US payrolls surprise to the upside.

172k jobs added for May with upward revisions to prior months.

This print far exceeded the Dow Jones consensus estimate of 80k.

The 3 month average of monthly nonfarm payroll gains is at its highest since March 2024.

USD swaps market have fully priced in an interest rate hike by the end of the year and Treasury yields are trending higher across the board.

The USD is strengthening across both EM and DM currencies.

Headline Image Source: CNBC

#markets #macro #rates #fx

Taiwan overtakes India as the World’s Fifth Largest Stock Market. The Taiwan stock market has hit a fresh all time high and is up 52% year to date.

The market cap of Taiwan has now climbed to $4.95 trillion, behind only the US, mainland China, Japan and Hong Kong.

Meanwhile, the Indian Rupee traded at an all time low against the US dollar (at 96) and is nearing psychological resistance at 100.

Chart Image Source: TradingView

#markets #macro #fx

The US dollar is getting a renewed bid (DXY at 99.30 + 0.20) from the latest headlines coming out of Iran while market interest in EURUSD downside option structures, such as put spreads, gains traction. Short end rate differentials are slowly tipping towards favouring the USD compared to the EUR.

The 2 year US-German rate spread narrowed soon after the Iran conflict began. Given that Europe is a net energy importer, and particularly exposed to rising gas prices, the initial consensus was that ECB rates should ramp up higher. EUR OIS swaps are currently pricing a 90% chance of a hike next month.

The US was seen as being more insulated from any oil price shocks (particularly as they also have production at home.) US hikes were therefore being priced in less quickly and aggressively than compared to Europe.

However, this interest rate differential has now dissipated and we are back to where we were pre-conflict in the German-US 2 year yield spread. There has been strong US inflation (both in recent consumer and producer prints) with the recent FOMC minutes indicating that the Fed may ditch their easing bias.

Chart Source: TradingView

#markets #macro #rates #fx #trading

Pimco said that Japan’s 30 year bonds looked attractive while the curve was too steep. Meanwhile, Treasury yields fell from multiyear highs on a paring back of rate hike bets. Minutes from the April FOMC meeting will be out later today.

News Headline Source: Bloomberg

#markets #macro #yields

Long end 30 year US Treasury bond yields continue to surge and are very close to their highest since 2007 - currently trading at 5.15%. A few banking strategists are also warning that it could break through 5.5% - levels that were only last seen in 2004. Bond investors are seeking a greater yield as compensation for holding long term debt due to sticky inflation concerns, budget deficits and global uncertainty.

At the start of the year, the market was pricing in between 2-3 cuts for 2026. Now the market is pricing in even greater odds of a hike than a cut. Kevin Warsh is taking the helm at the Federal Reserve at a time when consumer and producer price inflation is surging and his first rate setting meeting in June will be pivotal.

Meanwhile, the US dollar continues to strengthen with escalating interest in downside EURUSD structures in the options market. Today the Indian Rupee also hit an all-time low against the greenback at above 96.5.

Chart Image Source: TradingView 30yr US Treasury yield

#markets #macro #rates #fx

UST’s and JGB’s continue to selloff as the Federal Reserve may have to eventually ditch their easing bias.

As Brent crude futures climb (rising above $110 a barrel earlier today) and cause concern about inflationary pressures, the global bond selloff continues and the effect of this is this being seen most in long end yields.

US 30 year yields have risen above the psychological 5% level and near to their highest since 2007. Meanwhile, Japan’s 30 year yields have surged to their highest since 1999 on fiscal concerns after the PM called for an extra budget.

Looking at other central banks, the market is pricing in an 85% chance of a hike from the ECB next month. Meanwhile, the UK 30 year gilt added over 25bps last week with UK politics driving the move and weakness in the cable currency pair.

News Headline Image Source: Financial Times (FT)

#macro #markets #rates #fx

Brent oil prices and global bond yields hit new year to date highs as we await a pivotal set of tech earnings out before the end of the week.

Image Source: CNBC

#markets#economy#macro

De-dollarization and currency diversification discussions continue.

Globally, the dollar still dominates foreign currency debt issuance, world FX trades and also reserve markets. Meanwhile, foreign investors are increasing their US TSY holdings.

Chart: TradingView

#markets

The US Dollar trades lower as risk remains well bid.

DXY's ascending channel seen during February and March has broken to the downside with April typically a weak month for the greenback based on historical seasonal trends.

Chart Source: TradingView

#markets#macro#fx

Gilt, OAT and BTP sovereign yields have continued to selloff.

Rise in borrowing cost from the February low point:

UK 10 year 4.23% to 4.80% (+57bp)

Italy 10 year 3.27% to 3.81% (+54bp)

France 10 year 3.22% to 3.68% (+46bp)

News Headline Source: Financial Times (FT)

#macro

US CPI Surges 0.9%

Today's US inflation print jumped by the most in almost 4 years with a 21% rise in gas prices compared to last month. The consumer price index (CPI) rose 0.9% from February and from a year ago it accelerated by 3.3%.

#economy#macro#markets

A weak US jobs report hits stocks as non-farm payrolls slid 92k last month (+50k expected) in one of the largest falls since the pandemic.

A negative payrolls number coupled with the jump in oil prices is causing stagflation concerns in the market.

#economy#macro#markets

The Brent oil price tops the $90 per barrel level for the first time since October 2023 as the Strait of Hormuz closure halts oil flows. Iraq and Kuwait are cutting output of their oil after running low on room to store their bottled-up crude.

#markets#economy#macro

Mexico is the largest silver producing country on the planet, supported by high grade deposits and a copious mining infrastructure. They produce over 6000 metric tonnes a year which is almost 2 X as much silver as the second largest country, China.

#markets#economy#macro

Donald Trump's new 15% flat rate global tariff will have varying impacts on different countries. With $133 billion in possible tariff refunds being debated in courts across the world, global markets seem to be interpreting this as tariffs rewritten not removed

#markets#tariffs

The market is looking to next week's inflation data for clues to the Fed's next move and pricing a 4% chance of a cut in January. 30 year mortgage rates have now dropped to their lowest in 3 years days after President Trump asked the US government to buy $200bn of mortgage bonds.

The Fed kicks off its 2 day policy meeting today with the market pricing in a 90% chance of a 25bps rate cut of the Fed Funds rate to 3.50%-3.75%. Look out for discussions and talk on balance sheet plans, financial stability and money market liquidity.

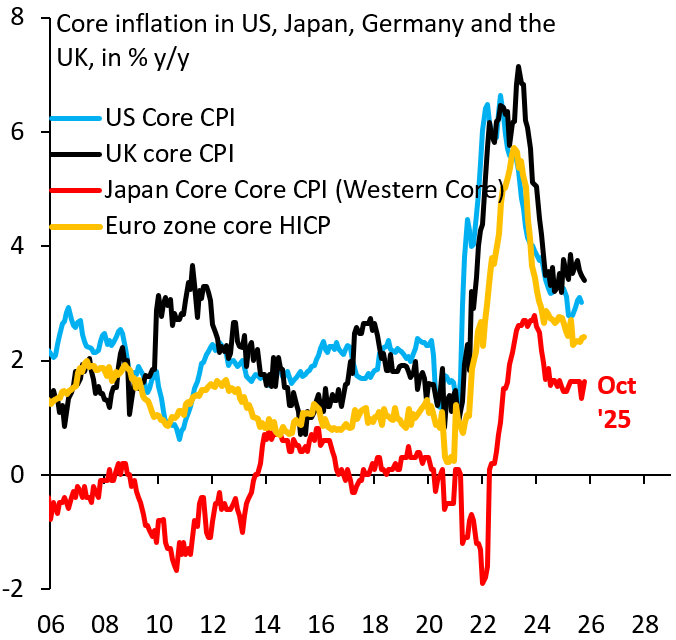

Core inflation in each of the G-4 has settled well above its pre-COVID equilibrium and in most cases is above the 2% target. That's not about supply shocks, but about demand and a global economy that's running hot. No wonder we have the "debasement trade."

https://t.co/PGLpL15cmJ