Although we don’t yet have the details about the motives behind last night's shooting at the White House Correspondents Dinner, it’s incumbent upon all us to reject the idea that violence has any place in our democracy. It’s also a sobering reminder of the courage and sacrifice that U.S. Secret Service Agents show every day. I’m grateful to them – and thankful that the agent who was shot is going to be okay.

We sold Shelly after:

1) Change of accounting principles

2) More details on the incentive program

which looks bad in combination with our belief there was a buildup of inventory at the distributors. Jury is still out, likely no fundamental problems but better options elsewhere.

$SLYG

1 - The right way to calculate days of sales outstanding (DSO) is to compare accounts receivables (AR) with sales of the period that generated the AR. In a company with sales split relatively evenly between quarters, you can calculate DSO almost any way you like. For a company like Shelly that is growing rapidly with sales heavily concentrated in Q4, you must take care to match AR with the sales from the period that generated the AR. If you calculate DSO based on the last 4 quarters, you get a huge jump in Q4 2025 which is very alarming.

If you take care to match the AR with the relevant sales period, DSO calculated on the last two quarters of sales increased much less dramatically by 13 days to 129 in Q4 and importantly did not follow the usual seasonality of decreasing DSO in Q4. This is a yellow flag.

With just two pieces of information, future return on capital and earnings growth, I can calculate the free cash flow. The free cash flow discounted to present value is the true value of a company today.

In other words, future return on capital is crucial for value creation. Unfortunately, the common return on capital ratios such as return on equity (ROE), return on assets (ROA), and return on capital employed (ROCE) and return on invested capital (ROIC) have a number of problems.

ROE, ROA, and ROCE are so simplistic that the same company yields different results depending on the company's history, accounting practices, and financing choices. I think that's a major problem for a ratio where one of the most important purposes is to compare across companies.

ROIC is great in theory but difficult to calculate in practice. ROIC has no universally accepted calculation method, which makes the ratio hard to use as a common language.

I think the best ratio is return on net tangible assets (RONTA), a measure that is consistent across companies and relatively easy to calculate. RONTA is a good starting point for predicting the future return on organically invested capital.

If you'd like to hear more, I've made a YouTube video where I walk through it all in 12 minutes — the underlying problems with ROE, ROA, ROCE, and ROIC, and why RONTA is the most useful return on capital ratio.

https://t.co/I7RadFRFkT

Thank you for replying to my points.

1 - On the DSO calculation.

The trend is the same, but the magnitude is very different and magnitude is very important for the interpretation.

2 - On the maturity table

Overdue receivables are a very serious problem. Long credit terms may be a problem.

3 - On Cloud Activations

Sell through to end customers is the most important number and can cast the lacklustre cashflow in very different light.

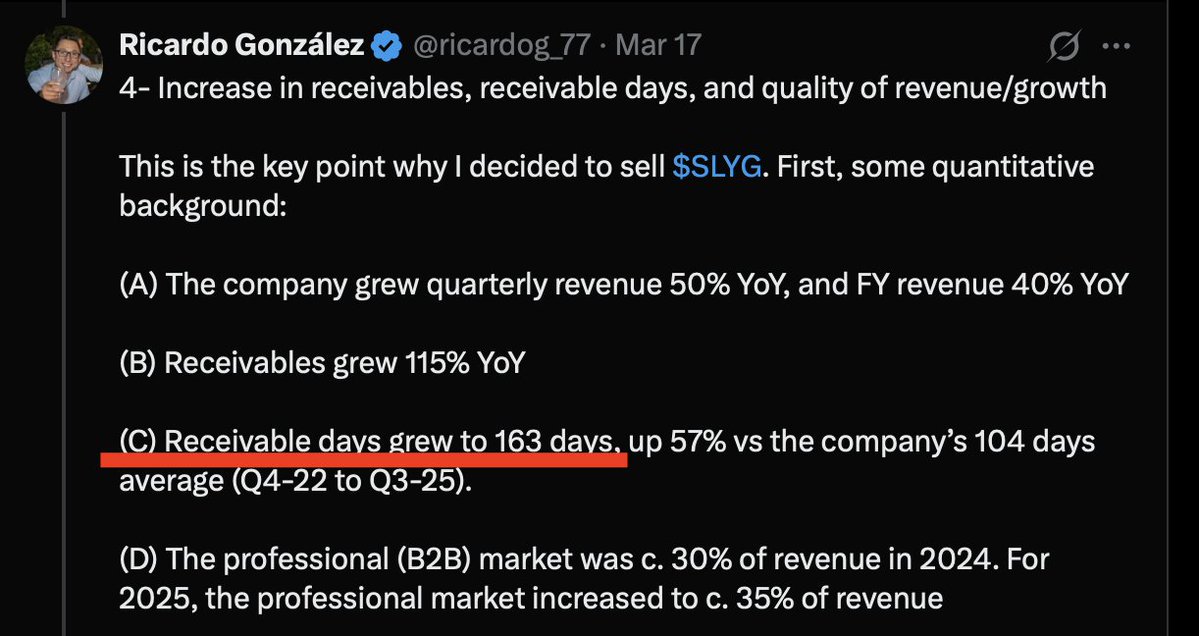

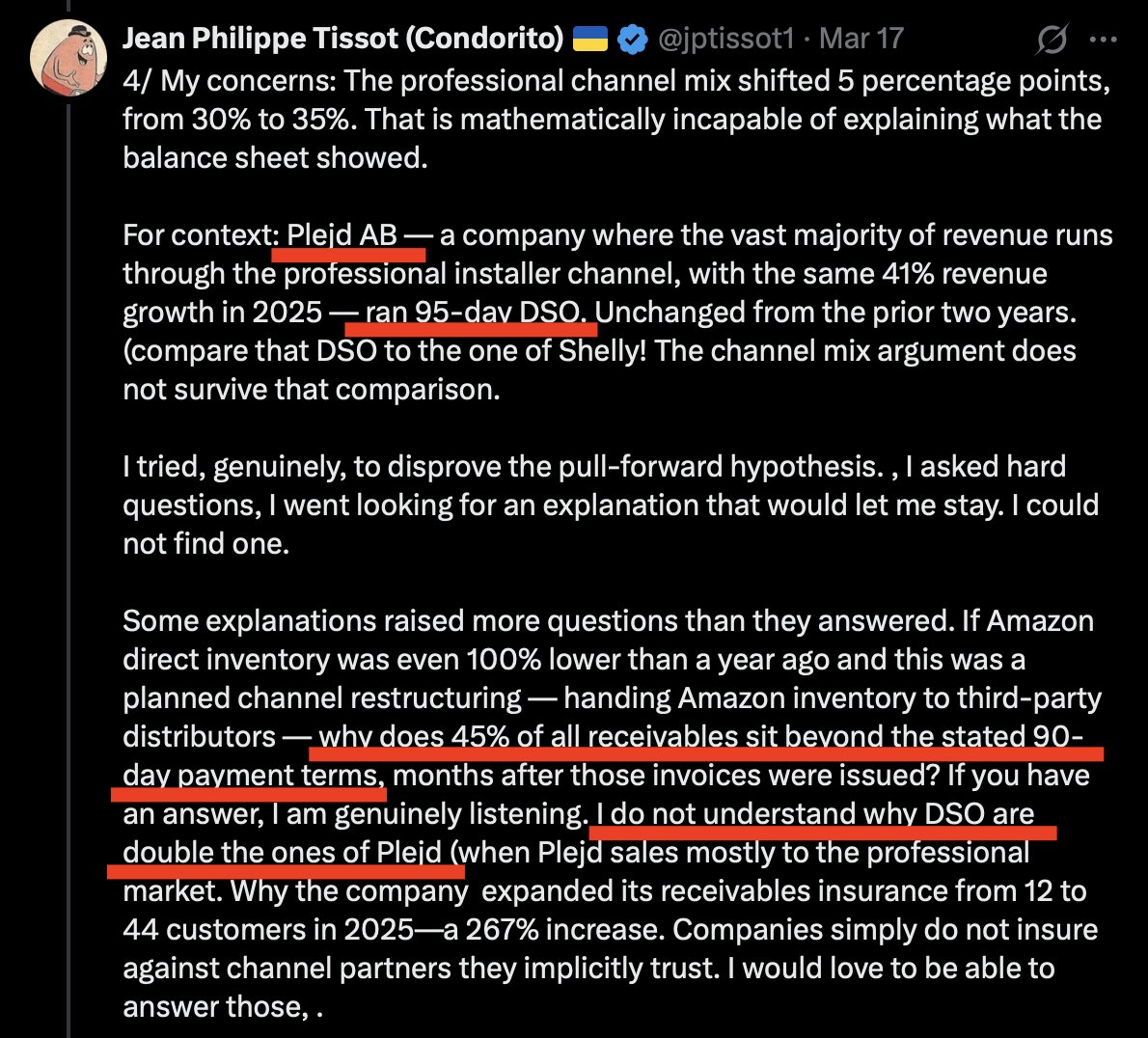

4 - DSO Shelly Plejd comparison

Clear communication is key, both for companies but also for investors, especially those who speak in public and may move share prices.

Shelly's communication could be a lot better on the expanding credit terms and growing receivables. However they literally said credit terms could be 90-150 days in the Q4 conference call, consistent with a DSO of 129. Don't get me wrong, I still think it is a yellow flag with a final verdict that depends on many factors including the rate of growth in DSO and sell through to end customers to name two.

Bob Mueller was one of the finest directors in the history of the FBI, transforming the bureau after 9/11 and saving countless lives. But it was his relentless commitment to the rule of law and his unwavering belief in our bedrock values that made him one of the most respected public servants of our time. Michelle and I send our condolences to Bob’s family, and everyone who knew and admired him.

5 - Additionally, it looks like you are misinterpreting Shelly’s information on expected future payments, framing it as ageing receivables. The 3-6 months receivables are not aging, it is likely the youngest receivables, being recently invoice with a payment term of +90 days, consistent with a DSO of 129 days.

I think these are honest mistakes and I suspect no ill intent. Q4 did contain some real negative information which should be weighed against all other relevant information about Shelly. MediumInvest own shares in Shelly.

4- While I agree with @jptissot1 and @ricardog_77 on the direction of their interpretation of Shelly’s Q4, I find the DSO based on the last two quarters to much better reflect the underlying reality.

Recalculating Ricardo’s and Jean’s DSO vs. what I find to be correct:

Ricardo:

Ricardo’s DSO of 163 days is consistent with using the real AR of 132,7 and four quarters of sales 292,9: 132,7/292,9*360=163 DSO.

Jean:

Jean does not explicitly state Shelly’s DSO, but he does state it is the double of Plejd’s and states Plejd’s at 95, implying a DSO of 190 days.

The only way I can get to a number in that range, is if I use the high-level receivable numbers from the top of the Q4 report, including both the real AR of 132,7 and advances to suppliers of 21,1 divided by 12 months of sales. (132,7+21,1)/292,9*360=189 DSO.

My take:

133 / (123+64)*182 = 129