Our founder, @Adam_Parker_Tri joined @CourtneyDoming of Payne Capital and Brian Levitt of Invesco on @CNBCClosingBell to discuss the day's market action.

The key issue: market broadening beneath the surface — and why that may be one of the more important signals investors are seeing right now.

Watch the full segment here: https://t.co/xtDCQfRQFe

Interested in our research? → email [email protected]

Our Founder, @Adam_Parker_Tri joined CNBC's Squawk on the Street to discuss the latest market trends, why today's Apple price action was interesting, and what investors should be watching beneath the surface.

Watch the full interview here: https://t.co/U1uWdWif0J

Interested in our research? → email [email protected]

Ask a growth investor where we are in the AI cycle and you will hear "3rd inning." Ask a value investor and it sounds more like the 12th.

That gap is the market's tension. Staying exposed is one problem — hedging the portfolio without abandoning the theme is another.

One sector has 66% expected 2026 EPS growth and has the most negative relationship with Technology its had in 25 years.

Interested in the full insight? → email [email protected]

Our founder, @Adam_Parker_Tri, joined CIBC’s Chris Harvey and Strategas’ @verrone_chris on CNBC’s Closing Bell Overtime to discuss the day’s market action as mega-cap tech came under pressure.

The key question: is this still a momentum market, or is leadership starting to shift beneath the surface?

Watch the full segment here: https://t.co/VHrYQAItk1

Interested in our research? → email [email protected]

Everyone is talking about AI. That makes sense: the theme is real, the winners have been powerful, and the market’s attention has followed the earnings.

But portfolio construction gets harder when one theme dominates the conversation.

I joined @JonErlichman Erlichman on Ticker Take to discuss a different question: where can investors find interesting opportunities that are not dependent on the AI trade?

We talked through a group of non-AI stocks that screen well on our work, why diversification matters when market leadership narrows, and how we are thinking about opportunities outside the most crowded part of the market.

I enjoyed the conversation and appreciate Jon having me on.

Watch here: https://t.co/0SfVzDCBPR

Our founder, @Adam_Parker_Tri, joined Invesco’s @BrianLevitt on @CNBCClosingBell last week where he argued that there could be a long runway in strong AI fundamentals.

Watch the full segment here: https://t.co/icnwk6mYiy

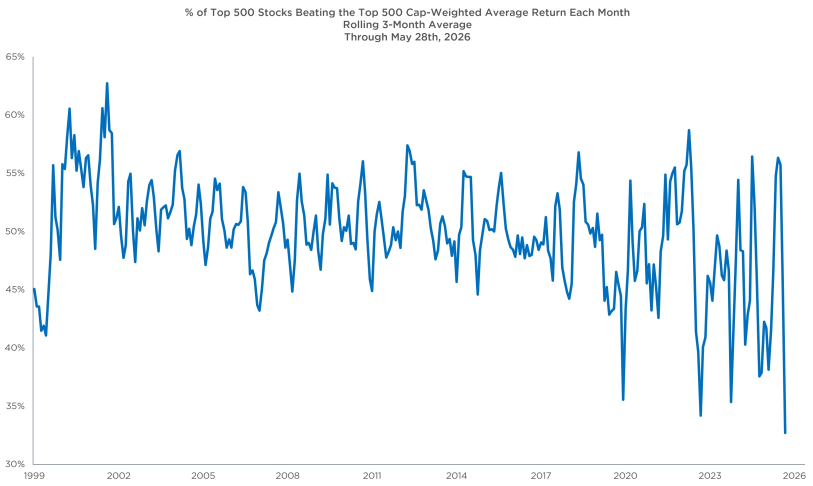

The S&P 500 rose 5.15% in May. The Nasdaq rose 8.36%.

But under the surface, only 43% of S&P 500 stocks were up — and just 25.4% beat the index.

That is not broad participation. It is a market where the winners are doing an unusual amount of work, while a surprisingly large group is still being left behind.

We looked back to 1999 to measure how extreme this split has become.

Interested in the full insight? → email [email protected]

I wrote in the Financial Times about five themes that I think US equity investors need to take seriously.

The market has changed in ways that feel less cyclical and more structural: giga-cap concentration, the surprising strength of lower-quality stocks, the return of earnings revisions as a useful signal, the market’s renewed appreciation for buybacks, and the increasing importance of dividend growth.

None of these themes are especially hard to observe in isolation. The harder question is what they mean together for portfolio construction.

If you are benchmarked to the S&P 500, concentration is no longer an abstract risk discussion. If you are trying to find alpha outside the index, the old quality/value/income heuristics may need to be re-tested against a market that is rewarding different behaviors than it did before Covid.

Full piece here: https://t.co/2m7kqnGFxP

"We can definitely all be wrong but there is no chance we are all right."

On our latest episode, we sit down with Trivariate Research Founder Adam Parker

We discuss:

☑️Why the stock market leads the economy

☑️The limits of economist forecasts

☑️What today’s rally may be telling us

☑️Why AI revenue is still concentrated in a small group of companies

☑️How trillion-dollar IPOs could affect market structure

☑️Why healthcare may be the contrarian AI opportunity

“Buy low, sell high means buy where the estimates are too low and sell where the estimates are too high, not the price-to-earnings.”

On the latest @excessreturnpod, we sit down with @Adam_Parker_Tri

https://t.co/jkVE3bgMXV

We discuss:

☑️Why valuation may not work as a stock-picking signal

☑️What today’s market is really pricing

☑️Why semis still look better than software

☑️The importance of gross margin change as a factor

☑️Why healthcare could be an overlooked AI winner

Everyone wants to map this market onto the late-1990s tech bubble.

The better question may be whether that analogy is hiding the more important signal.

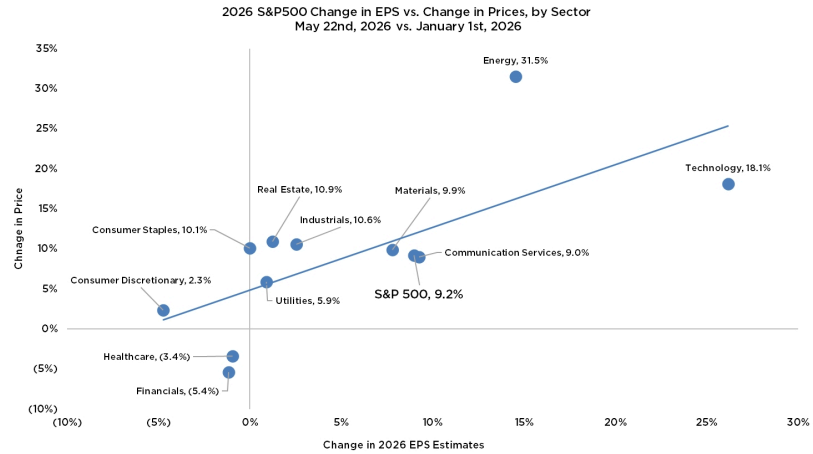

At the index level, 2026 S&P 500 EPS estimates are up ~8% YTD, almost matching the index's ~9% gain. Inside the market, sector leadership is following estimate revisions too — not just sentiment.

The market may look speculative from a distance, but the underlying earnings are less convenient for the bubble narrative.

We break down what that means for where the risk, and opportunity, may be hiding next.

Interested in the full insight? → email [email protected]

Reuters cited Trivariate Research in a piece today on how the AI trade is broadening beyond megacap technology and into small-cap tech.

The S&P 600 small-cap technology index has gained almost 54% this year, compared with a 20.1% rise in the S&P 500 technology index — the widest gap between the two in over 30 years.

The key question is not just whether smaller companies have AI exposure. It is whether investors are correctly separating durable earnings beneficiaries from stocks being pulled higher by the broader search for second- and third-order AI winners.

As I was quoted in the article, investors are looking for companies that can benefit from AI through share-gaining solutions or productivity, driving optimism about earnings growth.

Read the full Reuters article here: https://t.co/YbC7Q0GE2c

If you're interested in our latest views on AI exposure, portfolio risk, and the equity market as a whole, please reach out at [email protected]

Healthcare has become one of the hardest places in the market to pick winners. Over the past year, only ~11% of Healthcare stocks beat the S&P 500, and none beat it by 30% or more — the weakest breadth in 25 years.

But the bigger issue is that the usual quality playbook has stopped working.

We break down why that matters for portfolio construction inside the sector.

Interested in the full insight? → email [email protected]

Don't miss our monthly Trivector Takes webinar on Wednesday, June 3 at 11:00am EDT → https://t.co/mfaERQfN75

For most of the last two years, AI Semiconductors and AI Software moved at least moderately together. That relationship has broken sharply. In the last two sessions, the SOXX/IGV spread hit roughly 275 bps the first day and more than 350 bps the next.

The fundamental story for software is not clean, but the risk profile may be changing anyway.

We break down why that matters for investors already crowded into AI exposure, and which software names we would consider adding.

Interested in the full insight? → email [email protected]

Don't miss our monthly Trivector Takes webinar on Wednesday, June 3 at 11:00am EDT → https://t.co/mfaERQfN75

Our founder, @Adam_Parker_Tri, joined @CNBC 's @SquawkStreet on the Street to discuss his market expectations, modern playbook for the market, and more.

Watch the full segment here:

https://t.co/He8loqwMrN

The classic defensive playbook has a market-cap problem. Pharma, Telecom, Staples, and Utilities were nearly 30% of the S&P 500 twenty-five years ago. Today, they are just over 10%.

So if investors need defense before year-end, where can they actually find it?

We screened the industries that have historically held up when the market pulls back — then filtered for momentum, forecast EPS growth, and asymmetric beta.

Interested in the full insight? → email [email protected]

Our founder, @Adam_Parker_Tri, joined @CNBCClosingBell to discuss how investors should be thinking about equity markets.

Watch the full segment here:

https://t.co/MKmPQmIp3i

We parsed the earnings call transcripts of 1,465 companies — roughly $56 trillion in market cap — and filtered for what executives are actually saying about Hormuz, oil, sanctions, and the Middle East.

36.2% of companies had substantive commentary. Taken together, the net impact across the mixed, negative, and positive readings translates to roughly 10% of the US equity market's market cap.

But the sector dispersion is where it gets interesting. One sector's transcripts skew overwhelmingly negative — and we think Wall Street analysts are being complacent about estimate achievability there.

Interested in the full insight? → email [email protected]

Don't miss our monthly Trivector Takes webinar on Wednesday, June 3rd at 11:00am EDT → https://t.co/mfaERQfN75