🦔Chinese memory chips just showed up inside a Corsair Vengeance DDR5 retail product, which means American consumers are now buying RAM made outside the Samsung, SK Hynix, and Micron cartel that has controlled the market for 30 years.

HP placed major LPDDR5 orders with ChangXin Memory Technologies (CXMT) in January, Qualcomm began custom DRAM work with the company in April, and Dell, Asus, and Acer have all approached the manufacturer. CXMT and YMTC are both doubling production capacity this year. This comes as memory stocks rallied through 2025 on AI-driven demand and tight supply.

My Take

The memory cartel is about to get its first serious competition in 30 years. Samsung, SK Hynix, and Micron have controlled the global DRAM market so completely that the industry refers to itself as a cartel openly, and they have been printing money this year because AI demand outran their willingness to expand capacity. CXMT showing up in Corsair retail products is the moment that pricing model starts to crack. Chinese chips broke DDR3 and DDR4 pricing on the way in, and DDR5 is now next in line for the same treatment.

This connects directly to the Seagate post earlier this week. Seagate's CEO told JPMorgan on Monday that building new factories would "take too long," and the stock fell 6% because investors heard "we cannot meet demand." If CXMT meets that demand from outside the cartel, the supply tightness that justified the memory ETF rally collapses fast. The $10 billion that piled into Roundhill's DRAM ETF in six weeks priced in a world where supply stays constrained for years. A Chinese competitor doubling capacity through 2026 and now shipping to American brands like Corsair changes that math. The political risk is real, since CXMT could still get added to the US blacklist, but European markets are already open and the trade routes for memory chips do not respect Commerce Department guidance.

Hedgie🤗

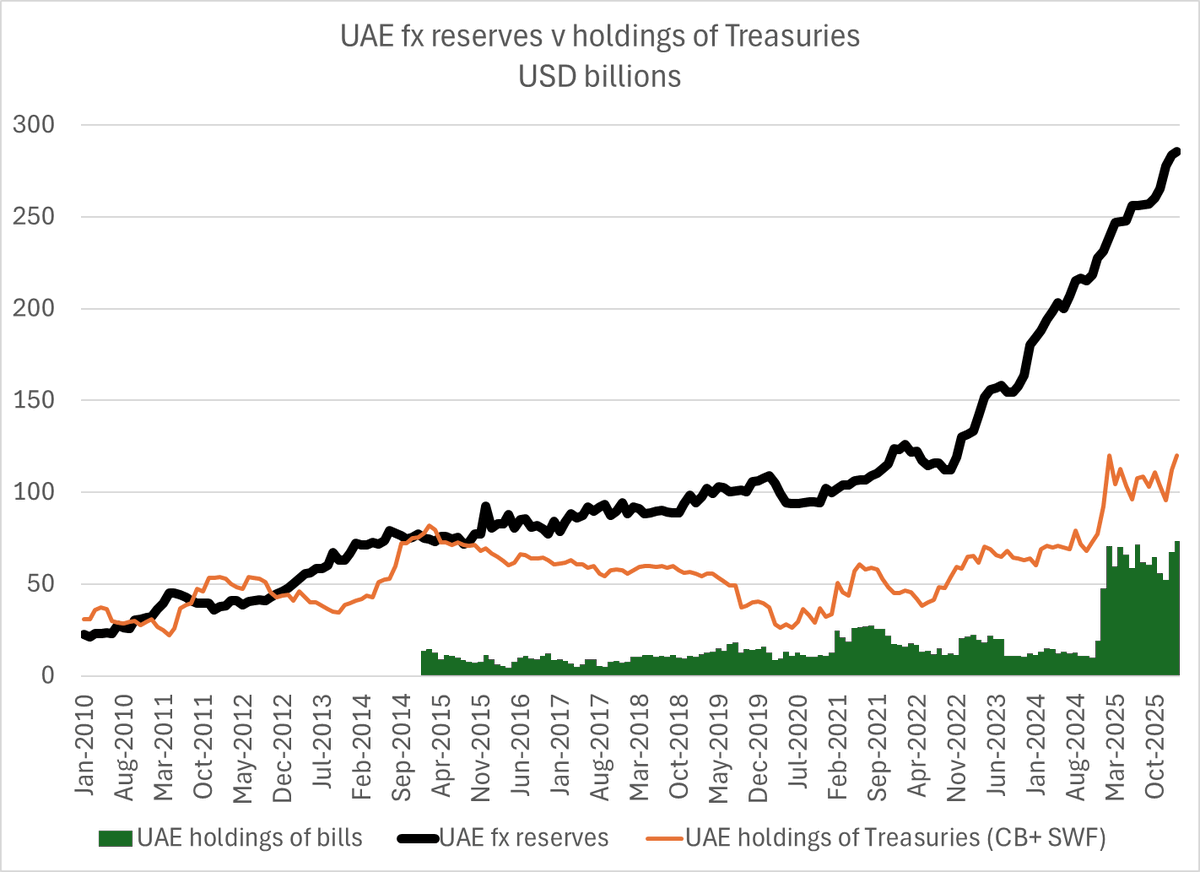

Interesting WSJ story about the Emirates request for a swap line --

the UAE hasn't reported its end March reserves but it went into the conflict with tons of reserves and no shortage of liquid bills in US custodians

1/

Asia now represents 49% of the global economy in PPP-adjusted GDP terms, totaling $219.2 trillion. The world’s three largest economies: China ($43.5T), the United States ($31.8T), and India ($19.1T) together account for 43% of global output.

Given that Asia is also the most populous continent, home to 58.6% of the world’s people, it has evolved far beyond its role as the “world’s factory.” It has become the primary engine of global demand growth. Investors can no longer afford to overlook this fundamental shift and should position their portfolios accordingly.

https://t.co/zt5IzA7a4g via @visualcap

Amid ongoing tensions in the Middle East, Chinese assets demonstrated remarkable resilience. Even GS maintained its “overweight” recommendation on Chinses stocks. Chinese assets have become a safe haven for several reasons:

- China has a diversified energy structure unlike South Korea, Japan or Taiwan.

- Valuation of the Chinese stock market (A-share) is at low point. The trailing 12 months P/E of Shanghai Composite Index is about 17 times, compared to 27 times for the S&P 500, 23 times for the Korea Composite Index, and 21 times for the Nikkei 225. So even in the face of external shocks the downside potential for A-shares looks more limited compared to, especially to overvalued tech US stocks.

- Chinese supply chains have demonstrated resilience. For the manufacturing sector, the stability of supply chains and the reliability of deliveries have become more important than pricing.

- The final, but not the least reason is the strong consistency in China’s macroeconomic policies and the optimization of its capital market system.

In the eyes of foreign investors, China is becoming an increasingly reliable and predictable counterparty with the Yaun becoming more and more involving in international transactions.

Sugar #11 is the only major tradable commodity in the US that still hasn't surpassed the nominal price peaks it hit in the 1970s and 1980s. It could very well become the next big story like Silver or even earlier examples such as Cocoa. I've been following sugar closely for the past two years, because one day there will likely be a similar narrative unfolding in the sugar market as we're seeing right now in the metals complex.

$SB #Sugar #Softcommdities

Telegram has fully repaid the bonds issued 5 years ago. Since then, Telegram has built an innovative monetization strategy and reached profitability in 2024.

Congratulazioni a Kimi Antonelli per la straordinaria vittoria nel Gran Premio di Cina. A soli 19 anni, un talento italiano torna sul gradino più alto del podio in Formula 1 dopo vent’anni.

Campione.

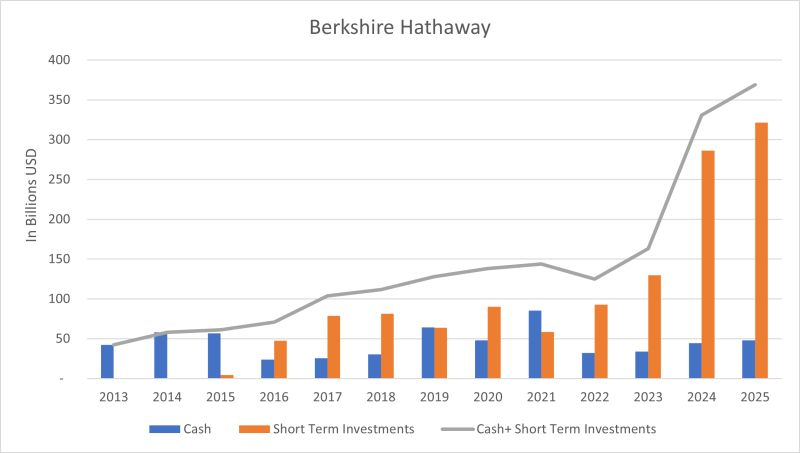

Berkshire Hathaway released its 2025 financial results on Saturday. This marks the final report under Warren Buffett's leadership as CEO, with Greg Abel officially taking over the role starting in 2026 (Buffett remains chairman). The company's cash position (including cash equivalents and U.S. Treasury holdings) reached a record $373.3 billion as of December 31, 2025. This reflects an increase year-over-year (up about 11-12% from the end of 2024), though it dipped slightly from the third-quarter peak of roughly down 2%.

In his first shareholder letter, new CEO Greg Abel described the massive cash pile as "strategic dry powder" for future opportunities, emphasizing that it doesn't signal a retreat from investing. He pledged to maintain Buffett's disciplined, long-term approach and Berkshire's fortress-like balance sheet. Operating earnings declined (notably due to insurance headwinds), but the focus has been on the cash buildup and leadership transition.

$BRK.B #BerkshireHathaway #WarrenBuffett #GregAbel

The Chinese stock markets (mainland and Hong Kong) have experienced a prolonged period of correction and sideways consolidation since the 2007 peak. This pattern is likely to persist for the next few years, resembling the U.S. stock market's roughly 20-year recovery phase after the 1929 crash (see the chart with orange cercle), where the Dow Jones languished in a broad range before eventually breaking out into sustained growth. In the next decade, China will witness a transformative, highly positive shift potentially comparable in scale and impact to the explosive U.S. market growth that followed the Great Depression era. As minimum, capital flow restrictions will be lifted somewhere next decade in China.

We are now in a period of global paradigm shifting. To weather the volatility and potential upheavals ahead, consider rotating away from overvalued tech sectors (which have dominated recent cycles) into currently undervalued, under-owned hard assets including precious, critical and base metals, commodity producers, mining companies, and related resource firms. These areas perform well during periods of economic rebalancing, supply constraints, and shifts toward tangible value.

BREAKING NEWS

A US GOVERNMENT-BACKED MINING INVESTMENT FUND HAS AGREED TO BUY A 40 PER CENT STAKE IN GLENCORE'S COPPER AND COBALT PROJECTS

It is raining now.

Yesterday, silver closed at a record all-time high of $56.72 per ounce, decisively broken above 45-years resistance level established in 1980 and 2011, followed by a successful retest of that level over the past few weeks. Now silver is trading entirely in uncharted price territory.

Assuming that the immediate gold target is $ 5000 per ounce with possible short squeeze up to $6 000 once it touches $5 000, I don’t exclude silver traded at $100 with possible following massive short squeeze driving it toward $150. After which there will be a prolonged correction/consolidation.

Silver is now mirroring the exact setup gold had in November 2023, when it finally broke free from its multi-year consolidation phase.

$GC $SI #GOLD #Silver #silversqueeze