$wve will likely PR their ADA 2026 presentation tomorrow. I expect they concentrate on WVE-007 phase 1 data with detailed DXA scan metrics and MRI-PDFF readouts demonstrating targeted visceral fat reduction and lean muscle preservation.

Bought more in 5.70-5.80 area

$ABVX This is exactly the moment when M&A thesis might really materialize. Euphoria is over, pragmatic reality is here. M&A deals are rarely signed when execs and the board have too rosy valuation picture in their mind

1/5

The $IOVA crowd is dunking on $REPL's 19% ORR data today, treating cancer treatment like a CT scan beauty contest. But flexing ORR while ignoring the recent regulatory reality check on cell therapies misses the point. OS is what actually matters. 🧵

6/6

The Setup: market currently prices $IMCR strictly as a niche uveal melanoma business, pricing the pipeline at zero. Mature OS data heavily de-risks the ongoing frontline cutaneous Phase 3 trial, exponentially larger TAM provides a clean fundamental path for a major re-rating.

1/6

After ASCO 2024 $IMCR was sold because the market panicked over a low ORR, ignoring early ctDNA data, survival curves weren't mature. Today's ASCO release completely changes this, brene OS data unlocks the true potential of the ImmTAC platform. 🧵

https://t.co/XZ3JwaI2bc

5/6

Competitors pushing autologous cell therapies may post higher ORRs, those come with massive logistical hurdles, including lymphodepleting chemo and ICU monitoring. ImmTACs are off-the-shelf bispecifics: standard IV bags in community clinics, wat lower COGS, ease of admin

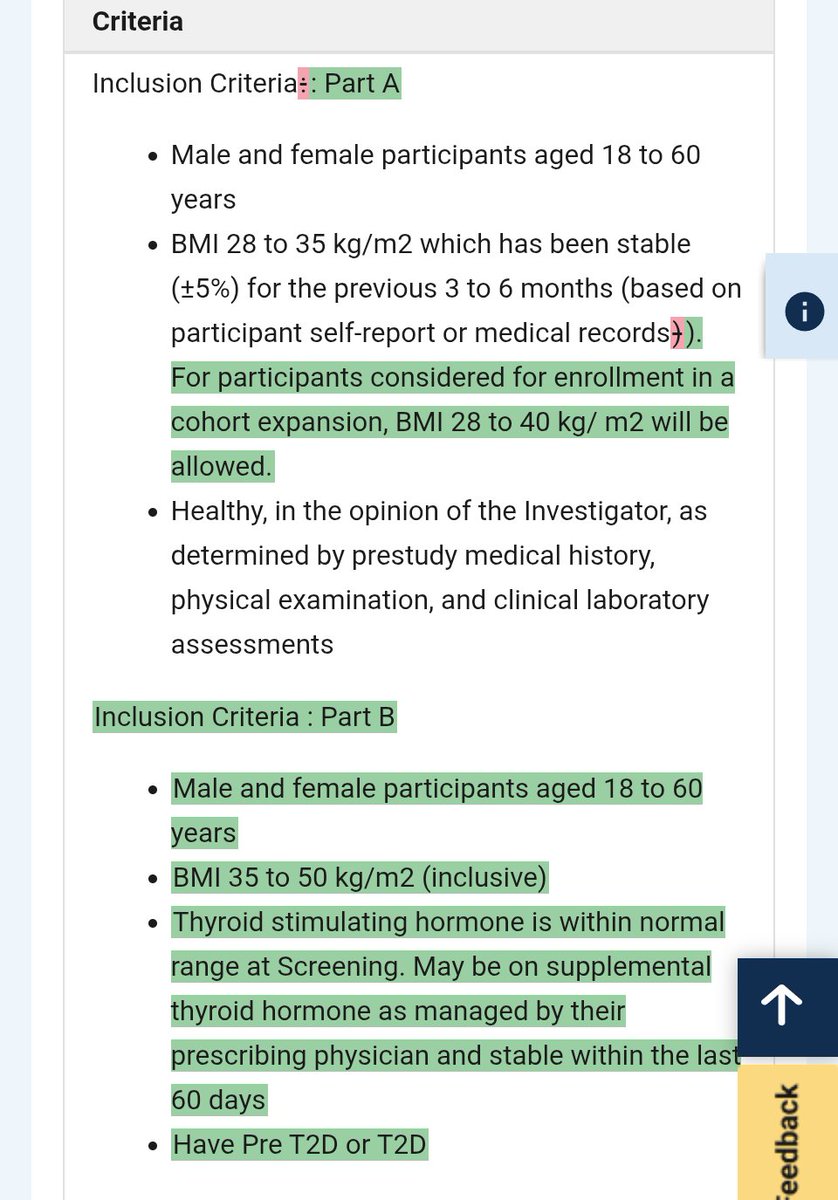

If you're $lly or $nvo and you want INHBE or ALK7 asset for the cardio metabolic future market , what would you do. Comment if you have another opinion $arwr $wve