🔬New Research: Exploring Multiple Methods for Forecasting Multivariate Volatility for Risk Indifference Pricing in Perpetual Contracts.

A thread 🧵 (1/8)

Want to jump into the discussion? Visit here:

https://t.co/aOeFBkzBLf

The $TRB market manipulation incident is a vivid demonstration of problems across perp DEXs.

Here’s what happened:

Perp DEXs let traders take on large amounts of leverage, while using Open Interest (OI) caps to limit the total amount of open positions for each asset to manage risk.

Low liquidity assets can become targets for market manipulators because it’s easier to influence their price. By engaging in coordinated buy orders across multiple exchanges they can artificially pump the price.

If OI caps aren’t set correctly, traders can take on much larger positions than what is appropriate.

Eventually, these artificially inflated prices become unsustainable and market manipulators sell off their positions which causes a crash.

In the case of Synthetix, this means stakers (aka LPers) incurred millions of dollars in losses.

Risk parameters need to be responsive to market conditions and riskiness of assets.

In a volatile market event like the $TRB price surge, @VestExchange’s protocol owned liquidity would be the first to absorb the impact and shield LPs from immediate losses.

In addition, Vest calculates the exact capital needed to ensure exchange solvency and LP risk - it charges trades the exact fees needed to be paid to LPs for this risk.

In the case of highly imbalanced markets like $TRB, fees and funding rates paid to LPs and the exchange would have automatically increased, covering potential losses. Unlike other DEXs, these fees are the exact fees needed to ensure that the exchange and LPs are made whole.

Other DEXs, like Synthetix, would have manually and arbitrarily increased their fees in correlation with imbalance, but not with the precision and purpose of counterparty solvency. In the case of Synthetix, the human dependency and manual fine tuning of fees was not enough to cover LP losses.

Vest’s approach is dynamic, automatic, and responsive, offsetting LPs heightened risk exposure with higher earnings and AMM capital protection. In my opinion, this makes Vest currently the most capital efficient and decentralized DEX in the space.

I will soon be publishing official simulation results of Vest on $TRB. Stay tuned for a follow up post!

Given recent discussions on vAMMs, here is our take on how a vAMM with a proper a risk engine can distribute liquidity much more efficiently than on orderbooks.

Write-up:

https://t.co/hhEGBqQfwi

Discussion:

https://t.co/rvGqCd96xp

👇👇👇

1/13

Join us for a technical fireside chat with @PrimitiveFi 🪵🔥

Topics covered...

- Modeling risk and trading strategies with Arbiter

- The Financial Virtual Machine (FVM)

- Tying these into their newest product: Portfolio

Join us at 9:30 AM EST 4/13👇

https://t.co/KOxsSFkIz9

Join us for a technical fireside chat with @PrimitiveFi 🪵🔥

Topics covered...

- Modeling risk and trading strategies with Arbiter

- The Financial Virtual Machine (FVM)

- Tying these into their newest product: Portfolio

Join us at 9:30 AM EST 4/13👇

https://t.co/KOxsSFkIz9

Join us for a technical fireside chat with @PrimitiveFi 🪵🔥

Topics covered...

- Modeling risk and trading strategies with Arbiter

- The Financial Virtual Machine (FVM)

- Tying these into their newest product: Portfolio

Join us at 9:30 AM EST 4/13👇

https://t.co/KOxsSFkIz9

1/7 🧪 New Research: Optimal Liquidations via Convex Optimization

We design a liquidation mechanism to minimize the negative impact on AMM's solvency.

Let's dive in! 👇

https://t.co/ZmQPWBWtGT

7/7 🎯 Join the Conversation!

Got insights or ideas on objectives or reward mechanisms? Share your thoughts on our Discourse research forum! Let's collaborate and shape the future of liquidation mechanisms together. 🦾

https://t.co/ZmQPWBWtGT

1/7 🧪 New Research: Optimal Liquidations via Convex Optimization

We design a liquidation mechanism to minimize the negative impact on AMM's solvency.

Let's dive in! 👇

https://t.co/ZmQPWBWtGT

6/7 🧐 What's Next?

Our research can continue with:

- Designing reward mechanisms that encourage optimal liquidations in decentralized settings

- Developing alternative objectives tailored to specific protocols

Tune in to our upcoming AMA with @SmileeFinance to discuss Volatility and Risk!

It's a great opportunity for you to get your questions in on how we view these parameters as well as how we plan to approach them in our product development! 💡

4/4 12AM EST

https://t.co/xenpQf2R3W

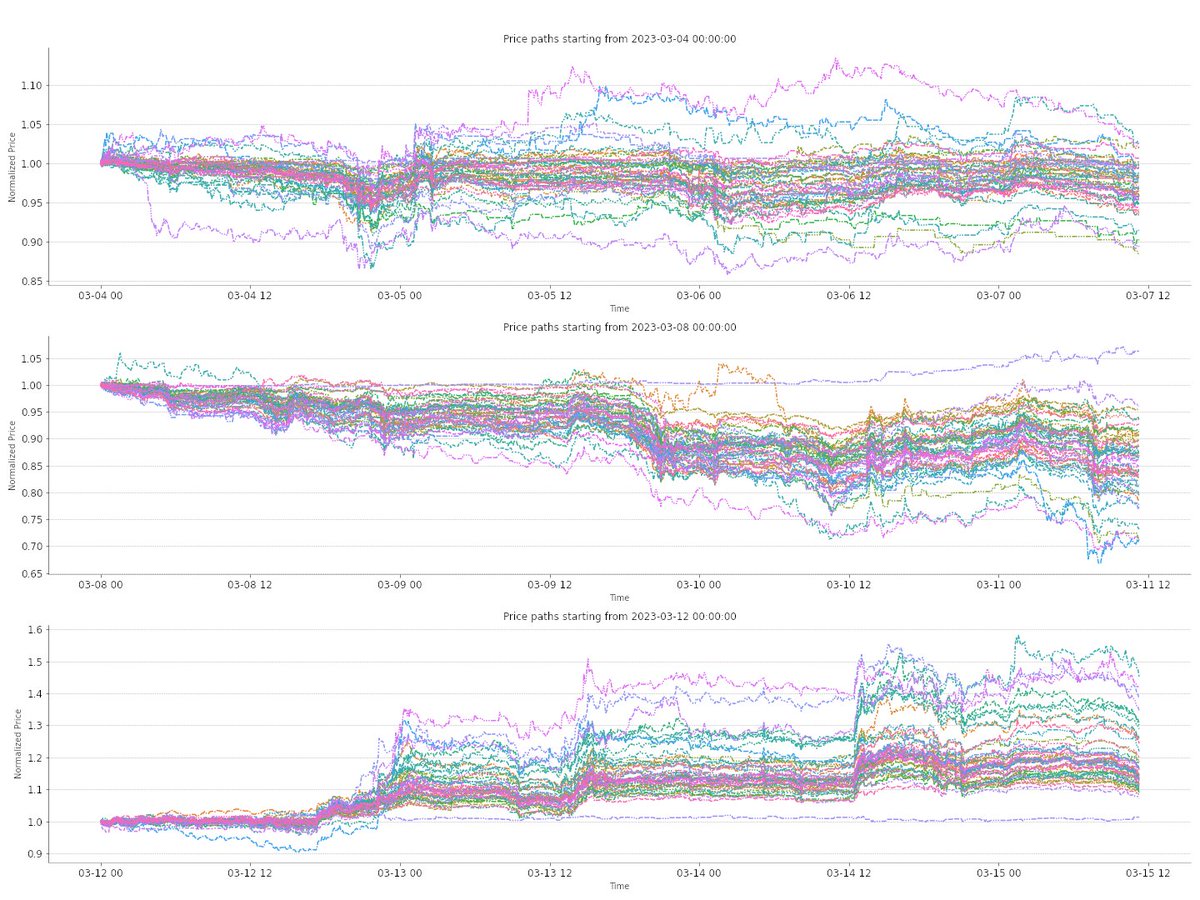

🔬New Research: Exploring Multiple Methods for Forecasting Multivariate Volatility for Risk Indifference Pricing in Perpetual Contracts.

A thread 🧵 (1/8)

Want to jump into the discussion? Visit here:

https://t.co/aOeFBkzBLf

8/8 Also, check out the full write-up for detailed description of forecast models as well as derivations for risk indifference pricing 📝🥼

https://t.co/Mos20bqF5r

🔬New Research: Exploring Multiple Methods for Forecasting Multivariate Volatility for Risk Indifference Pricing in Perpetual Contracts.

A thread 🧵 (1/8)

Want to jump into the discussion? Visit here:

https://t.co/aOeFBkzBLf

7/8 📚 Future Work

We will explore other hierarchical clustering methods, analyze MP law in practice, and apply Kalman Filters to denoise sample covariance. What other multivariate volatility forecast models should we try? 🧐

Join our discussion here!

https://t.co/aOeFBkzBLf