't seen since the interstate highway system. Solar + storage is the only thing that scales fast enough to match it. It's the NOW solution.

America needs to get past debating permits and realize it's AI ambitions are only as big as its grid.

Couldn't agree more, this always puzzled me.

Another example of something becoming politically divided that never should have been. Solar offers the right independence, the left a clean conscience, and everyone an economically viable path forward. You'd think a local, low cost solution to energy would excite everyone.

@CleanPowerDave Energy independence is the new national security. Cleantech is becoming more foreign policy and geopolitics than just idealism.

Local cleantech is the exit ramp from global dependency.

Really great way of zooming out here.

Scale like this is going to require everything. Build it all.

Imo solar and nuclear aren't competing, they're both just small parts of an almost incomprehensibly large build.

Solar for rapid, distributed, scalable deployment. Nuclear for firm, always-on baseload with high density that our system will desperately need.

Would be great to add fusion as an option in our lifetime as well.

Seeing this ring true in the energy transition.

As solar's levelized cost dropped below gas peakers, utilities notice. When payback periods hit 6 years, homeowners notice. When panel prices fall 90%, manufacturers notice.

Prices are doing exactly what they're supposed to → all pointing the same direction →☀️

Millions of individual spreadsheets all reaching the same conclusion.

Energy bills still elevated post-inflation. Panel costs down 90% this decade. People stuck in their homes due to mortgage rates → invest in it.

Local energy makes too much sense. Matter of time!

@CleanPowerDave Millions of individual spreadsheets all reaching the same conclusion.

Energy bills still elevated post-inflation. Panel costs down 90% this decade. People stuck in their homes due to mortgage rates → invest in it.

Local energy makes too much sense. Matter of time!

Fortescue is building the quite the rebuttal. The old argument was that heavy industry couldn't run on clean energy.

Mining has long been the poster child for why industrial decarbonization is so hard: enormous equipment, huge & constant power demands.

Meaningful signal to see a company like Fortescue elects to build it's own clean grid rather than waiting for the broader system to decarbonize.

Coal once powered over half this country.

Now it trails two technologies that didn't exist at commercial scale 20 years ago.

The grid is changing faster than most predicted and it's only getting started, regardless of policy.

@cremieuxrecueil Coal once powered over half this country.

Now it trails two technologies that didn't exist at commercial scale 20 years ago.

The grid is changing faster than most predicted and it's only getting started, regardless of policy.

The sharpest signal that fossil fuel economics are broken? The petrostates themselves are building solar + storage. Abu Dhabi's Al Dhafra is delivering firm, round-the-clock power at $70/MWh, cheaper than the oil it sits on top of. Crises force a repricing of markets and further accelerate disruption.

Very telling even the world's largest petrostate knows the math has changed.

The new geopolitical energy map of the future will run through solar irradiance, grid infrastructure, and battery manufacturing.

If your national energy strategy depends on fossil fuel imports - You don't have an energy policy.

- Fossil Dependence: Price set abroad

- Domestic Renewables: Price set at home. Capital stays within the country. Supply physically uninterruptable.

We have entered the incredible new era of 24/7 firm renewable power, an industrial and sovereign inevitability. The economics are brutal for anyone holding fossil assets. Here's the raw data from the latest 2026 IRENA, IEA, and Ember reports:

THREAD

Very telling even the world's largest petrostate knows the math has changed.

The new geopolitical energy map of the future will run through solar irradiance, grid infrastructure, and battery manufacturing.

If your national energy strategy depends on fossil fuel imports - You don't have an energy policy.

- Fossil Dependence: Price set abroad

- Domestic Renewables: Price set at home. Capital stays within the country. Supply physically uninterruptable.

Oil is priced globally so a refinery outage in Houston moves prices in Manila. But solar is priced locally, permanently, and upfront. Once the panels are on the roof, the fuel cost is zero. Forever. No OPEC meeting changes that math.

This is the structural break. Prior energy technology like coal and gas still expose you to ongoing commodity or fuel costs. Solar is the first mainstream source where the capital expenditure is the energy expenditure.

Oil inventories are falling at the fastest rate in years, but the bigger story isn't today's stock draw. Every supply shock reminds the world why electrification, batteries and domestic renewable energy are strategically valuable. The less dependent an economy is on imported oil, the less vulnerable it becomes to events beyond its control.

Could this simply be cost curve gravity at work? Years of underinvestment, project delays and declining mature fields eventually show up somewhere. First inventories fall. Then prices rise.

The irony is that every oil price spike strengthens the economics of the technologies replacing it. Higher fuel prices inevitably accelerate EV adoption, EV trucks, rooftop solar, behind-the-meter batteries and grid-scale storage as households, businesses and fleets look for ways to reduce exposure to volatile oil markets.

For the first time in our industrial age, humanity has an off-ramp. Previous oil shocks left us with few alternatives. Today we can electrify transport, generate power locally and store energy at scale. Markets have a funny way of solving shortages: they accelerate disruption.

In one year, China added a Germany-sized grid's worth of electricity generation, and coal still fell.

The framing of "capacity additions" has dominated Western coverage for years, which is why so many people still think China is just building coal + solar in parallel forever.

Solar and wind have near-zero marginal cost. Once the capital is deployed, the “fuel” (sunlight and wind) is free. Coal has ongoing fuel costs, logistics costs, price volatility. When you're a grid operator choosing what to dispatch at the margin, you run your zero-marginal-cost assets first.

China has now built so much zero-marginal-cost capacity that it's structurally displacing thermal generation even without shutting a single coal plant. The plants still exist. They're just running fewer hours. That's why you can add coal capacity and reduce coal generation simultaneously, utilization rates are falling across the thermal fleet.

And it's only accelerating. Wright's Law: every doubling of cumulative solar production cuts costs ~20%. China manufactured its way down that curve faster than any country in history and is now reaping the dispatch economics on the other side. The capex is sunk. The marginal cost is essentially zero. Coal can't compete with free at the margin.

It's funny how you can explicitly say in your China power sector charts that you're talking about renewable power *generation* (not capacity), and you STILL get people commenting as if you're trying to mislead them.

Look at these numbers for a few years and you can see how China’s power system is shifting towards clean power at the level that actually matters (generation and dispatch), not just capacity build.

Anyway, I've been using this "China added a Germany of new electricity consumption last year" line in interviews for a few years now (it's been true every year). It pretty much always hits, because it's such a remarkable statistic (helped a bit by declining German consumption).

2025 was when I got to add for the first time the new line: "-and that net new demand growth was fully covered by incremental low-carbon generation". That is to say, China didn't just add an entire Germany of incremental power consumption; it added an entire Germany of incremental low carbon power generation. This is how power consumption can rise while power sector emissions are flat - or even decline.

On the back of that, last year, wind and solar rose to ~11% of generation apiece, with hydro contributing 13.8% and nuclear adding 4.6%, for just a touch over 40% non-thermal total.

The remaining ~60% was thermal power, split by roughly:

- Coal: 51.5% (down YoY)

- Natural gas: 2.8% (down YoY)

- Biomass, including waste-to-energy: 2.1%

- Other thermal (oil, industrial byproduct gases, and waste heat/low-grade fuels): 3.4%

So yes, coal generation dropped in both absolute terms and as a share of generation. You can keep adding new coal plants while still using less coal overall. We've been saying this for several years now.

So far, power consumption growth has been sluggish in 2026, which makes it easier to add enough new renewables to cover incremental growth. If renewable capacity additions stay strong enough this year to make this happen, it'll largely be thanks to the SOEs. The wind/solar project returns largely aren't there right now for the private sector, following the marketization reforms of last year.

My forecast is we'll see thermal power drop to ~57% of the mix in 2026 (or 55% fossil fuels if you subtract biomass). Gas dispatch is going to take a hit on the margin thanks to the higher LNG prices, and will likely be replaced by coal dispatch where possible, so I'm not yet certain coal's share will dip below 50% for the first time, but it should be close.

Correspondingly, non-thermal will grow to ~43%. The real key will be how hydropower does. It underperformed in 2025, but it's doing well so far this year *touch wood*.

In one year, China added a Germany-sized grid's worth of electricity generation, and coal still fell.

The framing of "capacity additions" has dominated Western coverage for years, which is why so many people still think China is just building coal + solar in parallel forever.

Solar and wind have near-zero marginal cost. Once the capital is deployed, the “fuel” (sunlight and wind) is free. Coal has ongoing fuel costs, logistics costs, price volatility. When you're a grid operator choosing what to dispatch at the margin, you run your zero-marginal-cost assets first.

China has now built so much zero-marginal-cost capacity that it's structurally displacing thermal generation even without shutting a single coal plant. The plants still exist. They're just running fewer hours. That's why you can add coal capacity and reduce coal generation simultaneously, utilization rates are falling across the thermal fleet.

And it's only accelerating. Wright's Law: every doubling of cumulative solar production cuts costs ~20%. China manufactured its way down that curve faster than any country in history and is now reaping the dispatch economics on the other side. The capex is sunk. The marginal cost is essentially zero. Coal can't compete with free at the margin.