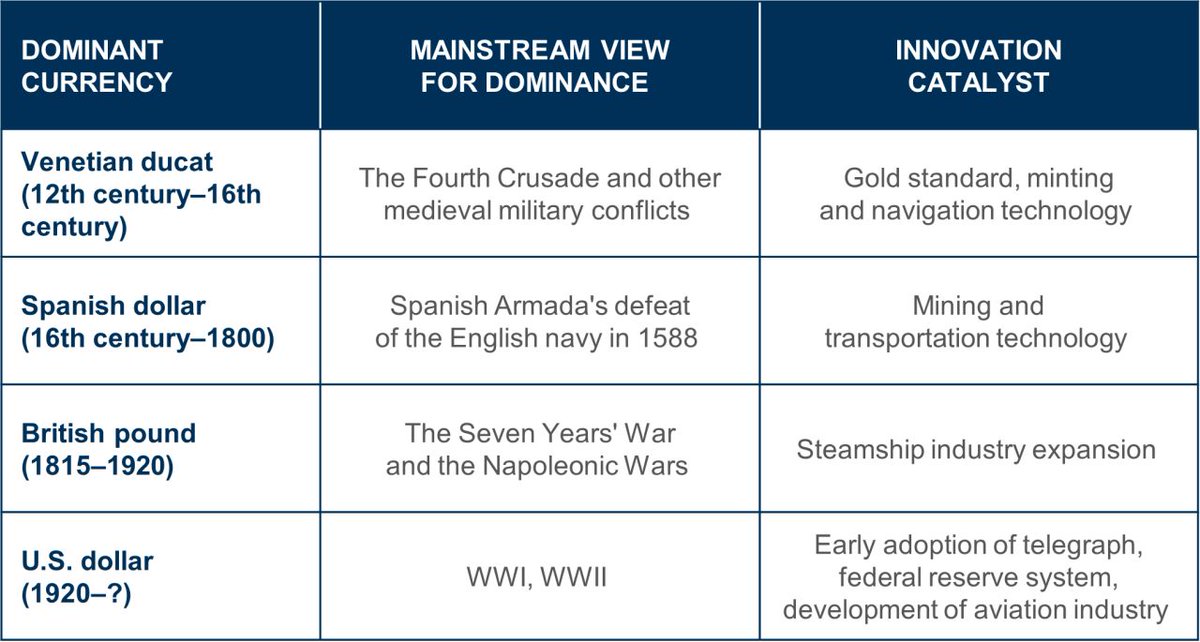

USD is not just a currency - it's a technology.

As history has shown, currencies are displaced by superior technology for moving value.

Stop watching the geopolitical horse race. Watch the infrastructure layer. That's where reserve currencies are actually won and lost. #stablecoins #rwas

For our team's full report: https://t.co/QH5buVrmAI

@sonyasunkim Applying credit judgment to borrower selection mirrors how traditional credit markets developed, not just purely price-driven. Great step towards broader institutional adoption. Congrats @sonyasunkim and team!

@TokenizeThisNYC Great work team! Congrats on getting more traditional institutions in the room; like the panel @hey_elizabethy participated in. Looking forward to next year.

@centrifuge@NYLIManagement Infrastructure is never finished. It will change. Parts will be ripped out. Some decisions will prove wrong.

Can’t go wrong when optimizing for better investment outcomes for clients remains the goal.

We’re proud to partner with @centrifuge as we take an important step in @NYLIManagement's tokenization journey.

For more than 180 years, we have remained focused on our commitment to long-term investment outcomes over short-term noise. This is bedrock and will not change. #Tokenization is the infrastructure that lets us keep serving our clients for the next century.

Thank you to @itsbhaji, @anemoyanil and the entire team, who have been exceptional partners to me and @hey_elizabethy as we worked through this project.

More to come and excited for what's next.

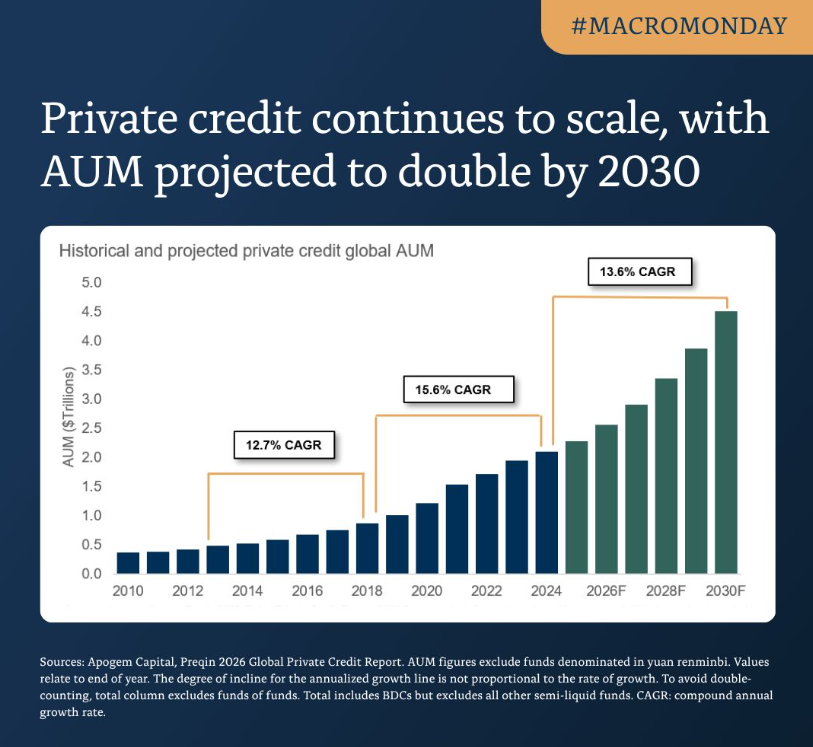

In this week's #MacroMonday, my team discusses why private credit will be defined by manager selection and not asset class exposure in a maturing credit cycle.

The fundamentals are still healthy. Default rates modest. Interest coverage improved. Borrowing stable.

For 15 years, rising AUM and a benign rate environment meant almost every manager looked good. The winners going forward will be defined by:

→ Quality of origination — not just deal flow volume

→ Underwriting discipline through the cycle

→ Workout capability when credits stress

→ Stable capital — no forced selling at the wrong moment

→ Lower middle market exposure — less crowded, stronger lender protections

Full report below:

https://t.co/JN7PFAaHrG

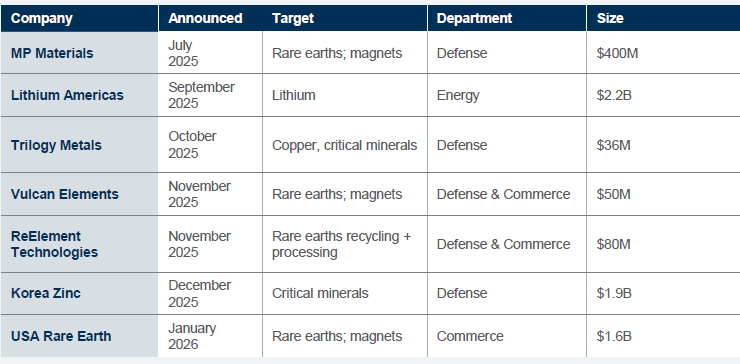

In our team’s latest geopolitics paper, we argue that most investor portfolios are built for a world that no longer exists. Most portfolios were built for a globalized, U.S.-led, rules-based order where capital flowed freely, supply chains optimized for efficiency, and geopolitics was background noise.

A fragmented, security-first world replacing it has profound implications for every portfolio — implications most investors can't position for on traditional financial rails.

This is where the #blockchain becomes a structural answer. #Tokenized real assets, infrastructure, and credit across geographies give investors exposure to the defense buildout in Europe, the critical minerals story in the Americas, the nearshoring opportunity in EM.

🇺🇸 U.S.: no longer just setting the rules. It's writing checks and taking equity stakes. Critical minerals have shifted from a commodity cycle story to a strategic-capacity story. Policy is now part of the capital structure.

🇩🇪 Germany: €100B modernization fund. EU defense at €381B in 2025. Rearmament is now industrial strategy.

🇪🇺 Europe: EU-India trade deal (Jan 2026) = building a non-China, non-U.S. channel. Trade is now risk management.

🇯🇵 Japan: Doubling defense to 2% of GDP. JGB yields moving higher as security spending replaces ultra-easy policy.

🇨🇳 China: U.S. exports fell from 7% to 2% of GDP since 2006 — deliberate. Gold accumulation at record pace. mBridge = payments outside the dollar.

🇲🇽 Nearshoring. 🇹🇷 Steel dome defense. 🇮🇩 60% of global nickel — export restrictions forcing processing onshore.

Full report below:

https://t.co/6RWPVidYBX

Here is another inflation risk factor I don't think the market has fully priced in yet - 2026 Super El Niño

Iran conflict disrupted fertilizer supply. Now a Super #ElNino is forming on top of it.

→ Two independent supply shocks

→ Same crop cycle

→ Same 2026–2027 window

This is supply-driven inflation that monetary policy can’t fix.

🌡️ What @NOAA says:

→ 90%+ probability El Niño arrives Jun–Aug 2026

→ 1-in-3 chance of a very strong event by year-end

Peak pain in 2027 given 6–12 month production lag, with the most exposed being:

🔴 Sugar: India & Thailand production -20–30%

🔴 Cocoa: West Africa drought risk

🔴 Palm oil: Southeast Asia dry conditions

🔴 Wheat: Australia down ~9M tonnes in 2026/27

🔴 Rice: Indian monsoon failure risk

The fertilizer double hit:

→ Urea prices doubled since Iran conflict

→ U.S. imports 90% of its potassium

→ Hormuz carries 1/3 of global fertilizer trade

If the FAO food price index rises 50% by year-end ➡️ G7 food inflation hits double digits in 2027.

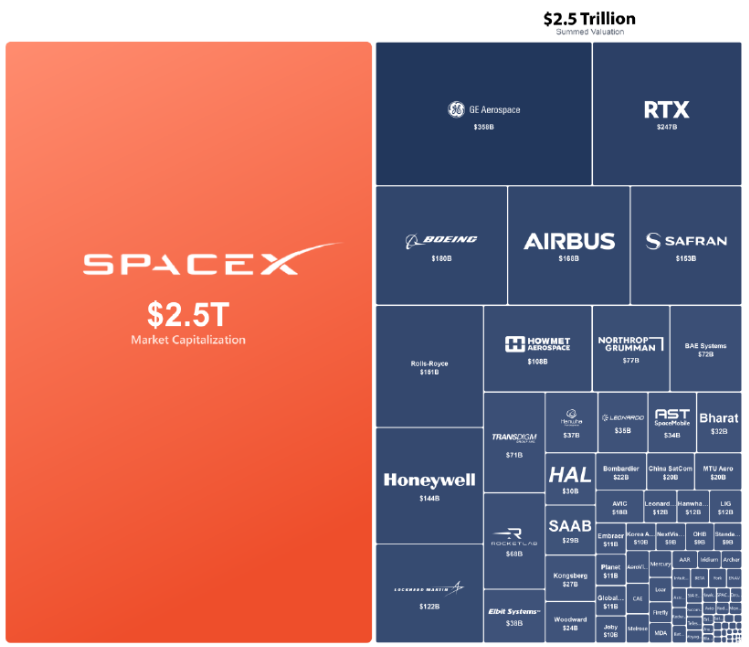

SpaceX: $2.5 trillion. The entire global aerospace & defense industry combined: $2.5 trillion. Compunded conviction + patient capital.

Credit to @Macro_Mike_ for interestign chart.

Over the past two decades, companies have chosen to stay private longer, shifting a larger share of value creation away from markets the general public can access.

↘️Public markets shrank by 42% ↗️Private markets grew by 512%.

#DigitalAssets

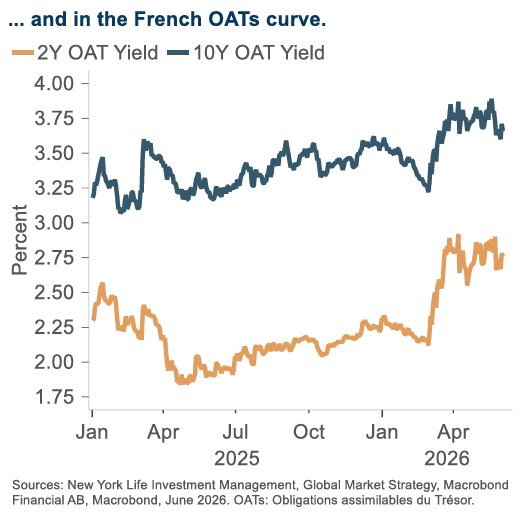

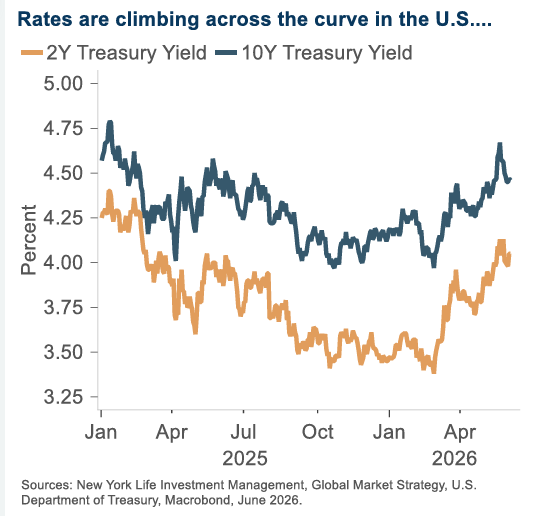

Global long rates have risen meaningfully, but short rates have seen a larger move – meaning that global yield curves have flattened, as the market focuses on near-term upside inflation risks over downside economic risks.

We believe a Treasury bear steepener effect is most likely, as demand destruction is baked into near-term policy and rate expectations.

Among other developed markets, we expect the bear flattener effect to persist as major central banks, including the ECB and BoE, enact rate hikes as early as June.

Link below for or our team's June outlook across all public and private asset classes:

https://t.co/QH5buVrUqg

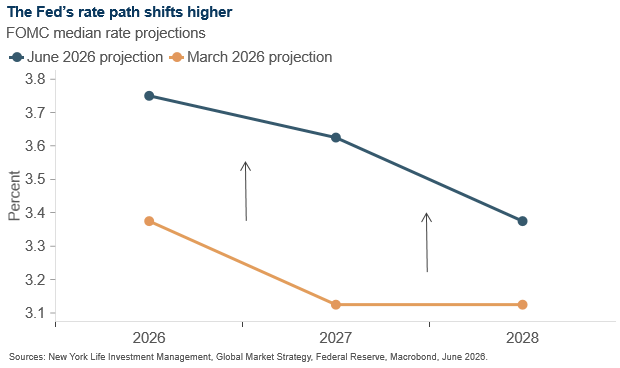

While Kevin Warsh forged a decidedly dovish path to Fed Chair, today’s meeting was decidedly hawkish.

The June SEP showed a more hawkish path for rates, with the median dot now implying one hike in 2026 and two cuts in 2027.

The vote was 12-0 in favor of no change but the view on year-end policy was split, with 9 of 18 members projecting at least one rate hike, 8 projecting rates on hold, and one in favor of a cut.

That level of disagreement reinforces that the committee is no longer debating a clean easing cycle.

First Warsh FOMC today. Everyone’s watching rates, but watch the balance sheet as well.

Hold today is the likely outcome. But the balance sheet is a slow-burning inflationary force that no rate decision resolves.

Chart 1: QT is over

Balance sheet stabilized at ~$6.5T. The Fed stopped draining liquidity. That’s dovish — and inflationary. $2.3T in MBS still on the books suppresses mortgage rates, keeps housing demand elevated, and feeds directly into shelter CPI.

Chart 2: Reserves at “ample” — not “abundant”

Bank reserves down from $4T to ~$3T. The Fed is approaching the floor. Go lower and you get 2019-style repo chaos. This is a hard constraint on further tightening — regardless of what inflation prints.

The Fed can’t hike aggressively ➡️ funding stress

Can’t restart QT ➡️ same risk

Can’t normalize the balance sheet ➡️ mortgage market collapses

Our team's full report below:

https://t.co/QH5buVrUqg

Three cash-flow-negative AI companies entering an already concentrated, high-valuation market will test investor conviction and market liquidity.

AI and infrastructure companies have become market-defining businesses while remaining largely inaccessible to public markets. Companies have chosen to stay private longer, shifting a larger share of value creation away from public markets.

When companies this size enter passive indexes, forced selling begins. SpaceX's Communication Services classification means Meta and Alphabet face mechanical selling pressure to make room.

Watch bitcoin and Tesla as the early pressure valves. If they crack around the IPO window, speculative capital is being rotated, not added.

Our team's #MacroMonday report below:

https://t.co/VrbTZKMa9s

Cash has lost yield potency, driving a clear incentive toward buy-and-hold total return opportunities in credit.

Saying again➡️ buy-and-hold total return

- The credit cycle is healthy today, but macro risks have risen and the credit cycle has matured. We also expect ongoing yield curve volatility. Our “solve” for both concerns is to stay short duration across credit types in the U.S.

- Upside risks to long rates remain: we are staying on the short side of neutral in duration, seeing buying opportunities above a ~4.6% threshold on the 10Y yield.

- We prefer to balance short duration Treasuries, convertibles, and corporate credit exposure with longer duration in securitized credit, where we see long-end exposure as better rewarded.

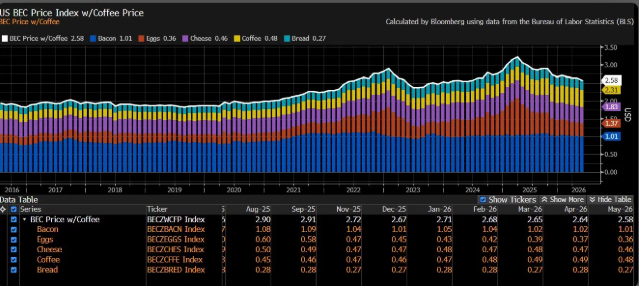

Here is a relatable inflation indicator - the Bacon Egg & Cheese w/Coffee Index. You don’t need a CPI report to feel inflation, just make breakfast.

Markets largely looked through the inflation print, with Treasury yields little changed following the release.

Attention now turns to next week’s FOMC meeting where policymakers will weigh the highest inflation print in three years against a resilient labor market.

In the coming months, we remain focused on second-order inflation effects, specifically whether higher energy prices will feed into transportation and other energy-intensive categories, ultimately pushing core inflation higher.