@AnthonyCrudele 'That said, even on the short side in the Nasdaq I would stay skeptical about getting too aggressive'

Given VIX is trading 16-being aggressive on short side is v-risky. As you said, its sell rallies type market as profit taking continues.

Broadcom is not Nvidia. But not raising guidance at a time when every chip company is telling us demand is stronger than expected should be enough for a mild pullback.

Yes, Broadcom's custom chip business is different. Yes, management may simply be being responsible.

But markets do not wait around for explanations.

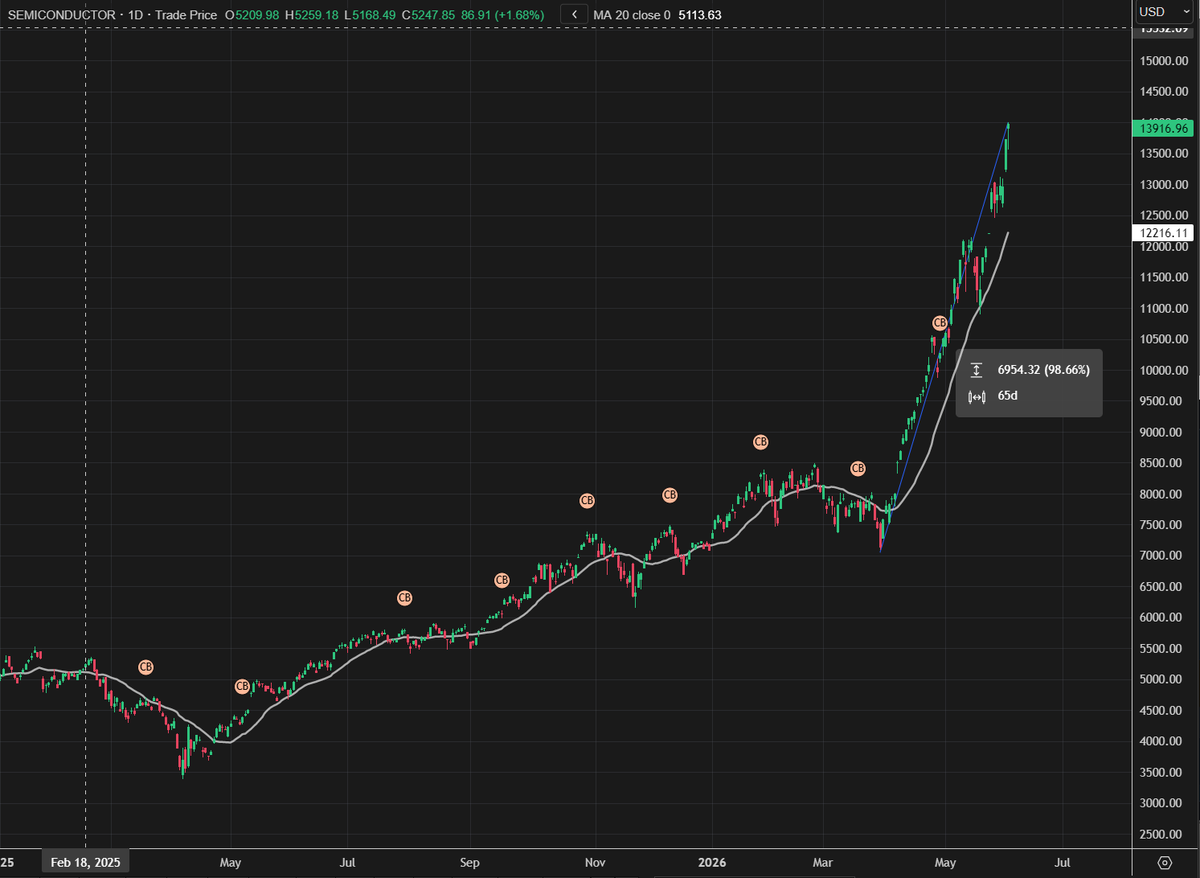

The Semiconductor Index is up almost 100% from the April Middle East war lows (chart attached). At some point, good news stops being enough.

Broadcom is down >10% overnight and that will drag rest of chip sector lower with profit taking mode.

What does that mean for broader markets? Semis have dragged US equities to record high after record high over the past few months. When leadership pauses, the index pauses. So further consolidation now looks likely.

To get equities aggressively bidding again, the market needs the next catalyst. It is oil. Get Hormuz flowing normally again and risk assets will have a reason to push higher.

Oil is heading back toward its 20-day average around $97.

The reaction in bonds and equities remains muted. That speaks volumes. Markets are already pricing a deal.

Overnight we got more of the usual headlines.

"Self defence."

"Retaliation for attacks."

"Targeted."

"Limited."

And risk assets barely reacted, bcause the market is fully priced for a 60-day ceasefire MOU and some form of agreement to reopen Hormuz. That remains the base case.

But the clock is ticking. There is plenty of debate around reserve levels and how much longer this can continue. What there is broad agreement on is that meaningful shipping traffic needs to be flowing again before the end of July.

For now, traders are willing to wait. But markets are not infinitely patient. At some point, if the headline does not cross the wires, the market will start questioning the assumption that a deal is imminent.

Until then, muted reactions tell you everything you need to know.

ECB Update. Inflation comes in above 2% target, as expected due to the conflict.

ECB is suffering from short term bias. Fearful of a repeat of 2020 covid inflation spike. CPI chart attached. Of importance here is the timing of the Russia/Ukraine conflict. Note how inflation was ALREADY at 5.5% at time of the conflict. Throw in a supply shock at a time when people are spending lavishly like there is no tomorrow and you get 10% inflation.

This time is different. The starting point for one is inflation was at the 2% target. Secondly consumers are not spending lavishly, they are being cushioned by governments subsidizing the current energy price shock.

Hiking rates next week will be a policy mistake despite it being called an insurance hike.

The result will be below 2% target inflation in 2027 and a return to low growth , low inflation era experienced pre-2020. If it were not for the lavish fiscal spending across Europe, most countries would print zero growth.

Market Squawk: Anthropic moves toward IPO, potentially beating OpenAI to public markets. Nvidia launches next-gen AI PC platform; Iran negotiations continue despite conflicting signals from Tehran and Washington.

#AI#Geopolitics#Oil#Hormuz#MoU $NVDA.NE

MSTR announces formal sales of just 32 BTC and market continues the freefall. This despite risk-markets sitting just shy of record highs.

With IPO's like SpaceX and Anthropic its going to suck even more money away from Crypto-Land.

For reference, Anthropic will raise between 50-100bn at IPO for a valuation around 1trln mark. Historically Saudi Aramco was largest raising 25.6bn.

There is some serious money about to be allocated toward new shiny, exciting , sexy themes.

All that new money has to come from somewhere. Retail chases the hype. BTC is so 2000-and-boring.

@Kuma_D_Trader Unfortunately there are officials desperate to not repeat the blunder of Covid . The difference this time around is peoples bank accounts are not piling up with cash .

ECB hiking next week would be a mistake.

What does 25bp actually achieve? Households are already being squeezed by higher fuel and food prices. Another hike simply acts as an additional tax on consumers at a time when demand is already slowing.

The Eco Suprise Index chart tells the story (attached). US economic surprises are improving despite 50/50 chance of hike priced in. Europe? Rolling over!

And look when the divergence began to accelerate... right as the Middle East conflict started feeding through energy markets. Europe is simply more exposed. Higher energy costs hit European consumers harder, hit growth harder and show up in the data faster.

The ECB is worried about inflation expectations. But hiking into a supply shock does not create more oil, lower fuel prices or reopen trade routes. It just tightens financial conditions further.

I said it before, I will say it again. I think the market will eventually price the mistake by flattening the curve massively and eventually forcing aggressive cuts from ECB.

London June 18th. 🇬🇧

I’m hosting a meetup for traders. 🤝

@traderkane and @Trader_Bran are trading the close live. In person. On the charts. No rehearsal, no replay. 📈

Spots are extremely limited. You know what to do 👇

https://t.co/5EgIIbjzmU

US strikes Iran again in ‘self defense ‘

Iran strikes in retaliation

Red lines remain and talk of imminent MOU being agreed are premature. Yields will now steadily rise as spot oil begins to price out an imminent agreement and the likelihood of more ‘intense ,self defense , limited , retaliation’ strikes increases as we head into the weekend.

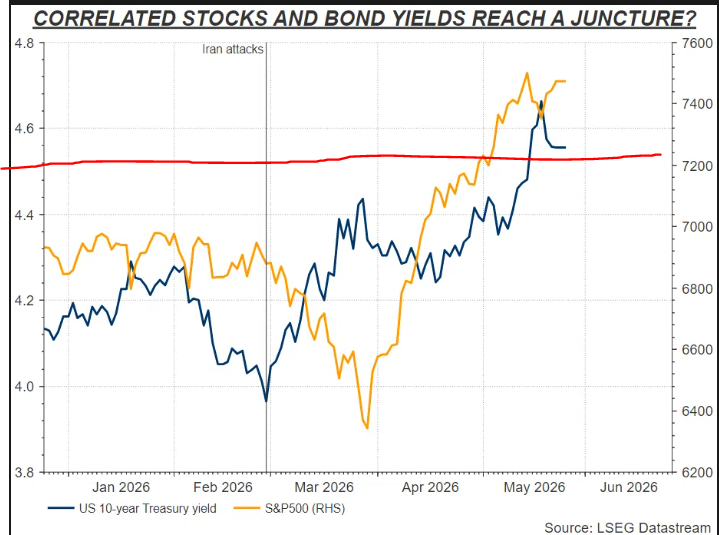

Yields in the news again this AM. Soc Gen talking about correlation between SP500 and US10yr. (Chart Attached).

In simple terms. ABOVE 4.5% is a drag on further upside returns for risk markets. Current yield 4.46%.

Two things to note.

1. If US 10yr drops back down to 4% once the war resolves. Then SP500 year end targets of 7700 which is consensus needs to be revised ALOT higher.

2. To get back to 4% you need oil below $75 . Which is unlikely in 2026.

All you need to know? If no deal in the Middle East by the end of the week, yields will again be pushing higher above 4.5% and that will again flush out the momentum chasers.

Except that calling for capitulation of bonds is pre-mature . Oil above $80 will have pass through effect on inflation and Fed won’t hike . They will simply tolerate higher inflation for longer . In that context - long bonds stay elevated for longer. Should the Fed choose to run policy with easing bias they will only create higher long end yields . Looking at the charts technically there is nothing capitulation about it right now . The logic however of betting on small caps - is sound and small caps lead the rally at start of the year when 10yr was pushing on 4%.

@ChenaeMarr2213 Throughout Europe banks are tightening lending conditions ! The rate hike effectively hit already . If the ECB is smart they can simply keep forward guidance on tightening bias until war is over . Unfortunately this bunch wants to vindicate themselves of the covid blunder !

Markets are locked in for an ECB hike in June.

I think it will prove to be a policy error.

The ECB has always been obsessed with inflation expectations and yes, policymakers are worried higher oil prices eventually feed into wage demands. That is why they want to get ahead of inflation pressures now.

Looking at 5YR Inflation Expectations. Higher oil + tighter financing conditions are already hitting demand. Inflation expectations already peaked back in early May.

Consumers are pulling back and we are seeing some demand destruction. This is the problem with hiking into a supply shock.

You risk crushing the little bit of growth that was manufactured with Covid spending bill, just as inflation expectations begin rolling over.

If the ECB hikes from here, expect the bond curve to begin flattening aggressively as the market starts pricing the policy mistake. Later this year you will see growth forecasts downgraded further.

The ECB waited 12 months too long to hike after Covid, now they rushing to hike to avoid a repeat of Covid. Covid was a supply shock without demand destruction.