The Strait of Hormuz has become the single most important risk to global oil and LNG markets.

Around 12 million b/d of crude and 80 Mtpa of LNG flows are currently disrupted, with outcomes now dependent on how quickly geopolitical conditions stabilise.

Our upcoming Horizons Live will explore three scenarios: Quick Peace, Summer Settlement and Extended Disruption and what each means for supply, prices and global economic stability.

We will cover:

- Diverging oil and LNG price trajectories under each scenario

- Risk of sustained inventory depletion and demand destruction

- Implications for global energy security and investment decisions

Our experts will also take audience questions live.

Join us as they assess how far-reaching the impact could be.

Register today. https://t.co/NnecaeGo8W

30 of the world's largest oil and gas companies face a production shortfall equivalent to nearly two Permian basins by 2040. It’s a gargantuan task and not every E&P will succeed.

#WMHorizons sets out how Big Oil will need to deploy every tool in the playbook to square the circle: https://t.co/mMJyg6Lk0e

The energy crisis is escalating, fast.

- Gulf infrastructure now in play

- LNG + oil prices surging

- Recession risk rising

Key insight: prolonged disruption could push Brent to $150+ and reshape global energy markets through 2027.

Read more in The Edge: https://t.co/5fbLFZakRq

🚨 Iranian strikes have knocked out 17% of Qatar’s LNG export capacity.

As QatarEnergy CEO said, 2 of 14 LNG trains and 1 GTL facility were hit. That’s 12.8 mtpa offline for 3 to 5 years - not weeks, years.

~$20bn in annual revenue gone. Force majeure on long-term contracts now likely.

And it’s not just LNG. Condensate, LPG, helium - all impacted.

This is a major hit to one of the world’s key supply hubs. The gas market just got a lot tighter. 🛢️🌍

What just happened in Qatar is a structural break for global gas and LNG markets.

This is not a marginal disruption. It is the core of the system.

Qatar had already halted LNG production earlier this month and declared force majeure, removing ~19% of global LNG supply. The latest strikes now raise serious questions about the timeline for any restart.

Before this, the market consensus assumed a short disruption. A few months of outage, followed by a gradual restart and a return to normal balances by mid-2026.

That assumption no longer holds.

Even under optimistic conditions, restarting LNG is not immediate. Upstream restarts, train-by-train ramp-up, and now potential repairs to damaged infrastructure all extend timelines. What was expected to take weeks could now take months.

And duration is everything.

At current run rates, every month of disruption removes roughly 1.5% of global annual LNG supply. After five to six months, the market is structurally short year-on-year, even before accounting for demand growth.

This shifts the entire balance.

Supply growth was expected to add ~35 mt in 2026. That is now at risk. Delays to North Field expansion projects could push tightness into 2027 and beyond.

The consequences cascade quickly:

First, pricing.

This is no longer volatility. It is a sustained repricing higher, driven by physical scarcity.

Second, demand.

Asia will absorb the shock first. Buyers most exposed to Qatari volumes will be forced into demand destruction, fuel switching, or high-priced spot procurement. Growth expectations will reverse.

Third, Europe.

Lower LNG availability means reduced storage injections and continued fuel switching. Storage levels risk remaining well below comfortable thresholds unless demand is curtailed further.

Fourth, system response.

Maintenance will be deferred. Every available molecule will be pushed into the market. Sanctioned or politically complex supply sources may be reconsidered simply because alternatives are limited.

Fifth, strategy.

This is a reminder of concentration risk. Ras Laffan is an extraordinarily efficient integrated hub. In peacetime, that is an advantage. In conflict, it becomes a single point of failure with global consequences.

Finally, reliability.

Gas markets are large, but not flexible. They cannot easily absorb shocks of this scale. Security of supply, diversification, and portfolio flexibility will move back to the centre of decision-making.

This is not a temporary disruption.

It is a reset of how the market prices risk, reliability, and concentration in the global LNG system.

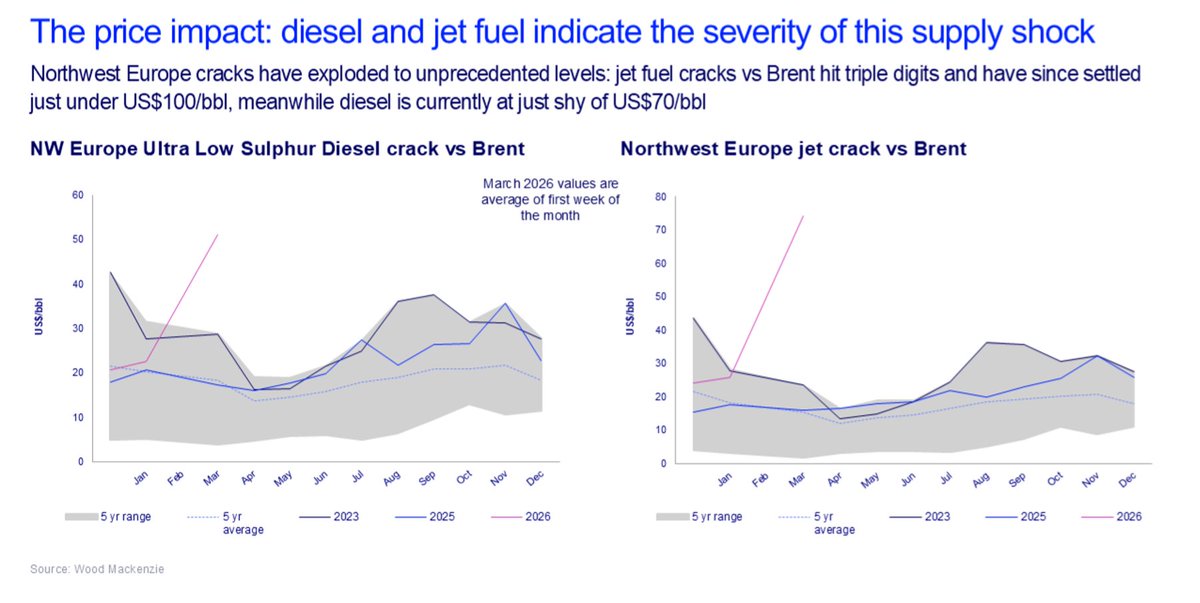

Brent has leapt US$30/bbl to over US$100/bbl in the 10 days since the start of the US/Israel war in Iran. As the conflict intensifies, the oil market is moving into a higher-risk environment. Prices are not yet reflecting a full supply crisis, but tensions are escalating by the day.

What’s next for the oil market and oil price? How much higher could Brent go? Get our analysis in this special edition of The Edge: https://t.co/Z0SqoL4wYb

Big Oil is recalibrating for the next decade. Q4 results show a clear strategic pivot:

- Strengthening upstream portfolios to avoid production decline

- Cutting costs and trimming investment amid weaker prices

- Scaling back buybacks as balance sheets take priority

- Eyeing AI, data centres and selective low-carbon plays

What do the latest results reveal about the Majors’ outlook on commodities, US gas, M&A and consolidation?

Find out in the latest Edge: https://t.co/16EpNXxR3j

European industrial competitiveness has been hit hard by soaring gas and electricity prices that have widened an already significant price gap with the US and China. A new wave of cheaper LNG supply could be about to throw a lifeline – but can it close the gap? Learn more in #WMHorizons: https://t.co/cIR08d08eJ

Few oil and gas companies have set net-zero targets for Scope 3 emissions, despite pressure from emerging regulations and mandatory reporting requirements. Download our infographic to understand how companies can start addressing Scope 3 emissions: https://t.co/va4BmJIp1L

A Republican sweep of the Executive and Congress could result in significant changes to the #IRA. Read on for an exploration of some of the key impacts of this severe downside scenario: https://t.co/3QwuC6kdxP

Five firms, including three in north-east Scotland, are being combined by their private equity owners to create D2Zero - a decarbonisation business with 4,000 people.

#EnergyTransition@hydrasun@FuelCellSystems@Powerstar@scoregroupltd and Global E&C.

https://t.co/IrNFQobDKH

Decarbonisation and energy solutions firm D2Zero has announced an expansion of its executive team and board as the group continues to build its leadership capability.

#decarbonisation#energytransition

https://t.co/3yerKc0KOp

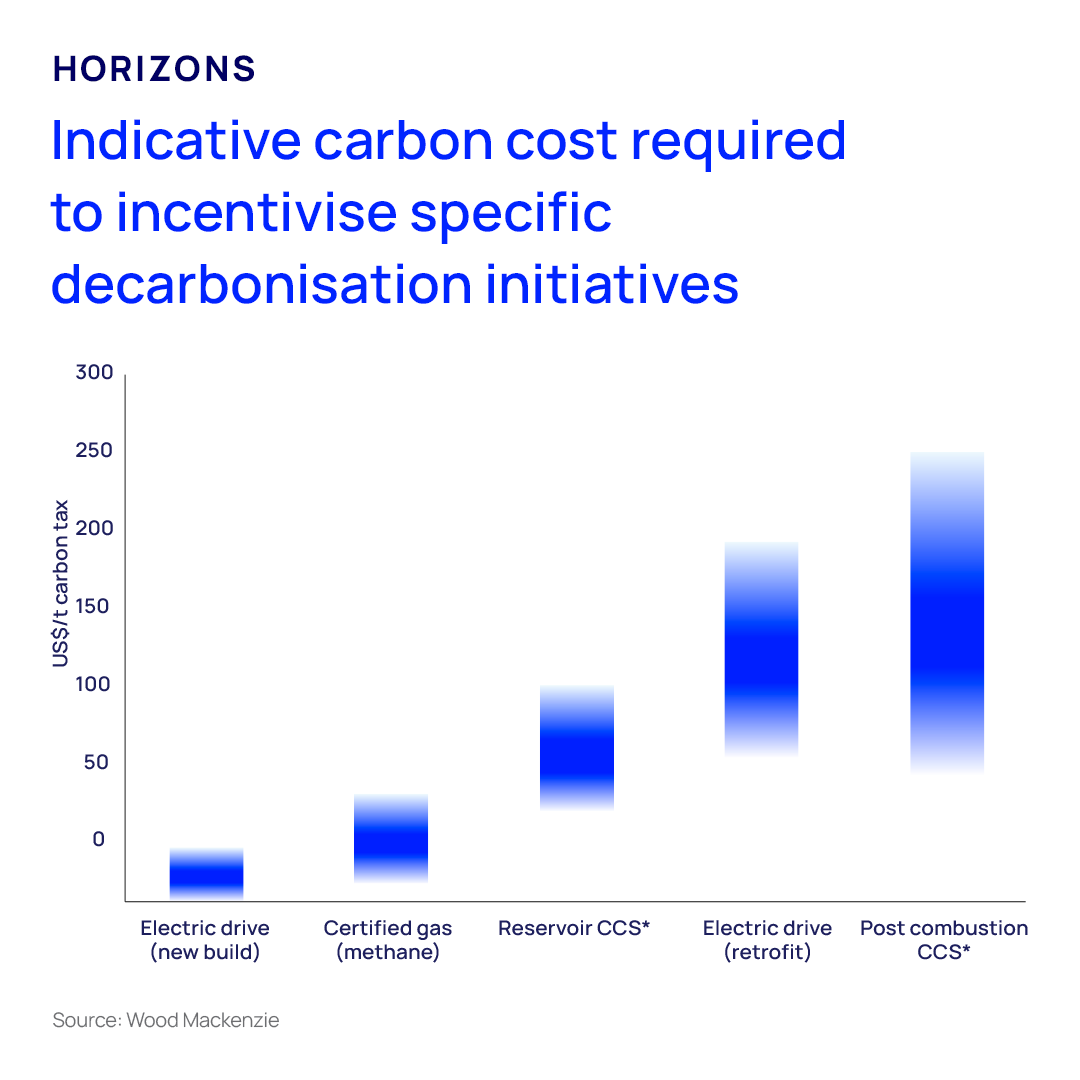

What are the options for reducing #emissions? Post-combustion CCS has been proposed in the US, where the 45Q tax credit is available. Worth up to US$85/t, the credit still falls well short of the cost of most post-combustion CCS developments. https://t.co/gy3guyrl50 #WMHorizons

The latest geothermal systems have the potential to be used more widely than before, poising geothermal energy as the next best low-carbon solution. But what’s the commercial potential for geothermal energy? Find out with our report: https://t.co/eCOAmoCL36

#geothermalenergy

In case there is any doubt if we should continue producing O&G in the UK..Our current supply will not cover our needs even in a Net Zero (1.5deg) scenario. We seem to preferring imports which will be 5x more carbon intensive. #energyliteracy#commonsense @WoodMackenzie

Net Zero holds the promise of a sustainable future, but can the energy trilemma be solved whilst maintaining economic growth and prosperity in society?

Join SCDI & @OEUK_ for this networking Q&A event with @VCKretzschmar

➡️https://t.co/tRlH05Q11T

Today at #COP27, #EnergyTransition Director, Dr @VCKretzschmar presented at a plenary session discussing #decarbonisation of the oil and gas sector and the issues posed by global energy, economic and climate challenges

Passes for COP27 have arrived!

Hope #cop27 will deliver real solutions to real problems, including how to acccelerate decarbonisation of oil and gas production, which will continue to play a critical role in the global energy mix for at least a couple of decades.

#decarbonisation