Secured 3rd place in The Leap - Christmas Edition😇

It was a trading contest by @tradingview (8-19 Dec 2025) where 71432 traders participated globally.

A tough competition with a broad exposure to trade #fx#eurusd, #spx, commodities like #gold#silver#cocoa & US stocks!

More info👇

https://t.co/0oK35bHrXk

https://t.co/PlxGrS7Pbc

Request to organizers & @in_tradingview - INCLUDE #NIFTY/#NIFTY50 index as a trading instrument in upcoming contests to get more Indian participation & interest!

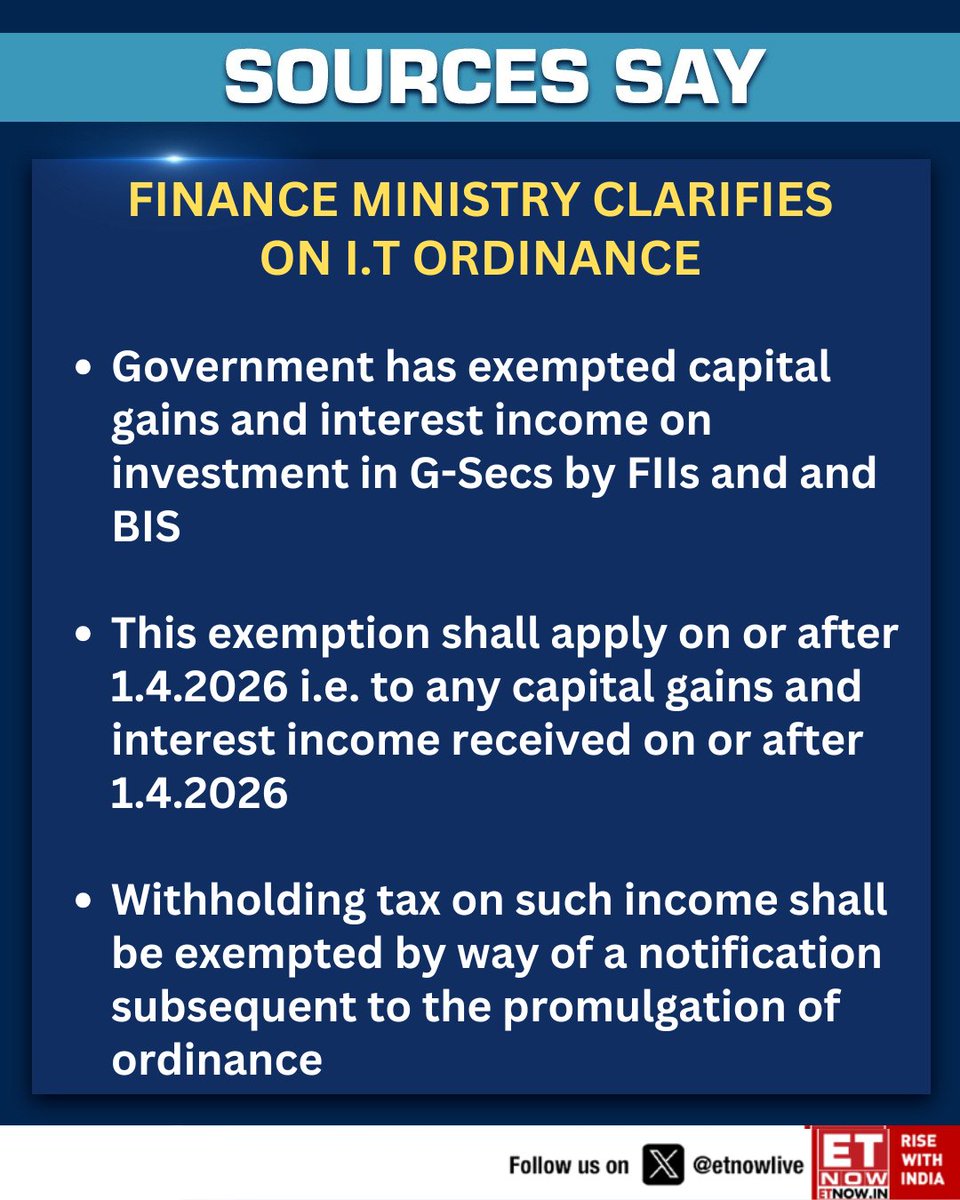

Despite issuing ordinance to exempt FII investment in G-secs from capital gains tax, IN10Y & #Rupee closed 6.97% & 94.9 resp. Why? Because bond & forex markets see much beyond this😈

1. Foreign ownership of G-sec is only 3-4% compared to domestic side. How can a favorable tax regime for this small fraction change the overall sentiment? Massive G-sec supply of Rs. 17.2 trn is also coming for FY27. Again, the marginal domestic buyer, i.e. banks, insurers, and the RBI, will have to absorb the majority.

2. Size of FPI investment depends on rupee status, not on tax. Dollar sales drain rupee liquidity, which forces more OMO to refill it, which is precisely why FY26 OMO ran to records. That feedback loop is the real constraint. Add to it not-so-good macros at the moment. RBI too has turned more cautious because of rising #crudeoil, #INR weakness, geopolitical risks, and inflation concerns! FY27 CPI inflation forecast raised to 5.1%, GDP growth cut to 6.6% from 6.9%. Market can outweigh the forces that actually set the price. Can FPIs be lured in this scenario? I DOUBT!

3. Ordinance is a slow structural positive, which will take its own time to fructify. I expect a slow uptick in FPI buying, maybe faster in Fully Accessible Route (FAR) than in General Route. This should support G-sec demand & provide some rupee support.

4. As far as the equity markets are concerned, longer-term problems & structural issues need solutions. Don't get too excited about this ordinance. Sorry, but it doesn't move the needle much! #nifty #nifty50

1. RBI bond buying is unprecedented, FY26 OMO purchases at record highs which absorbed more than 50% of GSec supply! RBI cant do this forever, sell dollar to defend #Rupee. Without this, we will be8%😈

2. CPI came at ~3.5% in Apr26 below RBI midpoint of 4%. Fuel hike after effects abhi baaki hai. So CPI should go up. Then the game begins....

3. also Repo was cut 100 bps in FY26 to 5.25%, so at 7% yield, term spread is only 175 bps, which is generally a fair value structure for EM curve. Let the front end move first, then.......🙈

4. Baaki toh tighest ever spread was in 2004, ~60-70 bps, even recently of 170 bps in mid 2025.

5. Sau baat ki ek baat is our sovereign debt is no longer attractive to unhedged foreign capital.

6. Mark this. More INR weakness coming before you see spread widening. Though RBI will let it happen in orderly fashion, IN10Y will blow out later this year

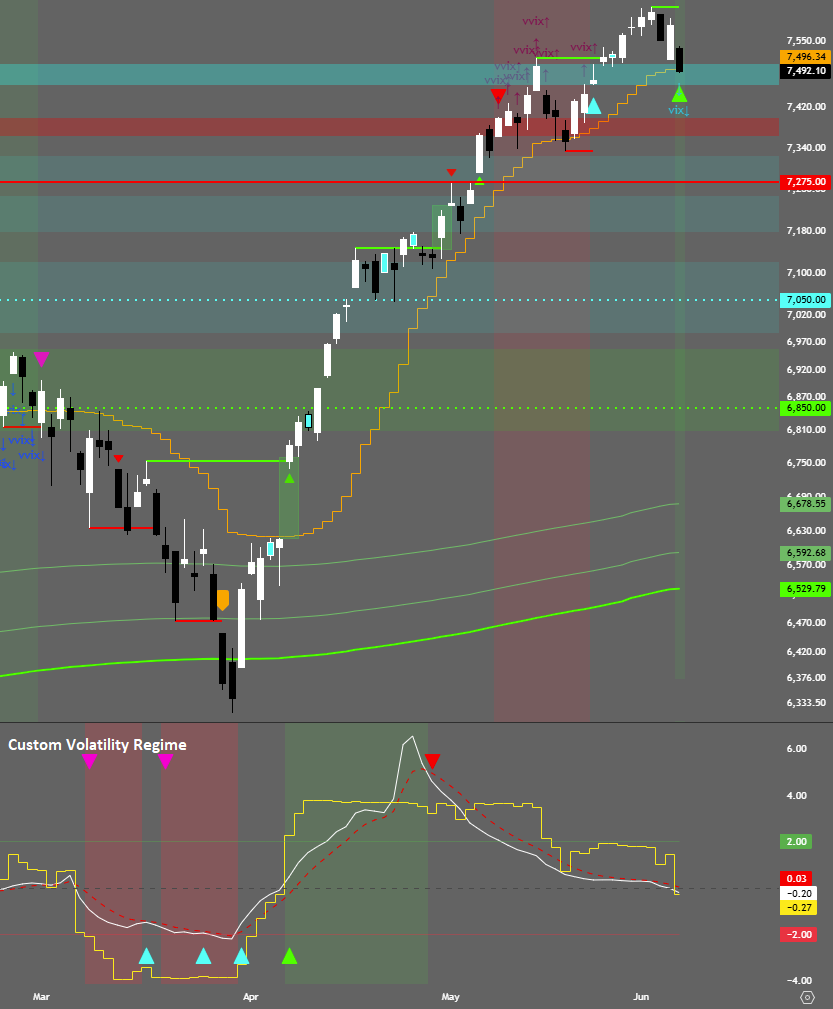

After breakout above 7500, #SPX did a slow grind till 2nd June26 to 7600-7650 (~7620 highs) with mean-reverting intraday flows and suppressed realized volatility!

Today regime has changed, aggressive selling seen since ~7532 level. As per current positioning, expect 7580 as resistance and 7460 to hold. Break below it looks like a low probability event as of now, but if it happens, 7400 should be tagged in next few sessions!

$spy #spx500 #es_f

#SPX gave a clear breakout >7500 (high of ~7539), now at 7515! Key support area around 7300-7275!

At the moment, SPX is riding a long gamma regime. So, expect a slow grind till 7600-7650 by next week, with mean-reverting intraday flows and suppressed realized volatility!

$spy #spx500 #es_f

1. RBI bond buying is unprecedented, FY26 OMO purchases at record highs which absorbed more than 50% of GSec supply! RBI cant do this forever, sell dollar to defend #Rupee. Without this, we will be8%😈

2. CPI came at ~3.5% in Apr26 below RBI midpoint of 4%. Fuel hike after effects abhi baaki hai. So CPI should go up. Then the game begins....

3. also Repo was cut 100 bps in FY26 to 5.25%, so at 7% yield, term spread is only 175 bps, which is generally a fair value structure for EM curve. Let the front end move first, then.......🙈

4. Baaki toh tighest ever spread was in 2004, ~60-70 bps, even recently of 170 bps in mid 2025.

5. Sau baat ki ek baat is our sovereign debt is no longer attractive to unhedged foreign capital.

6. Mark this. More INR weakness coming before you see spread widening. Though RBI will let it happen in orderly fashion, IN10Y will blow out later this year

1. Any specific examples where AI costs have exceeded employee costs? For many repetitive workflows, AI remains cheaper than labor & by nature, it's for narrow cognition, not for replacing organizational structure!

2. AI adoption won't come down, but rates will, which, if they don't reduce, will dent their revenue. So pricing power will decline with margins. It will be race to revenue, and weaker AI startups will collapse under their massive investment costs! 'AI bubble burst' story for next year😈

#SPX gave a clear breakout >7500 (high of ~7539), now at 7515! Key support area around 7300-7275!

At the moment, SPX is riding a long gamma regime. So, expect a slow grind till 7600-7650 by next week, with mean-reverting intraday flows and suppressed realized volatility!

$spy #spx500 #es_f

#SPX - On last closing, an EXIT alert generated on breadth + custom volatility regime's bearish conditions. Expect normalized conditions & a breakout above 7500!

Though these are not BUY/SELL signals, these alerts generally precede relevant LONG/SHORT setups! Last signal was a BEARISH alert on 8th May 2026.

$spy #spx500 #es_f

Aakash! Use your top floor, which seems to be empty. Who is stopping the defenders & goalkeepers from scoring a goal? No one! But they can't coz less opportunities & they have designated work to do, same like middle order batsmen! Football is played that way only! Clearly, you haven't played football in your life. Better concentrate on what you do to stay RELEVANT😈, which is "analysis paralysis" & creating a mountain out of molehill to get 'X' payouts! Sad to see people like you become cricket experts and talk on panels

With your stupid logic, tournaments highest run getter, highest wicket taker and man of tournament should be decided once league stage is finished even in a world cup or any similar competition? Why these players didn't push the throttle to take their team to finals, play more matches and win their purple or orange caps!! Virat Kohli or Shami got golden bat/ball after league stage or end of 2023 world cup?

Surprised to see reactions on a miraculous run of #Nifty to the moon or 30K once LTCG & STCG are lowered & STT removed😀

Tax reform can ONLY provide 'marginal relief' to the market by improving sentiments, incremental flows, and trading participation. But a sustainable FPI inflow regime requires:

1. Better & sustained earnings growth of 15-18%, private capex revival, manufacturing scaleup, banking credit growth, stable margins & attractive relative valuations.

2. Policy friendliness and stability in compliance & regulations. Ease in KYC/beneficial ownership disclosures and treaty clarity.

4. Compared to markets like Singapore, the UAE, or, historically, Mauritius, India is seen as administratively heavy, and that's why FPIs started exiting since Jan 2023 after GoI & SEBI introduced a stricter compliance framework. If that is reversed, capital will flow to the path of least resistance. Read about that👇

https://t.co/XkReeEK3hh

#sensex #nifty50

Very surprised to see a reputed brokerage house like Jefferies giving amateurish view on our SIPs that have put the #Rupee under pressure, & many so-called analysts & fund managers endorsing the same🤦

1. Mechanically its true, but causally, it is a very weak argument. Analyst has overstated the causal role of SIPs in #INR depreciation.

2. Domestic SIP is related to Rupee savings, which are invested in Indian equities from one domestic balance sheet to another. No forex transaction involved. The FX leg appears when an FPI exits. So the causal entity is FPI seller, not the SIP buyer. LIQUIDITY enables exit. It does not CAUSE exit.

3. #USDINR appreciation comes from #dollar & US yields strength, capital account dynamics, RBI reserve management, trade deficits, interest-rate differentials, and India’s structural inflation differential & not because you and me buy mutual funds. This analyst has forgotten that since Feb 2026, because of the #crudeoil shock caused by the #USIranWar, the Rupee has further depreciated by 6-7%.

4. India structurally runs higher inflation than the US, so long-term INR depreciation is expected.

COUNTER ARGUMENT TO JEFFERIES:

1. If SIPs disappear, INR will weaken more because of disorderly FPI exits, which will cause sharper & deeper stock market correction. Risk perception of India would worsen with broader capital outflows accelerating. SIPs are stabilizers, not destabilizers😇

2. If there are no domestic bids, FPIs will still sell for global reasons, asset allocation, US real-rate differential, India's relative valuation, and growth premium compression. COMMON SENSE🙃

2. FPIs started exiting since Jan 2023 because of India's COMPLIANCE HOSTILITY & REGULATORY COST ESCALATION. Read my views on that👇

https://t.co/XkReeEK3hh

https://t.co/8124HqB7c8

#nifty #nifty50

With most of the contentious & important issues negotiated & accepted between US & Iran, the deal is ALMOST done except for lesser-known & basic things like agreement on uranium stockpiles + forex reserves of Iran, war reparations, strikes on Lebanon, blockade of the Strait of Hormuz & its control + toll etc.😈

#DonaldTrump has just ended #USIranWar😉& must be wondering what rate cuts, I dont need them because #crudeOil will tank to 30s, #US10Y will crash to <2% & #SPX to the mooooooon with minimum 10000 by year end! I AM DONE🥱

Don't get fooled with to & fro negotiations between US & IRAN! #DonaldTrump has bought time till midterm elections, which is evident from his tone, like "dont rush into deal", "both sides must take their time" & in his many other communications since the ceasefire!

1. IF AT ALL, any deal finalized in next few days will be TEMPORARY! I repeat #USIranWar isnt over till its military objectives are achieved, where prime objective is to secure Iran's uranium, a condition Iran will NEVER accept!

2. Double naval blockade might get relaxations along with #crudeoil flows through the Strait of Hormuz.

3. Trump's idea is to bring inflation down with lower oil prices, push #USFED to deviate from monetary policy to cut rates sooner & verbally intervene to weaken the #dollar to help its economy! #US10Y is still >4.5%, need to bring it to <3%.

4. Meanwhile, #SPX will keep on making new highs. Already tagged 7500!

Also read about the imminent break of market equilibrium later this year👇

https://t.co/k9SBdfl786

#SPX - On last closing, an EXIT alert generated on breadth + custom volatility regime's bearish conditions. Expect normalized conditions & a breakout above 7500!

Though these are not BUY/SELL signals, these alerts generally precede relevant LONG/SHORT setups! Last signal was a BEARISH alert on 8th May 2026.

$spy #spx500 #es_f

#SPX Not a sell signal, but my custom volatility regime is saying an ALERT ahead😇

Could well cause a pullback ahead of 3-5% till 7100

$spy #spx500#es_f

Don't get fooled with to & fro negotiations between US & IRAN! #DonaldTrump has bought time till midterm elections, which is evident from his tone, like "dont rush into deal", "both sides must take their time" & in his many other communications since the ceasefire!

1. IF AT ALL, any deal finalized in next few days will be TEMPORARY! I repeat #USIranWar isnt over till its military objectives are achieved, where prime objective is to secure Iran's uranium, a condition Iran will NEVER accept!

2. Double naval blockade might get relaxations along with #crudeoil flows through the Strait of Hormuz.

3. Trump's idea is to bring inflation down with lower oil prices, push #USFED to deviate from monetary policy to cut rates sooner & verbally intervene to weaken the #dollar to help its economy! #US10Y is still >4.5%, need to bring it to <3%.

4. Meanwhile, #SPX will keep on making new highs. Already tagged 7500!

Also read about the imminent break of market equilibrium later this year👇

https://t.co/k9SBdfl786

READ THIS TILL MIDTERM ELECTIONS - TACO TACO EVERYWHERE & EVERYTIME😈

1. #DonaldTrump extending #ceasefire as if by giving time to Iran, it will surrender to the terms & conditions of the US.

2. All negotiations will FAIL because the non-negotiable condition of the US = Iran's ultimate goal and vision, i.e., uranium enrichment & then "you know......what to be made out of it🧐#USIranWar isn't over till military objectives set by the US are achieved. 3. Southern Lebanon will remain in hot pursuit by Israel because, in its grander scheme of things (world is ignoring this!!!!!!), capturing part of Lebanon forever is critical.

4. Expect scuffles here & there because there is a double naval blockade in the Strait of Hormuz. #Crudeoil will remain on tenterhooks, but probably in a broader range of 80-100 with temporary spikes!

5. Amidst calming the US bond markets (4.5% on #US10Y as a line in the sand, now 4.3%), driving the rate-cut agenda, Trump will also strategize to deploy ground troops because, without that, military objectives won't be achieved.

6. #SPX to make further new highs till 7500

#13F filings are the most useless data, it's for headline aggregators, which serve no purpose but get HUGE attention when released! A 13F filed on May 15 reflects positions as of March 31, which are at least 45 to max 135 days old. By the time traders react/act/replicate what their favorite investors have done, they may have already sold.

1. 13F reports options positions using the notional value of the underlying, number of contracts × 100 shares × underlying stock price with no adjustment for delta, strike, or premium paid (SEC Form 13F instructions, "Special Instruction 10" for derivatives). So, a 13F cannot distinguish between a leveraged directional short & a cheap tail hedge!

2. The most sought-after 13F of Leopold Aschenbrenner from Situational Awareness, which again gives a wrong picture. It seems he is betting against #AI hardware boom. How will you know if he he didnt cut/exit his positions in last 45 days, as markets went against him? You can't!

3. New PUTS on $SMH $NVDA $ORCL $AVGO $AMD may already have been exited, whoi knows?!

USE it as a confirming thesis for your already created long names and become happy that you think alike😈

Leopold released his 13F and uhh... WHAT IS THIS?

Puts in $SMH $NVDA $ORCL $AVGO $AMD $MU $TSM $ASML

Bro turned into Michael Burry

However, the fact that he was in these positions on March 31st means that the following rally over the next six weeks absolutely obliterated him.

What is happening to Leopold (or what does he think is happening to us)?

Article with too narrow an approach with lots of assumptions. I have highlighted a few. Care to reply?

1. Since you have the global data, tell me which bull market (BM) after 2008 has passed your "time shift return dispersion" test? Answer is NONE! So why penalize Indian bull market of 2020-24 for the speed of policy response, which was similar globally? Do you want a slow, grinding BM1 (2003-07) or a strong trending BM2 (2020-24)?

2. None of these bull markets will pass your dispersion test - i.e., won't after 2009, China 2005–07, Japan 2012–15, India 2014–17 small caps, AI-led US rally 2023–26. So, narrow leadership, timing sensitivity & your dispersion test can't automatically invalidate a bull market! This is narrow thinking!

3. The global market is much more coupled than it was till 2008. So even the next bull market (anywhere) wont pass your dispersion test!

4. You are ignoring & diluting structural changes that happened post 2020, which improved corporate balance sheets drastically, banking system repaired (PSU banks recapitalized, NPAs sharply down), manufacturing capex revived (PLI, china+1), defence localization etc. Can you increase/improve earnings power without these kinds of changes? No! So BM2 was durable!

5. FY22 change in EPS reporting for #Nifty50 from standalone to consolidated was NOT "accounting chimera." It was proper & just - better late than never! Standalone understates economic earnings, and consolidated gives a real picture! If this bumped up EPS growth, so be it! Are you saying we should have continued with wrong accounting?

6. Your breadth-degradation claim (50% to 36% large cap CAGR contribution) is because of change in index constituents (stocks/sectors) from BM1 (financials, commodities, infra heavy) to BM2 (IT, financials, autos, capex revival). Different leadership sectors have different CAGR profiles. Blame NSE for index construction for this (#nifty & other indices are re-balanced twice a year!)

7. Your conclusion "future returns may be too pessimistic" may be right based on your investment style, i.e., at index level or passive beta, but not wrt proper active investing, i.e., top-down sector+bottom-up stock selection approach! One can still generate MAASSIVE alpha in any market regime!

You are right on one thing LTCG/STCG/STT is noise! So why are FIIs exiting? Not because of tax regime, no AI play or valuations. They started exiting post-Jan 2023 because of COMPLIANCE HOSTILITY! Read my views👇

https://t.co/XkReeEK3hh

Reproducing my earlier views differently with an easy headline😀Got feedback that earlier headline was confusing & linked it with Akash Prakash's article. Actually, my views were contrary to what he was relating to, i.e., VALUATIONS🙃

1. Don't blame valuations. Blame the compliance wall. FPI selling isn't a valuation story. It's a regulatory cost-of-doing-business story. Capital flows to the path of least resistance, and India stopped being that path in 2023.

2. Remembered in Jan 2023, Hindenburg alleged FPIs were exploiting UBO materiality thresholds & in Feb 2023 SEBI directed DDPs to require FPIs to resubmit UBO details.

3. In Mar 2023, GoI amended PMLA rules by lowering UBO identification threshold from 25% for companies and 15% for trusts to a uniform 10% for both.

4. In Aug 2023, SEBI issued a circular requiring FPIs meeting specified criteria to provide granular details of all entities holding any ownership, economic interest, or exercising control, on a full look-through basis, up to the level of all natural persons. No structural shielding.

5. In Nov 2023, enhanced disclosure norms forced FPIs to bring down their equity AUM by Jan 2024. Non-compliance means invalid registration & mandatory liquidation of holdings within 6 months from de-registration. So disclose every natural person OR sell/leave!!!!!

6. In Dec 2024, more disclosure requirements came. FPIs can no longer issue ODIs with derivatives as underlying & outstanding ODIs with derivatives as underlying must be redeemed within 1 year. FPIs cannot hedge ODIs with derivative positions on Indian exchanges. ODIs must be fully hedged one-to-one with the same underlying securities. This closed whatever anonymity channel was remaining.

7. Partial rollback came very late in Mar 2025. Till then, many FPIs exited or restructured/reduced AUMs! Damage was done in the two-year window between August 2023 and March 2025.

8. These compliances were/are a disadvantage vs. peers in Taiwan, South Korea, Japan, Hong Kong etc. Money will flow to the path of least resistance!

#nifty #nifty50 #sensex

"Missing the forest for the trees" in Akash Prakash's article on #FPI selling? Missing COMPLIANCE HOSTILITY & REGULATORY COST ESCALATION STORY for valuations & taxation narrative?😈

1. Remembered in Jan 2023, Hindenburg alleged FPIs were exploiting UBO materiality thresholds & in Feb 2023 SEBI directed DDPs to require FPIs to resubmit UBO details.

2. In Mar 2023, GoI amended PMLA rules by lowering UBO identification threshold from 25% for companies and 15% for trusts to a uniform 10% for both.

3. In Aug 2023, SEBI issued a circular requiring FPIs meeting specified criteria to provide granular details of all entities holding any ownership, economic interest, or exercising control, on a full look-through basis, up to the level of all natural persons.

4. In Nov 2023, enhanced disclosure norms forced FPIs to bring down their equity AUM by Jan 2024. Non-compliance means invalid registration & mandatory liquidation of holdings within 6 months from de-registration. So disclose every natural person OR sell/leave!!!!!

5. In Dec 2024, more disclosure requirements came. FPIs can no longer issue ODIs with derivatives as underlying & outstanding ODIs with derivatives as underlying must be redeemed within 1 year. FPIs cannot hedge ODIs with derivative positions on Indian exchanges. ODIs must be fully hedged one-to-one with the same underlying securities. This closed whatever anonymity channel was remaining.

6. Partial rollback came very late in Mar 2025. Till then, many FPIs exited or restructured/reduced AUMs!

7. These compliances were/are a disadvantage vs. peers in Taiwan, South Korea, Japan, Hong Kong etc. Money will flow to the path of least resistance!

@_prashantnair@Iamsamirarora@thesanjaydutt@bsindia

#nifty #nifty50

Hey @1shankarsharma, good article, but too narrow an approach with lots of assumptions. I have highlighted a few. Care to reply?

1. Since you have the global data, tell me which bull market (BM) after 2008 has passed your "time shift return dispersion" test? Answer is NONE! So why penalize Indian bull market of 2020-24 for the speed of policy response, which was similar globally? Do you want a slow, grinding BM1 (2003-07) or a strong trending BM2 (2020-24)?

2. None of these bull markets will pass your dispersion test - i.e., won't after 2009, China 2005–07, Japan 2012–15, India 2014–17 small caps, AI-led US rally 2023–26. So, narrow leadership, timing sensitivity & your dispersion test can't automatically invalidate a bull market! This is narrow thinking!

3. The global market is much more coupled than it was till 2008. So even the next bull market (anywhere) wont pass your dispersion test!

4. You are ignoring & diluting structural changes that happened post 2020, which improved corporate balance sheets drastically, banking system repaired (PSU banks recapitalized, NPAs sharply down), manufacturing capex revived (PLI, china+1), defence localization etc. Can you increase/improve earnings power without these kinds of changes? No! So BM2 was durable!

5. FY22 change in EPS reporting for #Nifty50 from standalone to consolidated was NOT "accounting chimera." It was proper & just - better late than never! Standalone understates economic earnings, and consolidated gives a real picture! If this bumped up EPS growth, so be it! Are you saying we should have continued with wrong accounting?

6. Your breadth-degradation claim (50% to 36% large cap CAGR contribution) is because of change in index constituents (stocks/sectors) from BM1 (financials, commodities, infra heavy) to BM2 (IT, financials, autos, capex revival). Different leadership sectors have different CAGR profiles. Blame NSE for index construction for this (#nifty & other indices are re-balanced twice a year!)

7. Your conclusion "future returns may be too pessimistic" may be right based on your investment style, i.e., at index level or passive beta, but not wrt proper active investing, i.e., top-down sector+bottom-up stock selection approach! One can still generate MAASSIVE alpha in any market regime!

You are right on one thing LTCG/STCG/STT is noise! So why are FIIs exiting? Not because of tax regime, no AI play or valuations. They started exiting post-Jan 2023 because of COMPLIANCE HOSTILITY! Read 👇

https://t.co/nXAW8QnF2r

"Missing the forest for the trees" in Akash Prakash's article on #FPI selling? Missing COMPLIANCE HOSTILITY & REGULATORY COST ESCALATION STORY for valuations & taxation narrative?😈

1. Remembered in Jan 2023, Hindenburg alleged FPIs were exploiting UBO materiality thresholds & in Feb 2023 SEBI directed DDPs to require FPIs to resubmit UBO details.

2. In Mar 2023, GoI amended PMLA rules by lowering UBO identification threshold from 25% for companies and 15% for trusts to a uniform 10% for both.

3. In Aug 2023, SEBI issued a circular requiring FPIs meeting specified criteria to provide granular details of all entities holding any ownership, economic interest, or exercising control, on a full look-through basis, up to the level of all natural persons.

4. In Nov 2023, enhanced disclosure norms forced FPIs to bring down their equity AUM by Jan 2024. Non-compliance means invalid registration & mandatory liquidation of holdings within 6 months from de-registration. So disclose every natural person OR sell/leave!!!!!

5. In Dec 2024, more disclosure requirements came. FPIs can no longer issue ODIs with derivatives as underlying & outstanding ODIs with derivatives as underlying must be redeemed within 1 year. FPIs cannot hedge ODIs with derivative positions on Indian exchanges. ODIs must be fully hedged one-to-one with the same underlying securities. This closed whatever anonymity channel was remaining.

6. Partial rollback came very late in Mar 2025. Till then, many FPIs exited or restructured/reduced AUMs!

7. These compliances were/are a disadvantage vs. peers in Taiwan, South Korea, Japan, Hong Kong etc. Money will flow to the path of least resistance!

@_prashantnair@Iamsamirarora@thesanjaydutt@bsindia

#nifty #nifty50

@a_blue_jay As a trader, work on probabilities. analyze positional data & execute basis orderflow. 'Soon' is relative. Difficult to say for #nifty 24600 in this expiry! But your 26400 can come this year!

#SPX Not a sell signal, but my custom volatility regime is saying an ALERT ahead😇

Could well cause a pullback ahead of 3-5% till 7100

$spy #spx500#es_f

@a_blue_jay 👍could very well be around 7k in #spx. That earlier chart showed the breadth divergence on 8th, followed by an asymmetric volatility regime (will post chart later). Overall, that was an ALERT system! Now comes the trade setup part for execution. Expect bearish moves ahead!