High praise from an absolute legend of the game.

The distance between predicting the future and executing the trade is the widest chasm in finance.

It is purely psychological.

It may be the hardest pursuit there is.

Bridging that gap is the lifelong work.

@kindwombat Hi Strata, it speaks to tight credit / liquidity conditions. Simply put: if mega-caps need to sell stock to raise money, money may be becoming scarce. There is also a historical precedent of this scenario playing out poorly since 1929.

— CW24 WEEKLY MACRO EDGE —

BASE CASE: A market that is broadening, not (yet) a broad market selloff.

Long Edge;

- First thing to stand out on Friday was the relative strength of the $RSP and $YM / $DIA. The selloff was led by mega-caps and semis, not the broader market.

- Very strong labour market, confirmed by strong reads last week.

Short Edge;

- Rate hike is almost certainly on the cards with inflation problems confirmed (and a strong labour market), with futures markets pricing in at least 2 this year.

- This in turn leads to a stronger dollar which weighs on Global Market Indexes...as well as being net inflationary globally.

- Mega-caps doing equity raises are alarming and adds bearish headwinds for the next 12m of the stock market.

- Spot freight has been increasing (almost under the radar) week/week.

- The ceasefire becomes ever more tenuous as strikes were exchanged this weekend.

Can/will AI be able to uphold the narrative of extreme productivity enhancement and positive economic impact?

—CW20 WEEKLY MACRO—

Why is inflation being ignored? The union of policy under Warsh and Bessent is a bet that supply-side productivity (largely from AI but supported by Bessent's 3-3-3), not rate hikes, will contain the US-Iran war driven price spike. They may be right.

Pundits have been jawboning the impending stock market crash due to inflation/oil/war/AI-like 1999!/and viruses. This does not seem likely at the moment from a price empiricists perspective.

Long Edge;

- Revenues Per Share (RPS) and Earnings Per Share (EPS) are increasing across the board at record levels. Earnings analysts are having a field day. This is not, however, reflected in the breadth of the market.

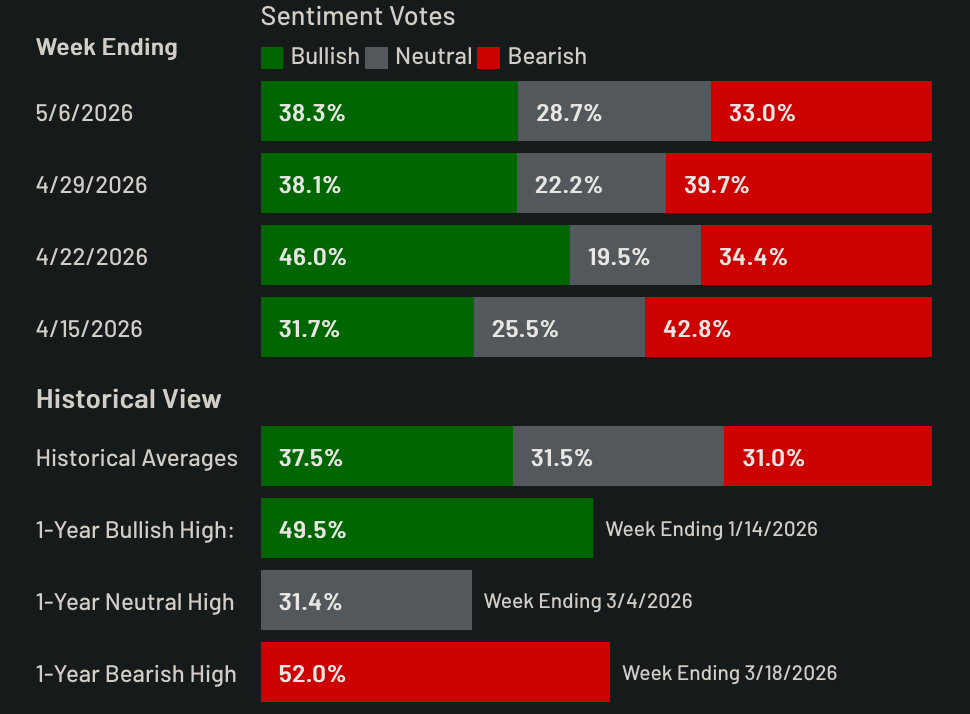

- Sentiment is still balanced (there are less bulls now than 4 weeks ago! Image ↓).

Short Edge;

- AI infrastructure (inclusive of semis) are dominating the concentration of the rally.

- Inflation is likely to be confirmed much hotter tomorrow. Will the markets care?

- Oil reserves are also dropping alarmingly. Whether or not the ensuing inflation can be contained rests on our thesis statement.

— CW23 WEEKLY MACRO EDGE —

Base Case: BULLISH. As the Iran 'Will-They-Won't-They Deal' starts to fades from focus, AI is retaking the center stage with force.

Are we approaching the singularity moment?

Consider;

- SK projected exports up 30%, with $220 historic trade surplus.

- IPOs, in the focus - like SpaceX which is primarily a bet on Elon and secondarily on AI data centers in space; where they may rapidly create a monopoly with the aid of billions in government contracts (all this despite losing $4B in Q1 2026). Reminiscent of COMSAT's "Early Bird" - the world's first commercial communications satellite which groundbreakingly handled 240 simultaneous two-way telephone calls or transmit one black-and-white television channel.

...this is all linked to AI enthusiasm.

No matter how extended you may consider the market to be, under this narrative, it may have far more to go.

Long Edge;

- VIX is low and stable.

- Growth is incredibly strong.

Short Edge;

- Liquidity is tighter than it should be, though a recovery in broad market liquidity will promptly lead the S&P500 much higher.

- Inflation is hot. Whether or not AI productivity can still markets higher is something that we can only 'wait and see.'

- Sentiment is still very poor (since COVID).

—CW22 WEEKLY MACRO EDGE—

Base Case: BULLISH with the same wild card as the last 8 weeks - Trump's peace with Iran (or lack thereof).

Long Edge;

- As economist Ed Yardeni says: it is "FEMO" instead of FOMO. FEMO stands for “Fabulous Earnings Momentum.” Valuations (more specifically P/E) is what bears loved to mention in 2025. Currently, IT trades at 24.4 forward earnings per share whilst the S&P500 trades at 21.1. That's "FEMO" at work.

- $RSP is breaking out, the S&P500 broadening in action. Whilst everyone's favourite $NVDA may be falling, it is overall healthy for a longer long run.

Short Edge;

- Liquidity of market participation measured via cross-sectional credit breadth is poor, either signalling poor sentiment driving participation or a genuine lack of net liq (we believe the former).

- Oil and petrol have been experiencing their largest historical draws on record. Repricing on fundamentals is imminent especially if peace deal and MOU with Iran is reached.

—CW 21 WEEKLY MACRO CONTEXT—

Staying humble. Mixed macro signals give no clear direction ∴ deferring to price empiricism.

Two key days this week:

1. Today, Monday. Warsh was greeted on his first day as Fed chair last Friday with spiking yields and a dropping market. Yields today will tell us more about real yields and inflation expectations.

2. Wednesday, $NVDA earnings. Likely to be spectacular, how the market reacts will be telling.

Long Edge;

- Sentiment. Both Investors Intelligence and the AAII Bulls/Bears is still below the long term average.

- Earnings and price.

- Perhaps the skewedness of AI and AI-adjacent hyperscalers dragging up the S&P500 is justified when we look at how much the large cap forward operating earnings per share are accelerating relative to the (still impressive ) MidCap and SmallCap earnings.

Short Edge;

- Federal funds futures have started to price in a rate hike. Fed officials have similarly started objecting to the prevalent easing bias signalling a shift. Wednesday's FOMC minutes will give greater clarity.

- Global yields are surging over SoH led inflation. Especially the JGB and Gilt.

- Gold is being suppressed by rising yields and a stronger dollar. This also aligns with the late inflation cycle characteristic of Gold when inflation materialises and becomes reality instead of expectation.

—CW20 WEEKLY MACRO—

Why is inflation being ignored? The union of policy under Warsh and Bessent is a bet that supply-side productivity (largely from AI but supported by Bessent's 3-3-3), not rate hikes, will contain the US-Iran war driven price spike. They may be right.

Pundits have been jawboning the impending stock market crash due to inflation/oil/war/AI-like 1999!/and viruses. This does not seem likely at the moment from a price empiricists perspective.

Long Edge;

- Revenues Per Share (RPS) and Earnings Per Share (EPS) are increasing across the board at record levels. Earnings analysts are having a field day. This is not, however, reflected in the breadth of the market.

- Sentiment is still balanced (there are less bulls now than 4 weeks ago! Image ↓).

Short Edge;

- AI infrastructure (inclusive of semis) are dominating the concentration of the rally.

- Inflation is likely to be confirmed much hotter tomorrow. Will the markets care?

- Oil reserves are also dropping alarmingly. Whether or not the ensuing inflation can be contained rests on our thesis statement.

ICYMI: Jawboning war turned HOT (briefly) late yesterday with an exchange of fire between US naval forces and Iran.

Futures have been green.

If today closes green then Bears take heed - this may be the contrarian warning before a squeeze.

Instead of the '2026 Iran War' or the 'Third Gulf War' it should be called 'The Great Jawboning War.'

"...Americans will not obtain through a failed war what they failed to gain in face-to-face negotiations, Iran has its finger on the trigger and is ready..."

متن اکسیوس لیست آرزوهای آمریکاییهاست تا یک واقعی��،

آمریکاییها چیزی که در مذاکرات رودررو بدست نیاوردهاند در یک جنگ شکست خورده به دست نخواهند آورد،

ایران دست به ماشه و آماده است، اگر تسلیم نشوند و امتیازات لازم را ندهند یا بخواهند خودشان یا سگهای پادوشان شیطنتی کنند پاسخ سخت و پشیمانکننده خواهیم داد.

The concerned authorities in the Emirate of Fujairah have confirmed that a fire broke out in the Fujairah Oil Industries Zone (FOIZ), as a result of a drone attack coming from Iran. #OOTT

—CW19 WEEKLY MACRO—

Impasse in the SoH or resumption of the war will both ultimately lead to the same conclusion: the real repricing of energy, fertiliser, and food.

There is a split narrative, with bearish populists citing a delusional market and whilst there is a REAL fundamental risk - we must remain price empiricists.

And price empiricism is saying that there is strength without mass participation.

One could think about it in terms of percentages, inspired by the late John Bender, where we might cite a 35% for a huge left side downturn, 15% for neutral range-bound movement, 15% for a broad recovery in the markets, and 35% for right side melt up. Because options are priced around a bell via the incorrect Black-Scholes model, one could also design options positions around this thesis.

Long Edge;

- Aggregate earnings growth on most of the S&P companies who have reported is ~20%! This the result of the transmission of economic effects through 2025/6 via liquidity/employment/retail spend.

- Valuations are therefore 'low,' despite markets being at ATHs.

- Sentiment is also not showing contrarian readings e.g. AAII crowded with bulls.

Short Edge;

- Rates are not likely to be cut despite Warsh's ascension to Fed chair in a month as the majority of governors seem hawkish.

- Inflation is high and likely to be higher from source input costs.

- There is a risk in the concentration of this latest rally, though a broadening is usually healthy.

On Crude / Fertiliser / Livestock / Alt. Fuels

1/ Before 28/2 - the start of the US/Israel/Iran war, oil prices were already creeping higher on geopolitical news ANTICIPATING even higher prices for events that had yet to materialise. The collapse of the Geneva talks in early Feb gave smart money the signal to pre-position. This relied on probabilistic forecasting rather than realised fundamental data (though price action via classical charting/technicals alone can be a pure guide to get involved at this stage as well). Right now, we are in the late stages of this anticipation stage for fertiliser, grains, livestock, and alternative fuels.

2/ With the beginning of the war on 28/2 and the closure of the SoH, oil prices have been rising spectacularly to price in severe uncertainty. In this stage, price swings are incredibly volatile on headlines (and Trump tweets). We are trading the volatility of the risk premium, not baseline fundamentals. This is why we are seeing a massive divergence between "paper" futures swinging wildly on ceasefire rumours, while the physical market (Dated Brent) trades at a huge premium. It matters less how much actual oil there is comparative to the perceived risk of SoH closure extensions, war escalation, and infrastructure damage. We are here for Oil right now.

3/ Eventually, all prices have to face the physical and fundamental constraints of time and usage. In the case of oil, this supply shock will breach the limits of government subsidies and reserves, forcing demand destruction as prices become unsustainable. But the ripple effect is the real play: the SoH closure hasn't just trapped oil; it’s trapped roughly 20% of the world's LNG and a third of the global seaborne fertiliser trade. Because LNG is the primary feedstock for nitrogen fertilisers, Urea is already spiking. Asian nations are already cancelling LNG shipments and reverting to alternative fuels like coal to keep the lights on. Like oil, fertiliser, grains, livestock, and alternative fuels will all be forced to find a new equilibrium when they reach this stage.

4/ The final stage is a permanent realignment of the changed supply and demand landscape. Global supply chains may permanently reorganise away from Middle Eastern chokepoints, accelerating investments into localised agriculture, alternative routing, and domestic energy production. Just like the unfundamental markets of Gold/Bitcoin and the tangible markets of semiconductors/RAM of recent years, a new baseline will be established. Market participants waiting for the SoH to just "go back to normal" will fail to adjust and be liquidated from the new normal.

Two charts:

Japan no longer just jawboning markets but have directly intervened in the Yen ($6J) at a critical level.

10-Year Breakeven Inflation ($T10YIE) — risk premium against expected inflation is parabolic. A breach of 2.5% seems historically significant.

![TitusChing's tweet photo. Biggest Disinflation

• Hungary: 4.6% → 1.8% = -2.8 pp

• Turkey: 35.1% → 32.6% = -2.5 pp

• Japan: 3.3% → 1.4% = -1.9 pp

• Poland: 4.1% → 3.1% = -1.0 pp

• Czech Republic: 2.9% → 2.1% = -0.8 pp

Biggest Inflation

• Italy: 1.7% → 3.3% = +1.6 pp

• United States: 2.7% → 4.2% = +1.5 pp [from Jan-26 (2.4% → 4.2% in 4m)]

• France: 1.0% → 2.4% = +1.4 pp

• Eurozone: 2.0% → 3.2% = +1.2 pp

• China: 0.1% → 1.2% = +1.1 pp](https://pbs.twimg.com/media/HKg5XcPawAE1_P_.jpg)