What shows me “politics isn’t working”, to use Burnham’s phrase, is a welfare budget set to spiral from £313bn a year when Labour took office in July 2024 to an estimated £408bn by 2030 – 31pc more in a single Parliament.

Britain already spends more on welfare than we collect in income tax – with the fastest-rising part of this gargantuan bill now health and disability benefits for working-age adults.

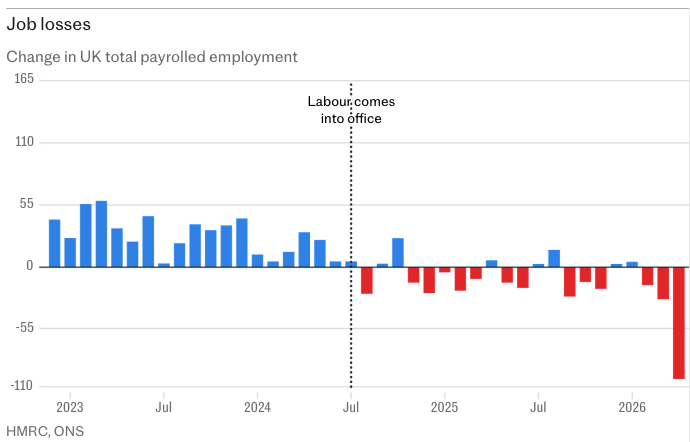

“Politics isn’t working” when the number of payrolled employees has fallen in 14 of the last 21 months, with job vacancies now at a five-year low. Labour’s sharp rise in employer national insurance contributions and two inflation-busting minimum wage increases are a punishing tax on jobs.

And with the government’s trade-union friendly Employments Rights Act now kicking in, countless firms have imposed a hiring freeze, with youth unemployment now at an 11-year high. What’s the point in over-zealous employment protection if you don’t have a job?

“Politics isn’t working” when UK firms are paying four times’ more for their energy than their US competitors and twice that in Germany and France, with British households also paying over the odds. Sky-high energy bills are seriously curtailing growth and enterprise.

Yet still, the powerful green lobby is bunged endless taxpayer-backed subsidies. And Ed Miliband’s insane ban on new North Sea drilling remains – the Energy Secretary’s dinner party boast costing Britain tens of billions of pounds in lost growth and hundreds of thousands of jobs.

🧵3/6

By their words ye shall know them:

Wes Streeting: If there’s a leadership contest I will definitely be a candidate.

He’s not running.

Keir Starmer: If a leadership contest is triggered I will definitely be a candidate.

He’s not running.

💥✍️ "When The Facts Change" Post

"Leading economists" finally admit the UK is on course for an IMF bailout ....

Where have they been for the past 12/18 months !?!!

If our careerist, complacent "economics establishment" had started speaking out earlier, clearly warning of the dangers of ever rising borrowing and spending, the UK might now be in a much stronger position ...

Instead, we are on the brink of a proper fiscal meltdown ...

Link to free-to-access "When The Facts Change" post below

Please like/share/subscribe to support quality independent journalism – journalism that matters

When The Facts Change: Economics and Politics in a fast-moving world, with Liam Halligan

https://t.co/p6UXQ71yMb

Jürgen Maier, Ed Miliband’s clean power tsar, has quit Labour’s flagship energy quango after just two years in the job. Mr Maier was appointed in 2024 to set up Great British Energy, which Labour’s election manifesto pledged would “cut bills for good” and create jobs “in every corner of the UK”.

Going well then, Ed...

#CostOfNetZero

No one elected Natural England, yet they are regulating us into a poorer country.

£700m to scare fish away, while your energy bills climb, you can't afford a home, & now they want the ponies off our moors.

Decisions made by people who never have to live with the consequences.

Labour risks being forced to seek emergency help from the International Monetary Fund (IMF) as Britain lurches toward a debt crisis, leading economists are now warning.

Former IMF chief economist Ken Rogoff says, in a new interview, that there is “more than 50:50 chance” of a major UK debt crisis before the end of this decade.

He is joined by Sir Charlie Bean, a former senior official at both the Bank of England and the Office for Budget Responsibility, who says the need for an IMF bail-out is now a “material risk” for the British economy.

I not only firmly agree with Ken Rogoff and Sir Charlie Bean – but have been repeatedly issuing the very same warnings for a very long time.

Because the grave risk of a major fiscal meltdown has been apparent for at least the last two years – to anyone who combines serious knowledge of UK economics and politics and global debt markets with an open mind.

The UK's public finances were already fragile when Labour took office back in July 2024.

But this government's misguided, ideologically-driven statist policies have made a bad situation much worse, seriously increasing the danger of a deep fiscal crisis - which would cause a disastrous state funding shortfall and a very nasty inflation spike.

That would result in Downing Street being forced to follow the orders of unelected technocrats flown in from Washington and elsewhere.

It would be a very major national humiliation combined with a deep economic slump and an even more intense cost-of-living crisis – in which low-income households, as ever, would suffer the most.

Yet those of us that have shown the brains and courage to point out these inconvenient truths over recent months and years have long been dismissed and derided for our trouble - not only by ignorant politicians and approval-seeking journalists but also the overwhelming majority of "leading economists".

Ahead of the general election in mid-2024, with Labour on course to win, the conventional wisdom among the great sages of broadsheet journalism and the economics establishment was that "the adults would soon be back in charge" ... Labour would "get lucky with the economy" ... and "Britain would now enjoy an extended period of political and fiscal stability".

I thought that was total nonsense – not least as I was well aware Labour's plans irresponsibly to increase borrowing and spending would be met with deep scepticism by the global pensions funds, insurance companies and other institutional investors that lend governments serious money.

My weekly @Telegraph "Economic Agenda" column of 23rd June 2024, a fortnight ahead of the general election, was a total outlier. I recounted the disaster of 1976 – when Britain was forced to go "cap in hand" to the IMF for a bailout – and warned that "The Ghosts of the 1970s" would haunt Labour's (so-called) economic resurrection".

Six months later, after the October 2024 "Hallowen" budget in which Chancellor Rachel Reeves did indeed sharply hike borrowing and spending, I assessed the market reaction then doubled-down – warning more assertively in my column of 12th January 2025 that "The UK risks a return to 1976 unless Reeves changes course".

And then again on 20th July 2025, as Labour's policies raised the costs of doing business, translating into price pressures which pushed up government borrowing costs even more, I again cautioned that "Inflation risks are taking Britain to the debt-crisis cliff edge".

"It’s now screamingly obvious that Labour’s crude Keynesianism – “pump priming” the economy by upping state borrowing and spending – isn’t working," I wrote in that column last July.

"Worse than that, this Government’s actions are pushing Britain towards a budgetary crisis every bit as serious as that in 1976 – when the UK was forced to go “cap in hand” to the IMF for a bail-out".

It's been a lonely task issuing these warnings. I've been hounded in public debates, slagged off by senior civil servants and often dismissed by "leading economists" as "alarmist".

So what do these same "leading economists" now say to Rogoff (Harvard Professor, Former IMF Chief Economist) and Bean (LSE Professor and Former Deputy Governor of the Bank of England)?

The "economics establishment" – with very few honourable exceptions, the brilliant @jagjit_chadha among them – has been and remains extremely reluctant to point out the deeply unsustainable nature of this government's addiction to ever more borrowing.

The systemic fiscal dangers of evermore "tax and spend" – and the prospect of a serious spike in gilt yields and related fiscal meltdown – are now so real and present as to be completely undeniable.

Yet the UK government is about to shift even further to the left, pushing up borrowing and spending even more under a new leader, in a bid to appease the massed ranks of economic illiterates among Labour's Parliamentary party and activist base – making those dangers even more acute.

Yet, still, the silence among "public intellectual" economists is deafening.

I'm glad the likes of Ken Rogoff and Charlie Bean are now issuing clear warnings. So where is the rest of the "economics establishment" - those who purport to understand fiscal management and financial markets, and often funded by taxpayers' money?

Britain is now clearly in the crosshairs of a very serious danger. The government's creditors are increasingly fickle and based overseas – with no regulatory or cultural obligations to lend money to the UK government.

Those holding UK gilts are increasingly "speculative" rather than "strategic" long-term investors – looking for quick returns, financing their government bond purchases with "leverage" (money borrowed from elsewhere), which will quickly be withdrawn when senitment decisively shifts, causing a plunge in gilt prices and a sharp additional surge in government borrowing costs, setting up a vicious circle.

The UK government is very heavily indebted – and the global investors we rely on to bankroll a huge slice of our state spending are alarmed that of the £132bn the government borrowed last year, no less than £110bn was spent on debt interest – as I wrote in a column on 17th May 2026, "As Labour lurches further left, the markets are calling time".

Global investors are alarmed the UK has consistently had the highest inflation in the G7 (which pushes up borrowing costs) and has easily the highest share of index-linked debt (which magnifies the burden of inflation on the state's balance sheet).

And they are deeply, deeply alarmed that when Labour came to power in mid-2024, the Office for Budget Responsibility was forecasting additional state borrowing of £323bn by 2029, the scheduled end of this Parliament.

But Labour’s runaway spending and growth-crushing tax rises mean that the same five-year borrowing forecast is now £583bn – 80pc higher. And still, the trade unions, MPs and Labour activists who will choose Starmer’s successor now want even more.

It is not too late to pull the UK back from the fiscal brink, to avoid the extremely painful and deep, lingering damage of being forced to go to the IMF and perhaps other multi-lateral creditors for a bailout.

It is not too late to avoid the inflation surge, the currency crash, the shocking blow to consumer and business confidence alongside the sky-high interest rates that will seriously whack our economy – or the perhaps even deeper damage of yet more of the British electorate losing faith in the ability of our establishment to manage the country in a manner that avoids imposing serious hardship on so many hard-working people simply trying to make their way.

But our political and media class needs to start acknowledging the economic and financial truth – that the UK government is borrowing and spending too much, taxation is now so high that it's hammering growth and employment, and that trying to finally get the economy moving by "moving further left", borrowing and spending even more, will result in a fiscal collapse.

Smart, experienced, high-profile economists need to start speaking out – as Rogoff and Bean just have – raising the alarm in a bid to force the broader establishment to face reality. Before it's too late.

If you've read this far, you clearly think this analysis is worthwhile and important. So please like and share.

And for more, read my "Economic Agenda" column in The Sunday Telegraph each week – and subscribe to "When The Facts Change: Economics and Politics in a fast-moving world, with Liam Halligan"

Good morning Liz.

You seem to be unaware of a few things. Let us help you out here.

⚫️ As an EU member, around 27% of types of goods were able to be imported into the UK from fellow WTO members without a tariff applied - from outside the EU that level is now over 50%

⚫️ Food inflation since Brexit has been *lower* in the UK than it has in the EU, so food is cheaper in the UK

⚫️ As for the NHS, the NHS budget has been increased by over £750 Million a week since we left the EU

⚫️ As for UK global trade, the UK has trade deals in place with over 100 countries around the world, many of which are on the same or better terms than the EU had or indeed has

⚫️ In 2016 the UK exported a total of £582.6 Billion worth of goods and services - in 2025 that had increased to £930.6 Billion

You continue to talk about a topic that you appear to know absolutely nothing about - or perhaps you do, and so you simply lie to your followers in the hopes that they are too blinkered to fact check you.

Perhaps you could confirm whether it is ignorance or deceit that drives your posts of continued misinformation.

There's an increasing amount of bad press about Labour's management of the economy

(via @CityAM)

https://t.co/8akSSBChVk

https://t.co/2vKyp3eSiN

https://t.co/QdCgstSBQS

WOW!!

Huge new business win for #OCDO

Providing a technically advanced and multi-dimensional platform to enable @ASDA improve their online grocery business

[There's more news coming soon, as well]

@CheltenhamBC Why are you attempting to stifle retailing with your new policy to remove all A-boards outside shops and hospitality businesses in the town?

What is the point?

Bricks & mortar businesses are already disadvantaged and you want to make it harder for them

@SatoshiPay@Vortex_Fi Forgive me, but this looks like a failed project. When can we expect to see an improvement, with some genuine money feeding through the system? Or, is it all in the past?

Treasury quoted as saying plans on food tariffs would save consumers £150m per year. About 30m households. So a saving of 10p per week per household.

Not to say it’s a bad policy. But the politics of giving impression it’ll make a noticeable difference? https://t.co/WTGWGC6gEm