I still don't think I own enough $ZETA and its ~30% of my portfolio.

Total Addressable Market: $700B+

The Global MarTech space could reach a TAM of $2.4T by 2033

Zeta continues to capture 51% of the Fortune 100 companies and partner with huge names like $PLTR, $SNOW, and OpenAI.

The long-term vision of Zeta Global has such a bright future. They just need to execute.

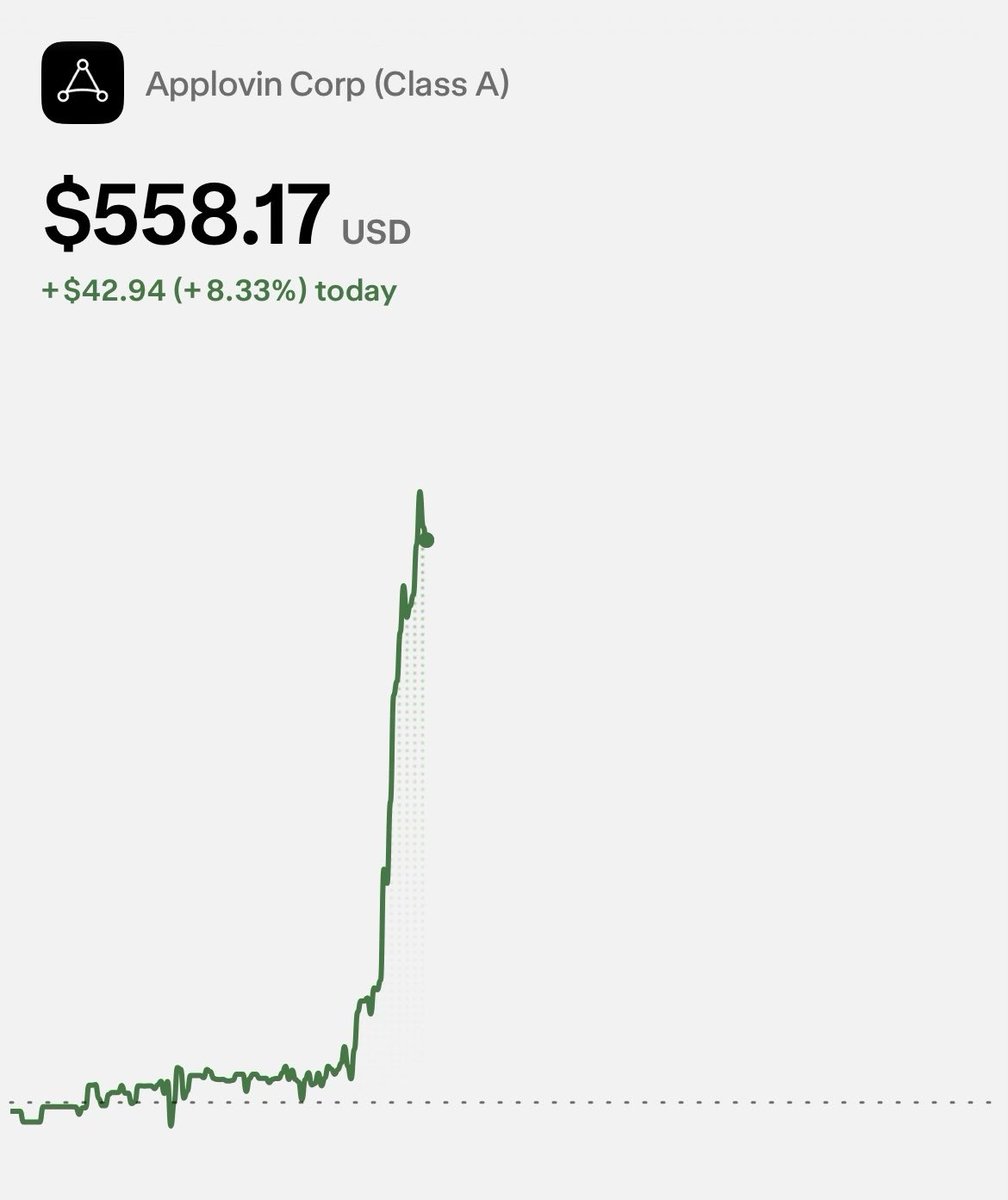

$APP is up 20% this week and I'm still looking to buy more.

• Price/Sales Multiple: 28.4x

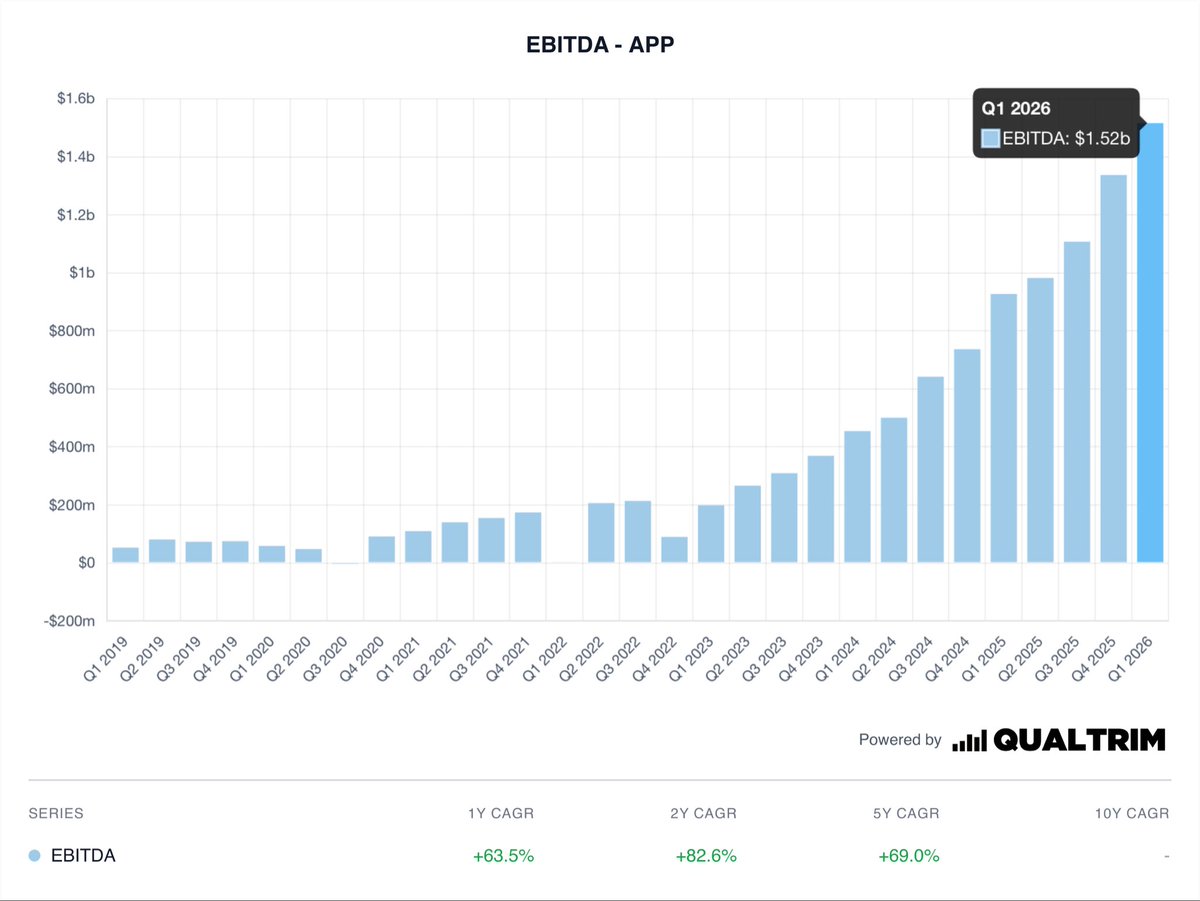

• Q1 ‘26 EBITDA: $1.52B (+82% 2Y CAGR)

When a business prints a 85% adjusted EBITDA margin while accelerating its top line growth at 59% YoY, traditional valuation multiples get forgotten about.

The market continues to price $APP like a gaming ad network, when truthfully they are an automated AI platform capturing highly scalable enterprise software spend.

Good morning $APP shareholders!

+8% this morning.

This one continues getting swept under the rug. While traditional software companies trade at massive multiples on slowing growth, the market is finally forced to re-rate this operating leverage beast as their new self-serve platform goes public.

Is the neocloud business dead…?

$META Announces plans to build out its own cloud business ("Meta Compute") to rent out its massive surplus of AI data center capacity and raw GPU compute.

Neocloud stocks like $NBIS tank -15%.

When a hyperscaler with infinite cash decides to monetize its overbuilt infrastructure and aggressively compete on raw capacity, the premium multiples for independent GPU operators vanish instantly.

People dont understand how industry breaking this move is...

$APP is taking its self-serve ad platform wide open. No referral codes, no gatekeepers. Any brand can now instantly target 1B+ daily active users.

This isn't just an ad network anymore it’s an automated software behemoth.

One of the craziest ETFs right now is $DRAM.

This ETF was listed in April '26, and it has already delivered a over 140% in less than 3 months.

DRAM is concentrated in the big three global hardware titans fueling the AI buildout: Samsung, SK Hynix, and Micron.

$MU is 27% of this ETF, earnings today will show a massive narrative.

MU's earnings are today.

Expected Numbers:

• Revenue Estimate: $35.75B

• EPS Estimate: $20.76

• Current Revenue: $23.86B (+102% 2Y CAGR)

With massive AI demand for high-bandwidth memory completely selling out their production lines, the market is expecting these historic, high-margin numbers to keep piling up.

Im bullish $MU.

$APP is officially opening the floodgates.

The self-serve ad platform is now open to ALL advertisers, no referral code needed. Any business can now tap into their 1B+ daily active users via a near one-click campaign setup.

The performance software flywheel is about to EXPLODE.

Nebius revenue guidance is STUPID.....

Consensus is estimating revenue to go from $3.5B in 2026 to $53B by 2023.

That implies a +97% CAGR over the next four years.

$NBIS

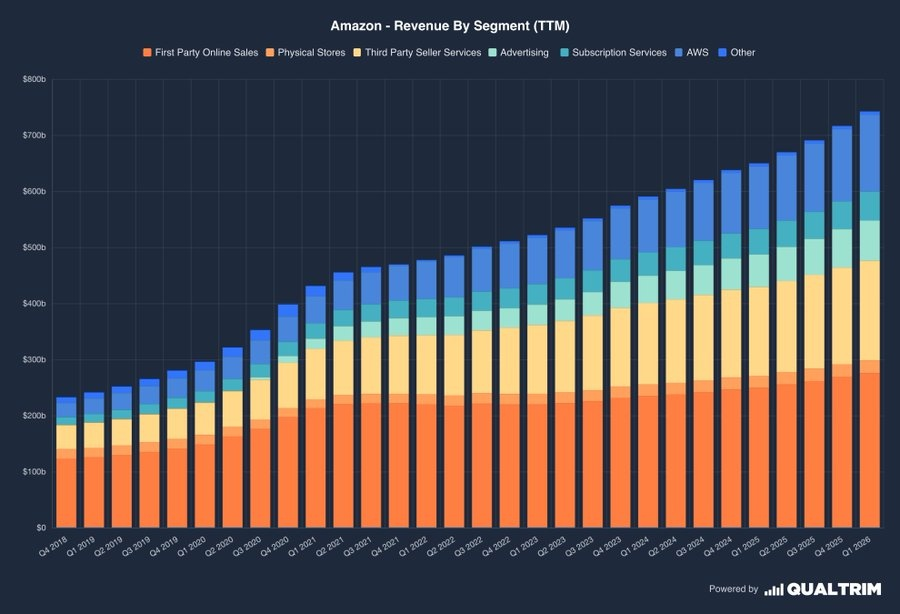

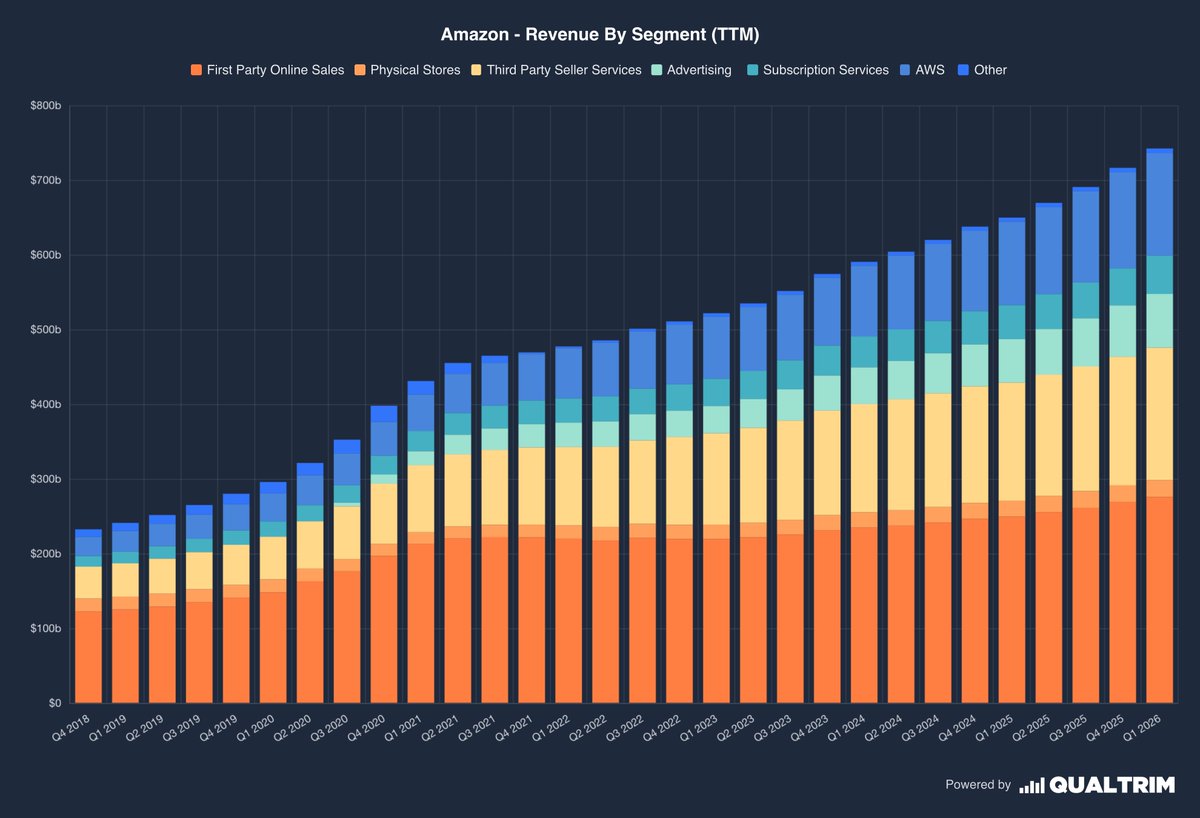

Amazon is an ETF within itself.

Ttotal TTM revenue has hit $743B

Between AWS cloud infrastructure, third-party seller services, and a digital advertising engine, you are buying a highly diversified powerhouse with 10 revenue streams.

This company is going nowhere.

$AMZN

One investment gives you exposure to:

- SaaS

- AI Chips

- Robotics

- Streaming

- Healthcare

- Robo-taxis

- Space Economy

- Cloud Computing

- Digital Advertising

- Consumer Economy

That investment is, Amazon.

$AMZN

An unheard of business "Kits Eyecare" ($KITS.TO)

Revenue: $40.6M (28% 2Y CAGR)

The demand for eye care will never deteriorate.

This Canadian startup is taking market share by offering lower cost products to the average consumer. By bypassing traditional optical markups, their direct-to-consumer digital model converts recurring volume into steady, high-margin revenue growth.