Long career in financial markets. Started as a spot FX trader, but then branched off to stocks, options & futures. Don't take anything as financial advice!!!

Caterpillar stock retreated from a record Wednesday after Michael Burry, famed for The Big Short, disclosed a short position in the industrial heavyweight https://t.co/kXe3Vm5BzR

Goldman Delta 1 head:

"The most interesting thing I read over the weekend came from Brian Armstrong at Coinbase. The accompanying chart showed AI spend has almost halved while token usage continues to grow exponentially. As Armstrong put it, “The goal isn’t to suppress usage. It’s to build the infrastructure that makes exponential growth sustainable.” The key wasn’t using less AI, but routing. Simple tasks are automatically sent to cheaper local or open-weight models, while frontier models are reserved for genuinely difficult reasoning. As he put it, “Ultimately, humans shouldn’t be choosing models. AI can automate this task.” I think this is one of the clearest examples yet of inference cost deflation. Some enterprises will build on-prem infrastructure, but many will simply route workloads to lower cost providers. The common denominator is that useful output per dollar keeps rising. Ironically, if companies discover they can achieve the same output for half the AI spend, the first instinct may not be to accelerate capex… it may be to pause and optimize."

Super Micro Computer’s offices in Taiwan were raided by government authorities on Monday, widening an investigation into the alleged smuggling of Nvidia chips into China using the company’s servers, according to a person familiar https://t.co/UepLXGZJv2

1-year rolling correlation between the S&P Equal Weight index and the S&P 500 index has collapsed to just 79% - the lowest reading ever (vs avg 96%). US equities are no longer trading as one index; they’re trading as a collection of individual stories

“South Korea has triggered five market-wide trading halts in 2026 — against only eleven such full-market halts since the system's 2000 inception. Nearly half of all market-wide halts this century have occurred this year. The rapid proliferation of highly leveraged single-stock ETFs on Samsung and SK Hynix has turned the KOSPI into a giant, self-reinforcing feedback loop.” - Goldman

For a precious metals buyer, gold vol popping and the put skew going vertical isn't a warning sign. If anything it's the best setup you'll get.

Gold vol is up around the 80th percentile, and the put skew is about as steep as I can remember. The market is paying a fat premium for downside protection in gold.

If you're nervous, that looks like a reason to stay away. If you actually want to own gold lower down, it's the opposite.

Steep put skew plus high vol means the puts you'd be selling are richly priced. So selling cash-covered puts at a level you'd happily buy gold anyway has rarely looked this attractive.

Equity index skew has climbed back to the 70th percentile. When skew is that elevated and vol then drops, dealers have to do Vanna buying, mechanically buying the index as their DELTA changes. That flow can propel the S&P back toward 7500 over the next week.

On positioning it's murkier. GEX models suggest the street is short gamma, which would normally mean more movement. But 0DTE supply tends to act as a stabiliser and offset some of that. 10-day realised is around 19.5 with front expiry options near 18 vol, so realised is running a touch above implied.

Hard to get a definitive read on street positioning here, but it doesn't feel that short vol to me. Fixed strike vol would be reacting more to down moves if it were...

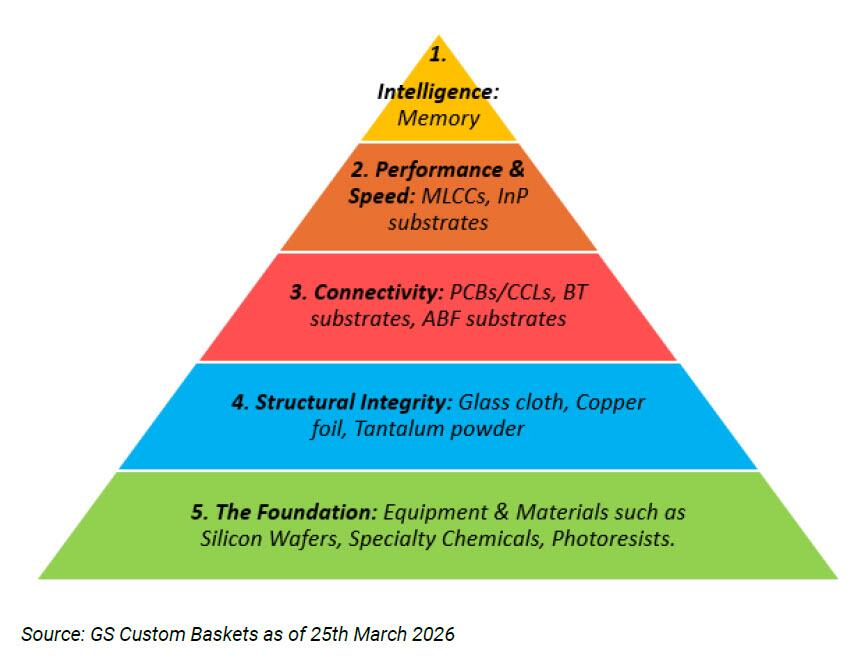

We've seen rotation between hyperscalers (payers) and chips (receivers). But all "bottleneck" companies now realize they can pull a "memory" and aggressively hike prices (capacitors are up as much as 20x in weeks). When do we see rotation out of memory into other substrates?

From Goldman's Delta-1 Desk:

Hyperscalers: This is poised to become one of the defining debates of the next few months. Markets have rarely rewarded companies allocating exceptionally large proportions of free cash flow toward capex during the build phase. This does not necessarily mean management is making poor long-term decisions; it simply means equity investors generally prefer immediate, tangible returns to distant, uncertain cash flows. Multiple expansion typically occurs during the harvesting phase, not the construction phase. The theory of reflexivity remains highly relevant in this environment. If hyperscalers continue to underperform while suppliers rally, boardrooms may increasingly question whether incremental AI investment is maximizing shareholder value. At some point, capital expenditure may slow and if one peer blinks, the market will immediately question whether others should follow.