I'm thinking of buying $NBIS for one simple reason.

Today, Nebius is running roughly 20k GPUs.

The plan is ~60k end of FY and ~240k by 2027+

That's a 5x fold increase.

And the CEO has hinted at something even more aggressive: up to 1 GW in 2026

That’s the opportunity.

The move Zuckerberg is making with Llama is one of the most strategically elegant plays I have seen from any tech CEO in years and I do not think the market fully appreciates it yet

By open sourcing Llama they commoditized the base layer of AI, built a developer ecosystem of tens of thousands of researchers essentially giving $META a free external R&D subsidy, and then created the perfect setup for New Spark, their premium cutting edge model, to be monetized through paid APIs and subscriptions

You commoditize the standard, then you monetize the premium

When I put that alongside $354B in projected revenue by 2028 and operating margins that keep expanding, the current price starts looking like a very patient person's entry point

Am I the only one surprised that $ADBE isn’t down +5% on $AAPL ‘s WWDC showcase and Siri AI capabilities, and more so on never seen before Image capabilities

I think we have bottomed on $ADBE stock

$META won't catch a break any time soon.

But this whole sell-off might create an enormous buying opportunity

Dilution isn't great, but I'm up 400% on $META , and could very much significantly double that over the next few years

1.1. Question 28: What happened 1973 and 1974 when your investment firm lost over half?

Charlie: Oh, that’s very simple. That’s very easy. That’s a good lesson. That’s a good question. What happened is the value of my partnership where I was running, went down by 50% in one year. Now the market went down by 40% or something. It was a once in 30 year recession. I mean monopoly newspapers are selling at 3 or 4 times earnings. At the bottom tick, I was down from the peak, 50%. You’re right about that. That has happened to me 3 times in my Berkshire stock.

so I regard it as part of manhood. If you’re going to be in this game for the long pull, which is the way to do it, you better be able to handle a 50% decline without fussing too much about it. And so my lesson to all of you is conduct your life so that you can handle the 50% decline with aplomb and grace. Don’t try to avoid it. (applause) It will come. In fact I would say if it doesn’t come, you’re not being aggressive enough.

1.2.

“I regard it as a part of manhood. If you’re going to be in this game for the long haul which is the way to do it. You better be able to handle a 50% decline without fussing too much. Conduct your life so you can handle a 50% decline with aplomb and grace. Don’t try to avoid it. It will come. And if it doesn’t come I’d say your not being aggressive enough”.

Is anyone actually going to buy SpaceX at $135 per share and a whopping valuation of $1.7 trillion (?), making it the 7th largest company in the US

It's only growing at 34% top-line growth

At a P/S of just under 100, is this valuation justified?

Probably not..

Something about this market continues to bother me and I think it is worth saying out loud.

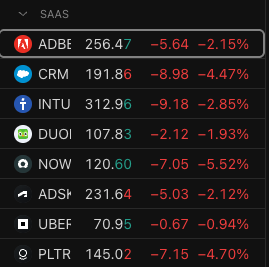

SaaS companies, businesses that grow revenue every quarter, expand margins, generate real free cash flow, and embed themselves deeper into enterprise operations with every single renewal cycle, are selling off like the model is broken.

Meanwhile, AI infrastructure names with no earnings, triple digit multiples, and a runway that depends entirely on a capex cycle continuing indefinitely are being treated like they are the safest thing in the room.

I understand that the market is forward looking and that AI is genuinely a transformational wave, I believe that too, but there is a difference between pricing in a revolution and pricing in perfection with no margin for error on one side while simultaneously throwing away the receipts on the other.

Some correction in SaaS is healthy and overdue, I have said that before, but what we have been seeing over the last 1-2 years does not feel like rational repricing, it feels like capital chasing heat and leaving behind the compounders that will still be growing quietly and profitably long after the current narrative cycle has moved on.

The market has done this before and it usually ends the same way: the businesses with real economics win, just not always on the timeline the crowd expects.

@giorgio2571 At this market nah. However while fundamentals improve I'm a super happy shareholder, and would gladly buy more if the market gives it to me below $180 again

$MRVL's operating profit growth is subject to skyrocket, while revenue is expected to grow at high 40% / low 50%

With FCF subject to grow up to 250% y-y in the next few quarters, $MRVL could be trading at a discount

$MRVL is up over 15% in overnight trading after $NVDA CEO Jensen Huang called Marvell “the next trillion-dollar company” at Computex.

Data center is now ~76% of revenue putting Marvell at the custom silicon and interconnect chokepoint of the AI buildout.