Sometimes it's time to reflect, to stop and look at where we are now, where we've been, and how things have changed. It's mainly about investing and putting capital into assets and trading.

Basically, the temperature in the hospital is as follows. All the trading gurus, influencers, and I, who were squeezing the franc and pushing the PP1:100, have suddenly disappeared and changed our narrative, presenting information about how they trade. Tech trading enthusiasts and those with ICT tattoos on their chests quickly switched to algorithms, statistics, and macro. The old methods no longer work, and no one is showing off new methods.

Newbies who only buy into the market with a higher probability of leaving without a complex take profit. Those who flipped NFTs, then memes, got officially slashed and deleted all their apps with $0.23 on their balances. On-chain analysts have retrained as detectives. ETF fans and those who threw a Molotov cocktail at the Fed office are now joining forces and piercing the Trump voodoo doll.

Who's left? What happened?

The assumptions that laid the foundations for retail have proven wrong. Whether due to illiteracy, unfinished eighth grade, or wild imagination. Trump helped himself, not the market. The adherents of macro and classical markets have earned their keep. All those who said "yuck" about options, news analysis, and automation in 2020 are now trying to adapt their trading. The AI, and the way it was waxed, said it was a joke—now it's the opposite: everyone is determined to make it routine.

A few actions from me.

• Don't completely deny everything and never say that the world can turn 180 degrees and you'll be proven wrong.

• Test your hypotheses and implement innovations into your life. Include routine, basic manual tasks. Then scale further.

• Stay hungry and never think you're at the top of the mountain. After achieving success, you need to simultaneously test a new, alternative iteration on how to get to the top. Like in a game: complete a mission, find another way to complete it. I need to work 10 times harder to stay on top, otherwise, suddenly, someone smarter, more agile, and faster than you will.

• Break old canons and don't remain a follower of old systems. A system is your way to take profits. Don't get emotionally attached to it; create something new.

• Invest in yourself. Be it a new course on trading, macroeconomics, statistics, or anything else. In the long run, it will come in handy. In the worst case, show others that you have expertise in something else. In the best case, you can use it as an example.

Hug. Connection.

If the market is pricing in fewer rate cuts, but the terminal rate remains stable, this is more likely a case of delayed easing than a hawkish shock.

If the terminal rate itself begins to shift significantly higher, and the forward rate curve rises sharply at the far end, this is a hawkish regime shift—and that's when the dollar begins to receive an influx of demand that creates a strong tailwind.

Jerome Powell will go down in history for more than just inflation. Perhaps his greatest test had nothing to do with rates at all.

During his eight years at the helm of the Fed, he weathered a pandemic, the sharpest inflation spike in forty years, a mini-banking crisis in 2023, and a series of internal scandals. But the final chapter of his career proved political: open pressure from Donald Trump, a Justice Department investigation, and a de facto fight for central bank independence.

The irony is that by the classic criterion for a Fed chairman—inflation—his record looks mixed. Prices never returned to the 2% target, and the word "transitory" became one of the most costly forecasting miscalculations in the history of American monetary policy. And yet, it was Powell who steered the economy through COVID, implemented one of the most aggressive rate hikes since Volcker, and seemingly achieved a rare "soft landing."

In this new article, I explore:

🛑why the "temporary inflation" error doesn't negate his legacy;

🛑how the pandemic changed the very doctrine of the Federal Reserve;

🛑why Trump turned the central banker into a political figure;

🛑and why historians will likely remember Powell decades from now.

This is a story about more than just rates and inflation. It's a story about how a technocrat unexpectedly found himself the last line of defense for one of the key institutions of the American system.

Inflation today may indeed resemble the 1970s, but this is a different economy.

Back then, the system was younger and more resilient. Strong unions, wage indexation, a lower debt burden, a different energy consumption structure, and a Federal Reserve that could ultimately raise rates to double-digit levels and severely suppress demand. The economy withstood it.

Today, the structure is much more fragile. The population is aging, debt is higher, the economy is more tied to financial assets, and interest rate sensitivity has become almost painful. Every move higher in yields immediately hits mortgages, auto loans, credit cards, commercial real estate refinancing, and, most importantly, the cost of servicing federal debt.

This is where the analogy with the 1970s begins to break down. Back then, inflation could circulate for a long time through wages, raw materials, and final prices. Now, the energy shock is hitting a system already overburdened by debt and shrinking real incomes. Under such conditions, inflation quickly turns from a self-sustaining cycle to a erosion of demand.

There's also a statistical problem. The CPI of the 1970s and today's CPI are not directly comparable. This is especially true for housing, where the modern index relies on OER and rent components, which significantly lag and smooth out real dynamics. Superimposing the two periods and drawing direct conclusions is, to put it mildly, risky.

In the 1970s, the key mechanism was the wage-price spiral. Today, it's a squeeze on basic expenses. First, energy, transportation, food, insurance, utilities, and financing costs rise in price. Then, households cut discretionary spending. Businesses lose margins. Credit conditions tighten. Hiring slows. The labor market is the last to react.

Inflation could very well accelerate again, and the internal components of the CPI and PPI are already showing this. But the main question is whether the economy can withstand another wave of price growth.

My baseline scenario is simple. Not "a return to the 1970s," but "inflation now, demand destruction later."

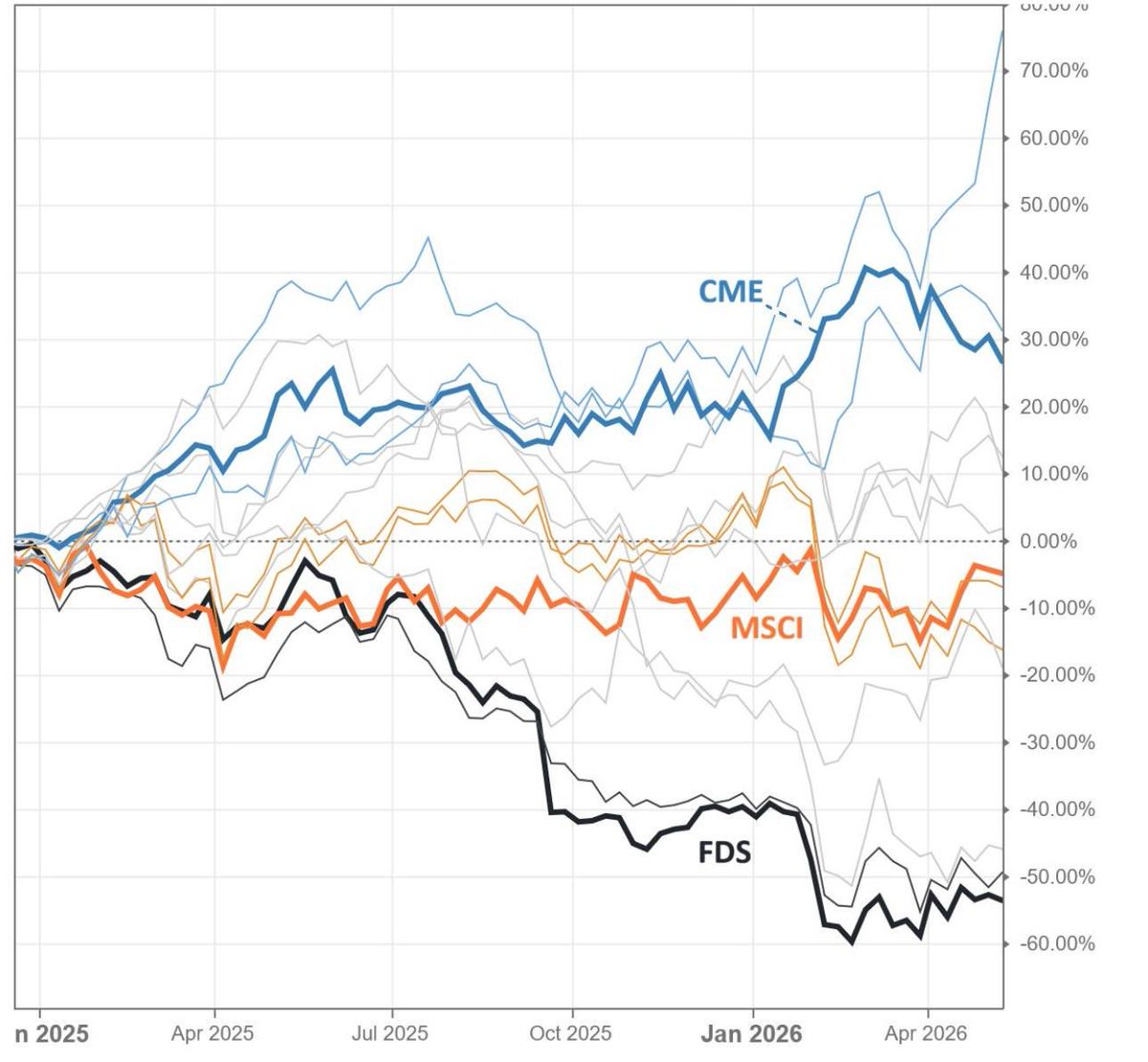

The financial data market still follows a simple logic: maximum value is created either at the source of the data or where it's converted into intelligent products. The economics in the middle, in distribution, are noticeably weaker.

This can be described as a "smile curve." The market confirms this pattern. CME Group has grown, MSCI has remained largely stagnant, and FactSet has declined. And it's not about AI or the quality of management. It's about where the business is in the value chain.

CME Group is a production facility. An exchange where prices are created. The cost of each additional transaction is almost zero, and monetization occurs twice: first, the commission for the transaction itself, then the sale of the data generated by that transaction. The same price signal can be licensed indefinitely, and any increase in volume is almost entirely lost to profit.

MSCI is an activation facility. The company takes existing data and turns it into indices, risk models, and benchmarks. The product is created once and used for years. Revenue is tied to assets under management, not to clients' investment performance. Scalability is almost built into the model itself.

FactSet is a distribution company. The company collects data from hundreds of sources, cleans it, and delivers it to clients via a terminal. The business is high-quality, with subscriber retention at around 95%, but the cost structure is more rigid. More data means more integrations, more quality control, and greater operational complexity. Hence the natural margin ceiling.

This is why CME and MSCI consistently trade with higher margins and multiples than FactSet. The value chain itself sets the ceiling for the business.

AI can steepen this curve even further. But it likely won't be able to invert it.

US inflation rises to 3.8% year-on-year

This is the highest level since 2023.

It was expected to be 3.7%.

Markets have already reacted by falling.

Meanwhile, Trump in his fictional world: "Laser, bam, bam, no",