One of the things I appreciate about Jay Chaudhry of Zscaler is his blunt quality and absolute tenacity in defending his company. “Totally wrong” is refreshingly direct to hear from an interviewee.

Zscaler CEO: ‘Investors don’t appreciate the platform we have built’

Cyber-security software giant Zscaler’s stock plunged 32% on Tuesday, and CEO Jay Chaudhry sat down with me to explain some of the notions people have about the company that are “totally wrong” in his view. His company is still “best in class” in cyber-security, he points out. Rumors of increased competition from the likes of Fortinet and Check Point aren’t true at all, he says. And as for AI “agents,” if even a handful of Fortune 500 firms start rolling out the stuff, it can meaningfully add to Zscaler’s revenue.

https://t.co/mIUIvlVmxr

$ZS

@zscaler

$PANW

$FTNT

$NTSK

$CHKP

At mid-year, the TL20 is up 70%, well ahead of the 17% of the Nasdaq. The TL20 has been more heavily weighted to Micron Technology of late, which has seriously outperformed Nvidia, thus contributing to market-beating gains.

This is not AI-based stock picking. This is knowing about tech companies and markets and stock valuations based on years of experience.

Subscriptions to the newsletter are $1 a week for the first four weeks.

https://t.co/mIUIvlVUmZ

Jensen Huang’s Nvidia is looking pretty good with his company’s $2 billion stake in Marvell after Huang sang the company’s praises at Computex. The double-dealing in the AI market, with companies taking stakes in vendors and then talking up those companies’ stocks, is rather remarkable.

Nvidia’s Huang pumps Marvell stock but consider the alternatives

Name-dropping about Marvell Technology by Nvidia’s CEO sent its shares soaring but here there are other things to consider in networking and fiber-optics such as Lumentum and MaxLinear. Also, the Street is underestimating ASML’s growth — possibly by a wide margin.

Subscriptions to the newsletter are $1 a week for the first four weeks.

https://t.co/mIUIvlVmxr

$NVDA $MRVL $AVGO $LITE

When you make promises well in excess of what you’ve delivered or can provably deliver, that’s slide-ware. Whether it’s Google warning of a quantum-crypto doomsday, or a roadmap from a vendor such as D-Wave that has plans to have a machine six years in the future, we’re living in an age of quantum slide-ware.

D-Wave’s gate discussion brings more quantum slide-ware

Quantum computing hopeful D-Wave on Monday talked up its roadmap to a hundred “logical” qubits’ worth of gates in 2032. The fact is, it’s still slide-ware, and there is as yet no proof they’ll hit their targets on time nor that it will add up to a very valuable machine by then. Among “boutique” stocks, I’d rather buy ASML.

https://t.co/mIUIvlVUmZ

$QBTS $IONQ $RGTI

The entry — again — of Nvidia into the PC processor market is not as earth-shattering as is being branded. It remains to be seen if enough AI “agents” actually show up in enterprises to make it matter. But if they do, it could make capitalism obsolete, according to Deutsche Bank.

Nvidia, Intel, Dell and the microprocessor craze

The entire personal computer “complex” is getting a lift Monday as Nvidia announced a new PC microprocessor. Frankly, the enthusiasm is a little overblown, in my view. Intel and AMD trade lower on the news. Also, favorable views on recently public Rare Earths Americas, and following where the AI money comes from and where it goes.

https://t.co/mIUIvlVmxr

$NVDA $DELL $INTC $AMD $MU $WDC $SNDK

Unbelievable numbers from Dell tonight. An 88% jump in revenue, year over year, at $44 billion. And more of the same promised this quarter. The company’s forecast three months ago didn’t come close, nor did the Street. This is unlike anything we’ve seen from Dell in years. Some giant AI companies just ordered a lot of servers. And Dell was actually able to ship them.

Dell soars: Enormous revenue upside, and profit, too

Dell’s shares surged 17% as the company said it is going to have $60 billion worth of AI server sales this fiscal year. Its first-quarter revenue blew away both the company’s own forecast and Street consensus. And the surge in profit is even more surprising, putting to bed worries about erosion from low-margin AI servers. And it looks like the good times will keep rolling this quarter and beyond.

https://t.co/mIUIvlVmxr

$DELL

$INTC $MU $AMD

The software analysts have been desperate for some company to offer up a thing they could point to that says that packaged software will survive and maybe even thrive in the AI future. The Snowflake “Cortex Code,” dubbed CoCo, has handed the bulls what they wanted. It is being celebrated as a pivotal development. Mind you, it has 7,100 accounts in total using it, and we don’t actually know how much money Snowflake makes off of it.

Hallelujah! Street gaga for Snowflake’s ‘CoCo’

One tool for “agentic” artificial intelligence at Snowflake has suddenly ignited the passion of Street analysts, driving Snowflake stock up over thirty percent in early trading and sending price targets zooming. It’s a little too soon to declare victory, but it seems to be resonating as a sign software can survive.

https://t.co/mIUIvlVmxr

$SNOW

ZScaler plunges as software still struggles

Software continues to be challenged as Zscaler’s sales effort struggles, and Workday’s new stuff for AI has yet to “move the needle,” as they say.

Software’s problems exist at the margins, where individual companies are being picked apart, within an overall terrible climate sentiment-wise. Tuesday’s results for Zscaler were not enough, and for Workday, fear of seat-license losses still weigh. Tonight’s reports from Nutanix and Salesforce are mildly encouraging, and Snowflake is surging over 30% on what is being viewed as a “solid” report.

Tune in tomorrow when I once again speak with Nutanix and Zscaler CEOs about the results and outlook.

https://t.co/mIUIvlVmxr

$SNOW

$NTNX

$ZS

$WDAY

$CRM

There are not a lot of signs of agentic AI ramping into production at normal companies so far. There is a lot of boosterism from tech companies about agentic AI. Without trillions spent on agents by enterprises, the whole thing could come crashing down…

Kudos to Tavis McCourt of Raymond James for a stimulating read.

The AI spending boom must face the external credit risk in 2027

Starting next year, probably, a lot of the incremental financing for the artificial intelligence boom will come not from the cash flow of cloud giants as it is now but from external sources, the kinds of professional investors who scare easy. If AI revenue doesn’t show up as expected, this could be the DotCom bust or the Chinese property bubble or the sub-prime mortgage implosion all over again.

https://t.co/mIUIvlVmxr

$MU $NVDA

I have been writing for years that Micron Technology is one of the most valuable companies in all of semiconductors, perhaps all of tech. The upward revisions happening for the DRAM market, and possibly NAND, are astounding, and beyond even what I expected. But it is in line with my thinking that the business is becoming less of a commodity business over time, which naturally leads to higher valuations. Micron is now the best performer of the TL20, up over 1,200% since 2022.

Micron in the trillionaire’s club: value it like Nvidia?

UBS suggested Micron Technology stock should trade much closer to Nvidia’s stock multiple given the durability of agreements Micron has worked out with its DRAM customer, driving shares up over 20%. The key seems to be the cloud giants and their insatiable demand for memory. The result is almost like a DRAM cartel but without the cartel.

https://t.co/mIUIvlVmxr

$MU $NVDA

Please enjoy my interview with Amkor CEO Kevin Engel, who has big plans for chip packaging in the Arizona desert.

Amkor CEO: ‘Semiconductors are going to continue to thrive’

Amkor is a fifty-eight-year-old purveyor of a once-humdrum technology called chip packaging that is suddenly hot in the AI age. CEO Kevin Engel expects that regardless of “fluctuations” in the AI market, semiconductors’ importance is only headed higher. He’s investing $7 billion of the company’s money to build new factories in the desert based on the need of customers such as Apple to make bigger and bigger chips for all sorts of things.

https://t.co/mIUIvlVmxr

$AMKR

Does anyone believe SpaceX actually has an addressable market of $28.5 trillion? Does this not seem like something created out of whole cloth in order to have a “wow” factor? Does this not seem like the Twitter version of a prospectus, unhinged from any responsibility for sober disclosure?

The TL Podcast for May 25th: IPO mania

Elon Musk’s SpaceX claims the largest market in history, $28.5 trillion annually — someday. Who knows if they’ll ever get there, as the xAI business is merely a money pit at this point. But the SpaceX IPO, and the expected offerings of OpenAI and Anthropic will certainly be bought in a big way, and they will steal some thunder from Nvidia and the other normal stocks.

https://t.co/mIUIvlVmxr

@SpaceX

Sometimes the hyperbole gets the better of us. Jensen’s furious pace on the conference call is vintage Jensen, but also a little over-heated and at times confusing. The results speak for themselves, however. The company’s business continues to be stellar.

Nvidia’s slightly bizarre conference call doesn’t diminish the stock’s tremendous value

Nvidia CEO Jensen Huang’s extended disquisition about the re-classification of revenue was a strange false note on the Wednesday conference call. But, no matter. Even without any multiple expansion — and Nvidia stock is dirt cheap at twelve times sales and twenty-two times earnings — the shares will appreciate simply because of the awesome growth. Oh, and bigger dividends and buybacks will draw more income investors.

https://t.co/mIUIvlVmxr

$NVDA

Sometimes the hyperbole gets the better of us. Jensen’s furious pace on the conference call is vintage Jensen, but also a little over-heated and at times confusing. The results speak for themselves, however. The company’s business continues to be stellar.

Nvidia’s slightly bizarre conference call doesn’t diminish the stock’s tremendous value

Nvidia CEO Jensen Huang’s extended disquisition about the re-classification of revenue was a strange false note on the Wednesday conference call. But, no matter. Even without any multiple expansion — and Nvidia stock is dirt cheap at twelve times sales and twenty-two times earnings — the shares will appreciate simply because of the awesome growth. Oh, and bigger dividends and buybacks will draw more income investors.

https://t.co/mIUIvlVmxr

$NVDA

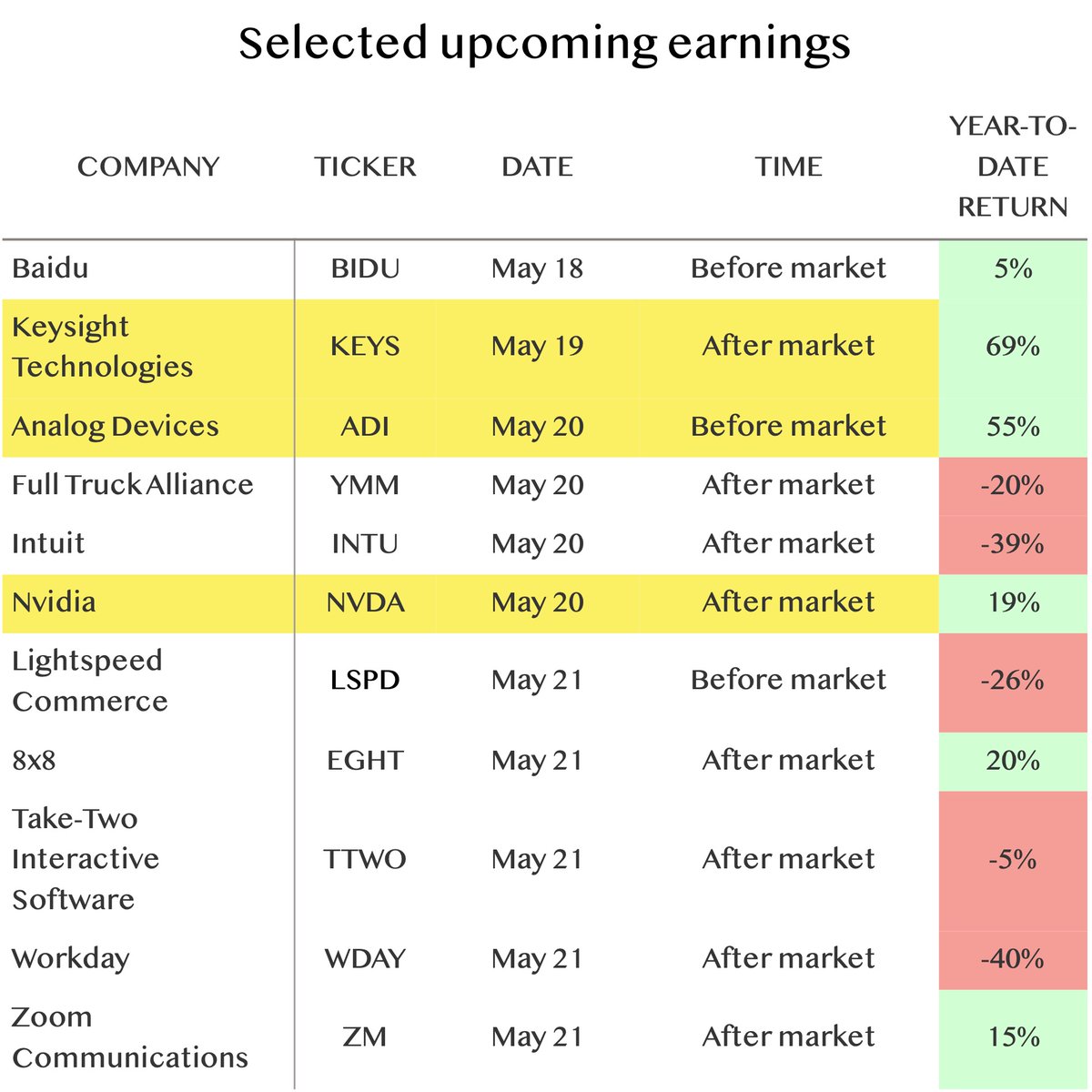

The threat of rising rates notwithstanding, the trends continue to be favorable for the most established tech companies linked to the AI trade, including Analog Devices and Keysight, and some stocks that have come to be value stocks such as Nvidia. Here are some thoughts ahead of their earnings this week.

Nvidia, Analog Devices, Keysight dominate by stability

They are not the most flashy names in AI these days, but Nvidia, Analog Devices and Keysight have much to recommend them, both this earnings week and in general. Also, CoreWeave and Nebius are set to “taking a breather,” and Zscaler can withstand competition.

TL is $1 a week for the first four weeks — the most economical way to stay up to date on the day’s tech-stock developments, every day of the week.

https://t.co/mIUIvlVmxr

$NVDA $ADI $KEYS

Congrats to Andrew Feldman and team at Cerebras as the stock opens its first day of trading. A fine outcome for a decade of hard work. Stock has opened almost double the offer price of $185 offer, and gone as high as $386.34. I would estimate a future market capitalization of $121 billion based on a 12.8 multiple of sales if the company can somehow put together $9 billion in revenue next year from OpenAI. That’s a big if, of course. But that could yield a price of $563, I estimate.

Cerebras opens at $350: Price target $563 or bust

Shares of chip maker and AI hosting provider Cerebras Systems on Thursday opened for trading at almost double the offer price of $185. If Cerebras can actually get billions in revenue from main customer OpenAI, and if they get a stock multiple comparable to that of CoreWeave or even Nvidia, that could yield a stock price of $563, well north of the IPO. There are a lot of ifs in there, and the whole thing could still come crashing down.

https://t.co/JvCpg81JCP

solana:4yEjcMiy6GAgrpWpUvhUXfaP1vQmJXfqJjEyxBSZpump

Cerebras: Price target $563 or bust

Congrats to Andrew Feldman and team at Cerebras as the stock heads to the open of the first day of trading. A fine outcome for a decade of hard work. Stock has been indicated to open way above the $185 offer, perhaps $400 or more. I would estimate a market capitalization of $121 billion based on a 12.8 multiple of sales if the company can somehow put together $9 billion in revenue next year from OpenAI. That’s a big if, of course. But that could yield a price of $563, I estimate.

@cerebras

solana:4yEjcMiy6GAgrpWpUvhUXfaP1vQmJXfqJjEyxBSZpump

Please enjoy my interview with Dynatrace CEO Rick McConnell.

Dynatrace CEO: Pursuing large deals with AI giants

Dynatrace CEO Rick McConnell says his company is working on deals with the largest AI companies. That’s not a promise, but there seems a reasonable chance they can ink some kind of very large commitment down the road. If and when that happens, it could be a “catalyst” for shares currently trading at a rock-bottom valuation.

https://t.co/mIUIvlVmxr

$DT