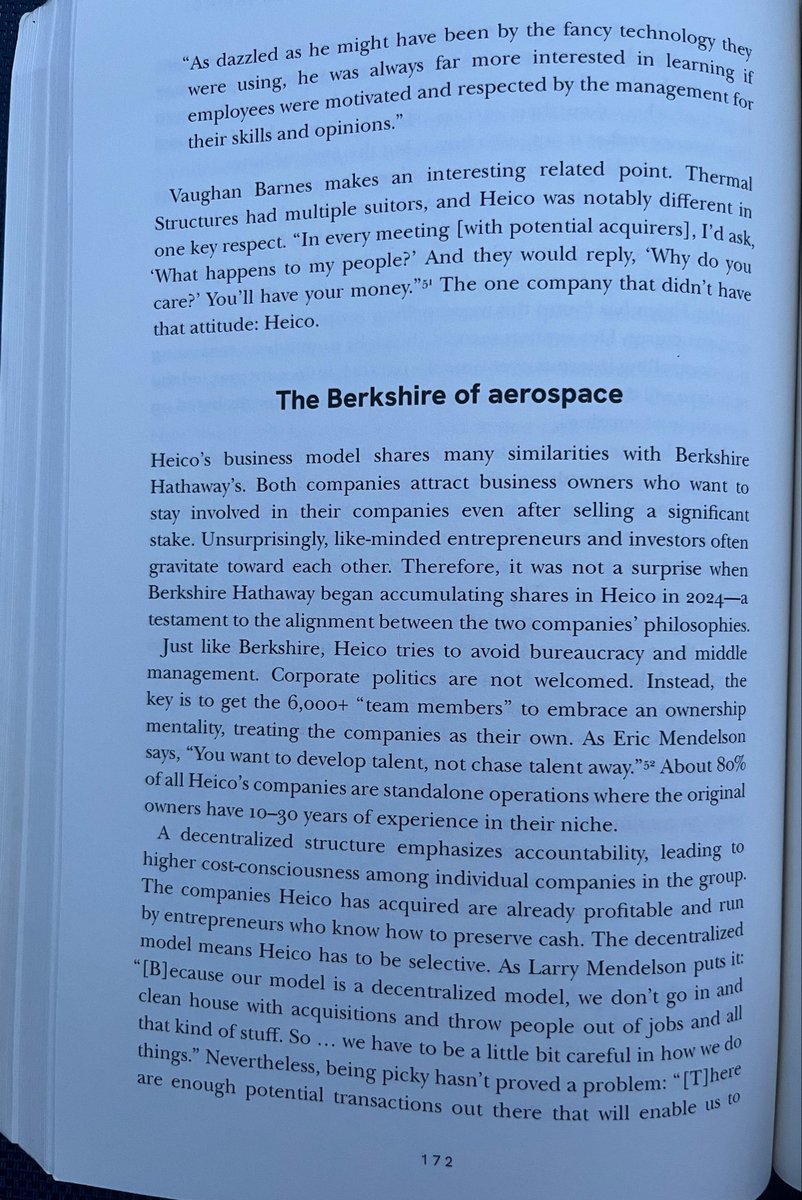

“Heico’s business model shares many similarities with Berkshire Hathaway’s. Both companies attract business owners who want to stay involved in their companies even after selling…80% of all Heico’s companies are standalone operations where owners have 10-30 years of experience”

Morningstar on $TSCO:

"We view shares as undervalued... We like the firm's plans to shift product mix into these categories, though execution will take time; thus, we don't expect an immediate bounce. The bottom line: We plan to hold our $48 per share fair value estimate.."

Morningstar on Amphenol $APH:

"We now expect nearly 50% sales growth in 2026, with 30% coming organically, and driven by the data center. Still, we like continued double-digit organic growth in industrial and defense sales that keep the business diversified."

This is probably because O’Reilly has a higher percentage of its sales mix from commercial customers, which tends to be more recurring

AutoZone also discussed this on today’s call, “It is why it is our #1 growth priority.”

O’Reilly tends to outperform AutoZone on domestic sales growth in more challenging environments (not entirely apples-to-apples because their calendars don’t line up)

$ORLY +8.1% (reported last month)

$AZO +4.1% (reported today)

Recently sold $COST at $993 or ~52x earnings

Hard for me to underwrite decent returns over the next 5-7 years at that price 🤷♂️

Also hard not to love Costco the business

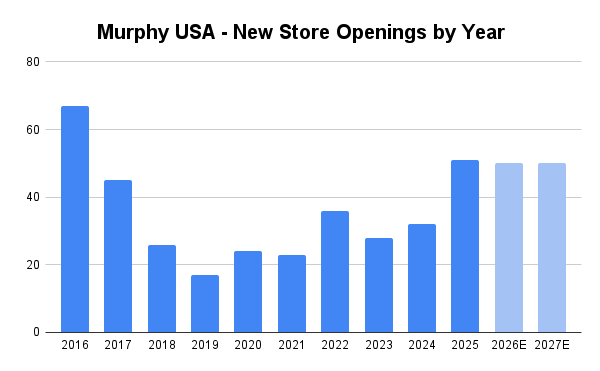

Murphy USA is expecting to open 50 new stores per year in the coming years, which should add ~$40 mill in EBITDA from each cohort as these stores mature

At $1 billion in EBITDA (2025), that should be a 3-4% CAGR tailwind to earnings from new stores alone

Link in bio!

Latest write-up: Why I Own Murphy USA $MUSA

The long-term case is more than just higher fuel prices:

- accelerated store openings

- ~15% returns on new stores and higher margins from inside sales

- attractive capital allocation, retiring 6-7% of shares annually

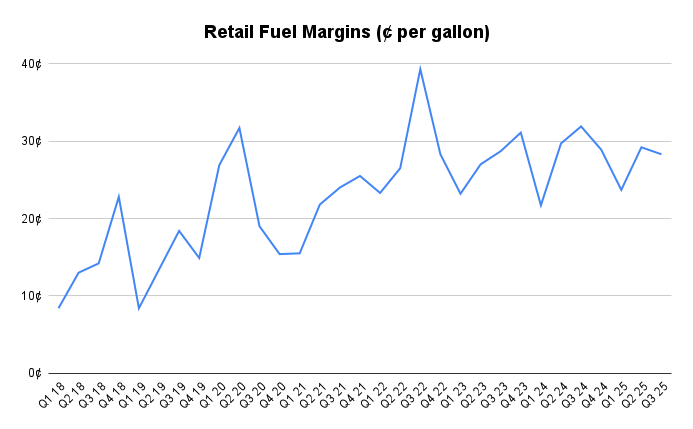

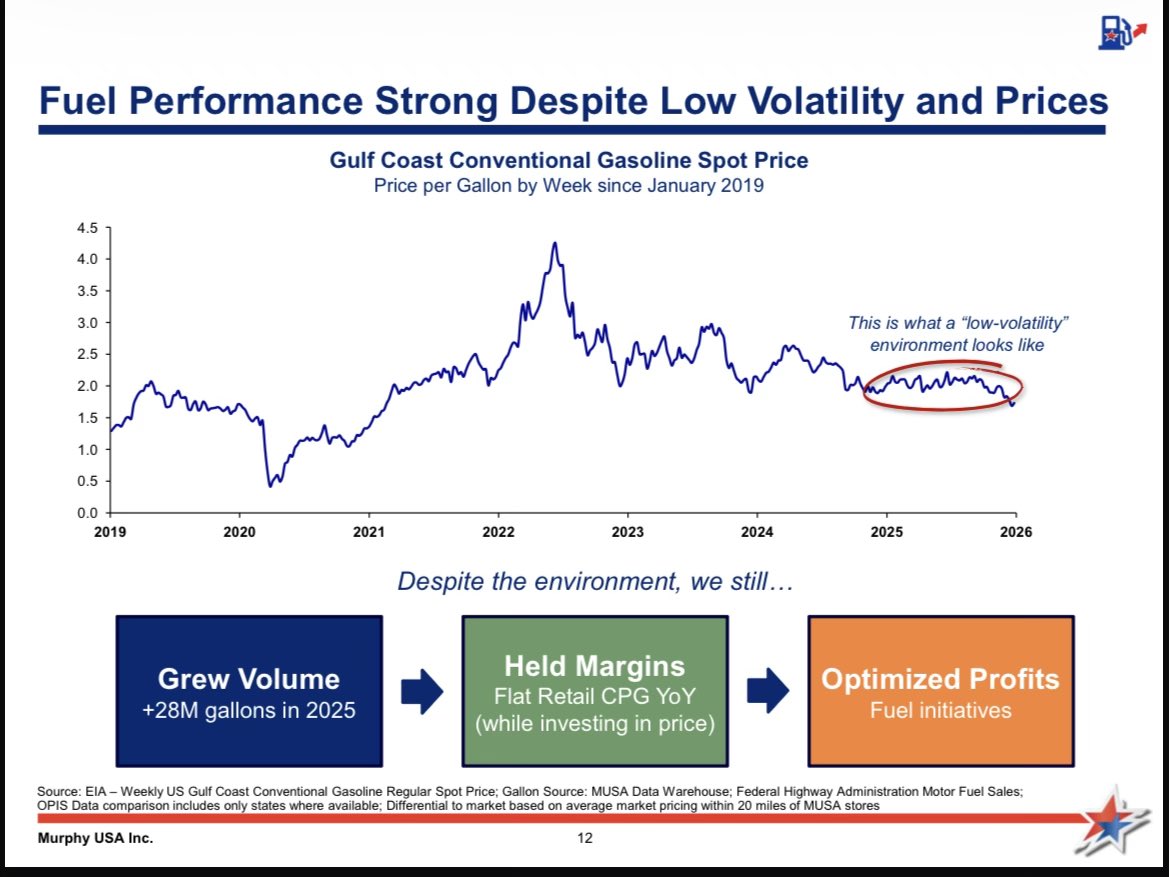

The last time we saw real volatility in fuel prices, Murphy earned ~40 cents per gallon for a brief period

Typically, higher fuel prices = more traffic for Murphy because they tend to have the lowest prices

As fuel prices increase, consumers become more price conscious

Brian Niccol: "This is the Starbucks our customers deserve and the Starbucks we believe will deliver long-term growth and value for our partners and shareholders."

Two consecutive qs of SSS growth - step in the right direction considering the prior eight were negative

$SBUX

Morningstar on $SBUX:

"We continue to view CEO Brian Niccol’s Back to Starbucks plan as a prudent strategy that reinforces the firm’s premium position and supports its long-term competitive standing by placing a greater emphasis on the customer experience"

"In an evaluation document of the model, Muse Spark tops AI models from Anthropic, Google, OpenAI, and xAI in some categories, though it falls short in others."

🤷♂️ $META

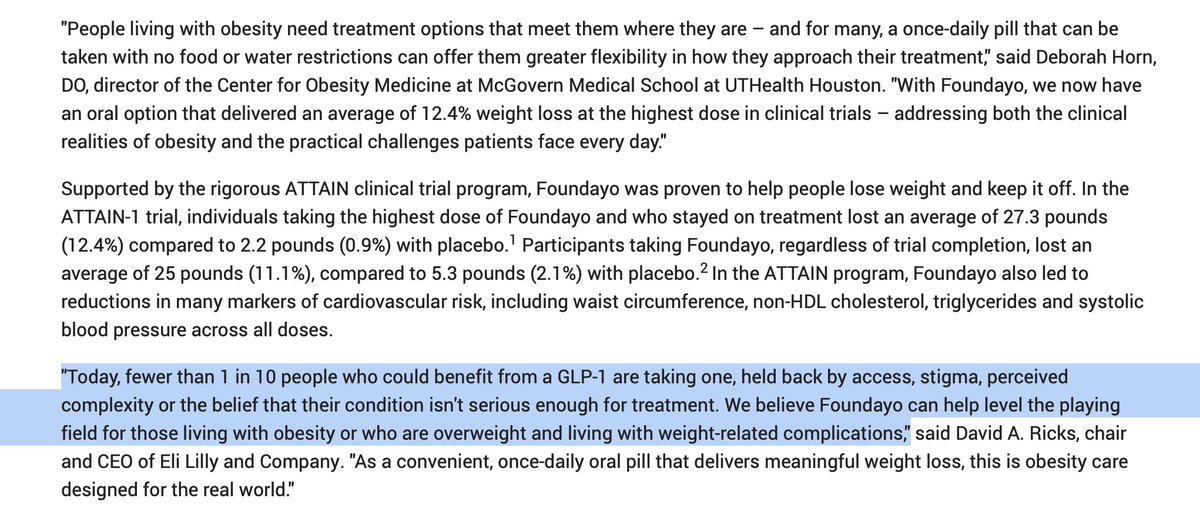

Eli Lilly: "Today, fewer than 1 in 10 people who could benefit from a GLP-1 are taking one, held back by access, stigma, perceived complexity or the belief that their condition isn't serious enough for treatment."

$LLY

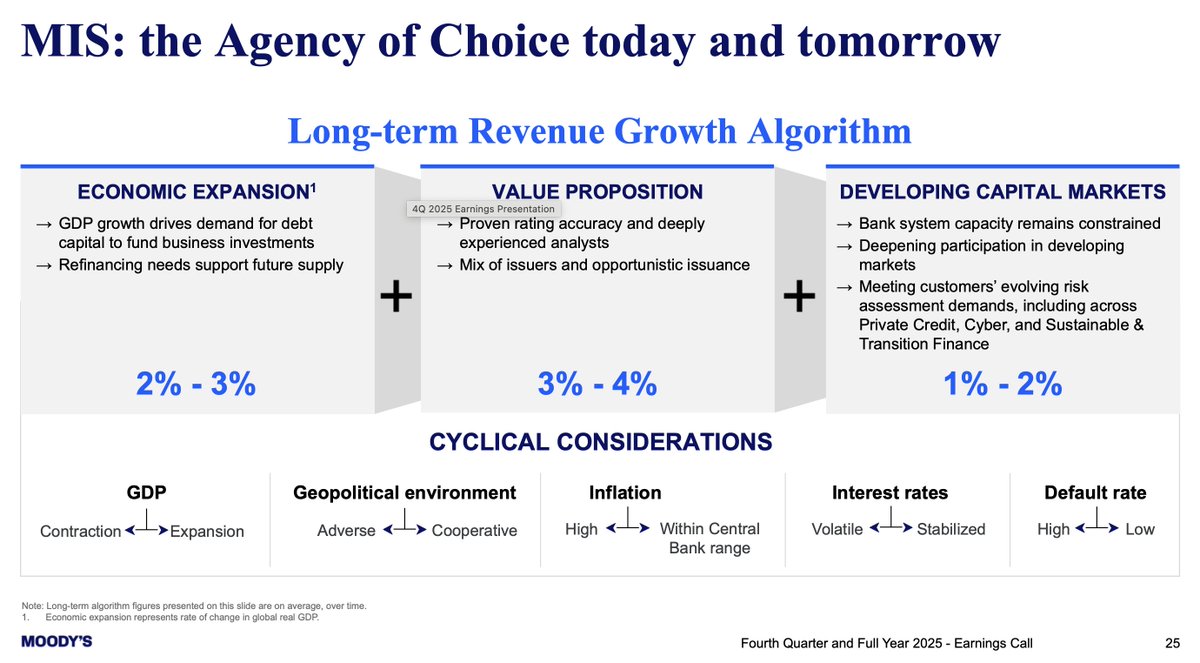

Moody's $MCO: "U.S. refinancing needs grew ~3% and remain weighted towards leveraged finance issuers... Refinancing needs up from ~$4.9T to ~$5.2T over the next four years."

$MUSA Murphy USA: “Volatility, we always say is our friend..We know that volatility can introduce itself into the market at any time, and we have a really strong and competitive business model to capitalize on it when it does.”

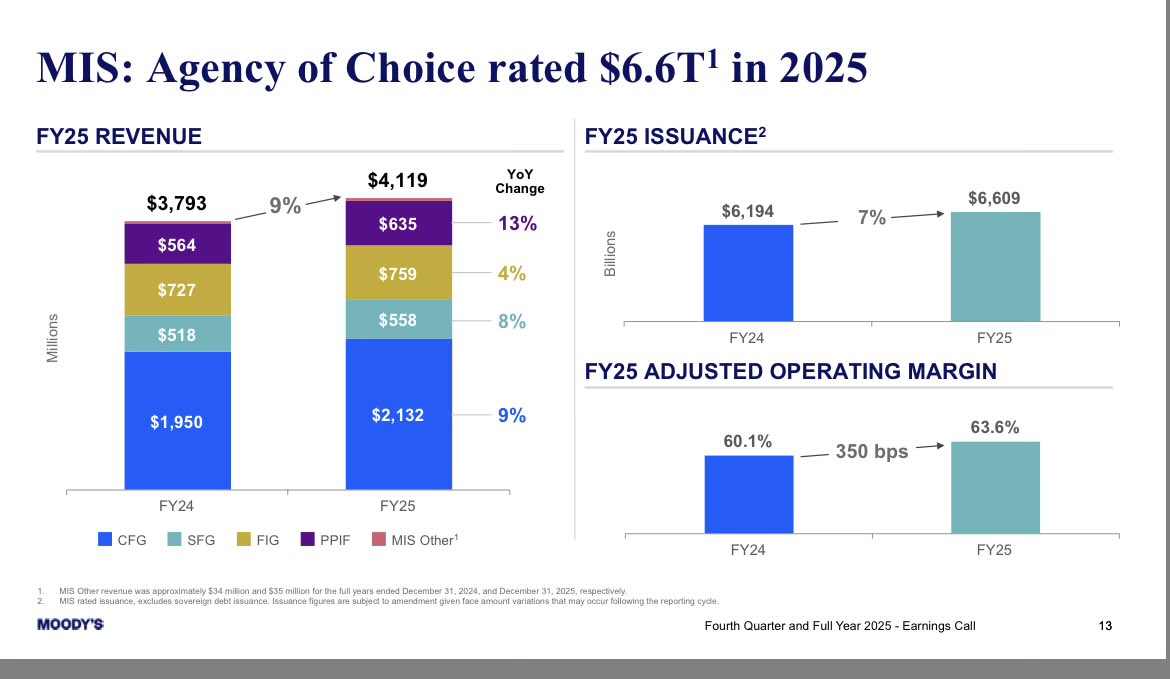

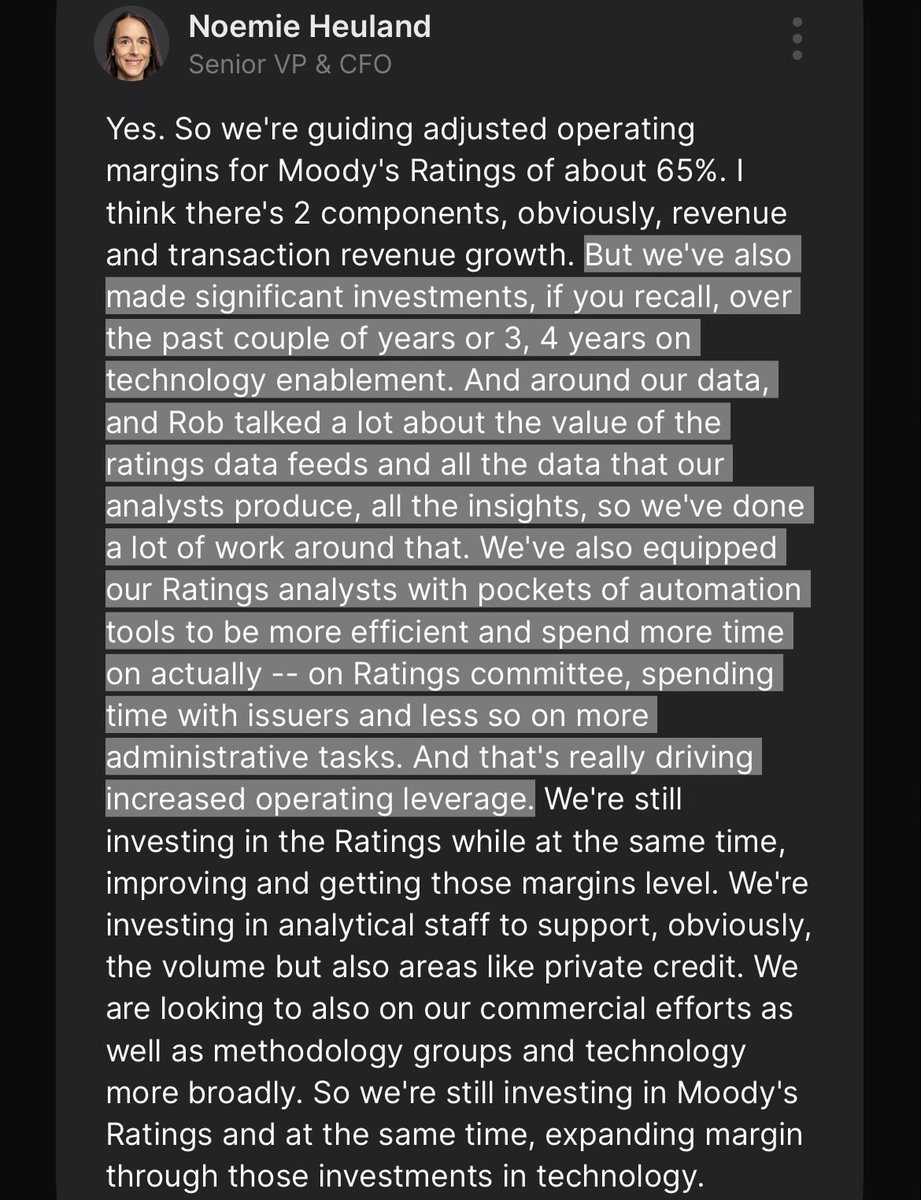

Moody’s on margin expansion in the Ratings segment:

“We've also equipped our Ratings analysts with pockets of automation tools to be more efficient and spend more time on Ratings committee, spending time with issuers and less so on more administrative tasks”

$MCO