Finance Bill 2026 makes for an interesting & fairly technical read both from a tax policy & administration standpoint.

A 🧵 on the 11 things that stand out from what we are seeing so far for me.

It’s either my uncle Waruthu is heavily bewitched… or the man is the luckiest dropout kikuyu in the history of Kenya.

This man dropped out in Class 6. No degree. No biashara. No master plan. Just inherited land and some anointed timing.

He starts in Kingeero with a plot left by his father.

Then boom Western Bypass construction comes slicing through it, then KeNHA appears and tells him,

“Waruthu, kindly move, but first collect your 16 million.”

Now a serious man would sit down, call a fundi, maybe an architect, maybe even think of rentals, biashara, mabati ya tenants, something sensible.

Not Waruthu.

Waruthu buys land in Gitaru for 4 million, puts up a 3-bedroom house, then takes the rest of the money and launches a one-man campaign of alcohol, women and complete financial vandalism.

The man did not spend money. He attacked it.

Two years later, before the dust even settles, KeNHA returns again.

This time for the Gitaru-Kikuyu interchange.

I’m not joking.

Same man. Same story. Same government. Another cheque.

19 million.

At this point you stop calling it luck. This is now a calling.

He moves to Manguo near Limuru town, buys about three-quarter acre, builds again for around 4 million, then does exactly what he had done before.

Not almost. Not roughly. Exactly.

House first, then the balance is taken hostage by bars, women and enjoyment until nothing remains except memories and hangovers.

Any other human being would learn.

Waruthu?

Waruthu behaves like a man who thinks compensation is a monthly salary.

Then last November Ruto launches the Rironi-Nakuru-Mau Summit Road project.

Now tell me why this man’s land is again sitting next to the highway like it had been booked in advance.

Again the government comes.

Again they acquire.

Again Waruthu is paid.

This time 25 million.

You people, there are men who hustle for 20 years and never smell 5 million.

This fool has made a full career out of being removed by road projects.

He doesn’t farm.

He doesn’t build wealth.

He doesn’t invest.

He just keeps positioning himself where tarmac will eventually develop feelings.

The last report we got was that he had moved to Ponda Mali in Nakuru.

Either there’s a powerful mganga somewhere blessing his land papers… or God has a very twisted sense of humour when it comes to my uncle.

The man is turning Kenyan infrastructure into his personal ATM.

Respect. 😂

Most Kenyans have no idea what’s happening in Parliament today.

Silently… almost deliberately out of the public eye… a new SACCO system is being pushed through — and it could change how your money is controlled forever. This is Not just oversight — control.

This entity will:

• Hold funds from multiple SACCOs

• Control liquidity across the sector

• Run payment systems

• Lend to SACCOs

• Invest pooled savings

In simple terms?

Your SACCO money may no longer just be in your SACCO.

It could be moved, managed, and influenced from the center.

And here’s the part that should worry you:

Your savings are only protected up to KSh 100,000.

Anything beyond that? Not guaranteed.

This isn’t just a policy change.

It’s a fundamental shift in who holds power over your money.

Kenya's Controller of Budget has flagged delays in settlement of Treasury Bond Interest obligations to the tune of Kes 53.56 billion.

The delays were as follows:

· Kes 25.79 billion that was due on June 16th, 2025 but ended up being paid on July 15th, 2025

· Kes 15.79 billion that was due on June 9th, 2025 but ended up being paid on July 15th, 2025

· Kes 11.98 billion that was due on May 19th, 2025 but ended up being settled on July 15th, 2025

Finally got my paws on Gerschenkron’s Economic Backwardness—my dad’s 1965 edition, which retailed at $3.50.

Current lowest Amazon price is $145, which means annual inflation of 6%

In what circumstances can KRA deem all deposits into your bank account as income & therefore taxable?

The judgement on appeal E1116/2024 (Kirin Pipes Limited vs KRA Commissioner Intelligence Strategic Operations Investigations & Enforcement) before the Tax Appeals Tribunal is one I think every Kenyan needs to read.

The Big Issue:

· The issue at hand is a crucial one - In what instances can KRA deem all deposits into a bank account as income & therefore taxable?

The Contention:

· KRA conducted an investigation into Kirin Pipes Limited's tax affairs for the period 2019 - 2022 & issued assessments for income tax of Kes 34,300,288 & VAT of Kes 22,687,105

· Kirin Pipes Limited went before the Tribunal arguing that KRA made an error by assuming that every deposit made into its bank accounts amounted to income capable of being charged tax

Kirin Pipes Limited's argument:

· The company commenced its operations in 2019 during which shareholders injected share capital. The ordinary share capital was Kes 10.0 Million but the company required further capital & therefore shareholders deposited a further Kes 29,425,495.45 into its bank account

· The company therefore argues that the deposit of Kes 29,425,495.45 was not income but capital injection

· During its formative years, the company required funds to help cover the initial setup costs & operating expenses & sought for a Kes 31,697.392 loan from Nanchang Municipal Engineering Development

· The company therefore argues that this deposit ought not be subjected to income tax by KRA since it was a loan

· The company also argued that it received funds from its shareholders totalling Kes 24,619,662 to fund its operations & that the said amounts were not income but shareholders deposits

The Verdict:

· The Tax Appeals Tribunal held that Kirin Pipes Limited failed to provide an analysis of the specific deposits which related to capital injections & to link the deposits to the shareholders who are indicated in the Official Company Search (form CR12).

· The Tribunal observed that Kirin Pipes Limited provided uncertified bank statements & swift confirmation slips which could not be attributed to capital deposits in the absence of other corroborative documents such as an analysis & description of the deposits, Meeting Minutes/ Resolutions or any other document to demonstrated that indeed the amounts in question were capital injections

· The Tribunal held that it was incumbent upon Kirin Pipes Limited to demonstrate the flow of capital from its shareholders & how the same was eventually accounted for by the company

· The Tribunal also held that Kirin Pipes Limited failed to provide evidence of the resultant shareholding structure after deposits by the said shareholders. Whereas Kirin Pipes Limited submitted form CR12, it only showed the initial capital of Kes 10.0 Million

· Tribunal found that Kirin Pipes Limited failed to prove that deposits worth Kes 54,045,101.45 in its bank accounts during the period under review were attributable to capital injection from its shareholders

· The Tribunal established that whereas Kirin Pipes Limited argued that a deposit worth Kes 31,697,392 was a loan from Nanchang Municipal Development Corporation, the documents indicated that it was interest free & the same could be repaid at any time at the discretion of Kirin Pipes Limited

· The Tribunal held that such open terms in the loan agreement made it difficult to verify whether the amount was indeed a loan, given that there was no interest charged & neither was there a repayment period

· Tribunal also pointed out that from the date the loan agreement was signed in 2019 to the date of assessments in 2024, Kirin Pipes Limited did not provide proof of any repayments it made towards the said facility

· The Tribunal therefore found that the documents tabled by Kirin Pipes Limited to support its claim that Kes 31,697,392.00 of the deposits in its accounts were proceeds of a loan advanced were insufficient & did not meet the evidential threshold of disproving that the loan was income chargeable to tax

· In sum the Tribunal found that KRA did not err in treading all deposits into Kirin Pipes Limited's bank account as income & therefore taxable

My key take aways from the meeting between President William Ruto & the Kenya Private Sector Alliance (@KEPSA_KENYA) this morning.

A 🧵

· We should expect to see a Business Laws (Amendment) Bill 2025 further down the road in 2025

· The President says he has directed the Ministry of Investments, Trade & Industry to table the Bill before the Cabinet by close of August 2025

· The President says the Bill will address issues that were not addressed via Finance Act 2025

Musings:

· It looks like the path (post-Finance Bill 2024) Kenya Kwanza has chosen is for staggered amendments (i.e. some come in via Finance Act IN Q2 then the second tranche comes in via Tax/Business Laws Amendments in Q4)

· This also played out last year with the Tax Laws & Business Laws (Amendment) Acts that kicked in on Dec 27th

· I wonder what issues the Business Laws (Amendment) Bill 2025 will be focusing on though?

The Auditor General's Special Report on Government Digital Payments Platform (eCitizen) is out!

Some heavy revelations here including the unearthing of diversion of funds from the mandatory 222222 Paybill for payment of government services to private accounts & the irregular collection of Convenience Fees totalling Kes 1.807 billion

A 🧵

We've done a deeper analysis on NSSF contributions and beyond for those who haven't fully understood the changes that took effect on Feb 1, 2025, and continuing into 2026.

This includes how payslips will look after deductions

Read & Save the thread below;

In the FY2024 Saccos' earnings season, the usual hype around dividends has been obscured by exposure to KUSCCO which has slumped into insolvency.

I sat down with the CEO of the regulator of primary Saccos (SASRA), Peter Njuguna, to discuss just how much havoc the KUSCCO insolvency has wreaked.

A🧵

We began from the prudential side of things:

· The total KUSCCO exposure to Sasra regulated 355 Saccos is Kes 14.6 billion

· This Kes 14.6 billion translates to just about 10.0% of the industry core capital (2023 industry data)

· Out of 355 Sasra regulated Saccos, 201 (56.62% of the total universe) are exposed to KUSCCO

Mhasibu Sacco takes a Kes 480.6 million hit on account of KUSCCO.

The Sacco indicates that the amount related to a fixed deposit held at KUSCCO & matured on Jan 16th, 2024 but KUSCCO was unable to honour the withdrawal request.

This dividend/AGM season all members must seek visibility on their Sacco's exposure to KUSCCO.

Two days after raising the issue of the Draft 2025 Budget Policy Statement, the National Treasury finally uploads it.

First, I see an issue here. The public has until Jan 21st, 2025 to make submissions on the document.

That's just 6 days to interact with the document & make submissions.

So what's new?

A short 🧵

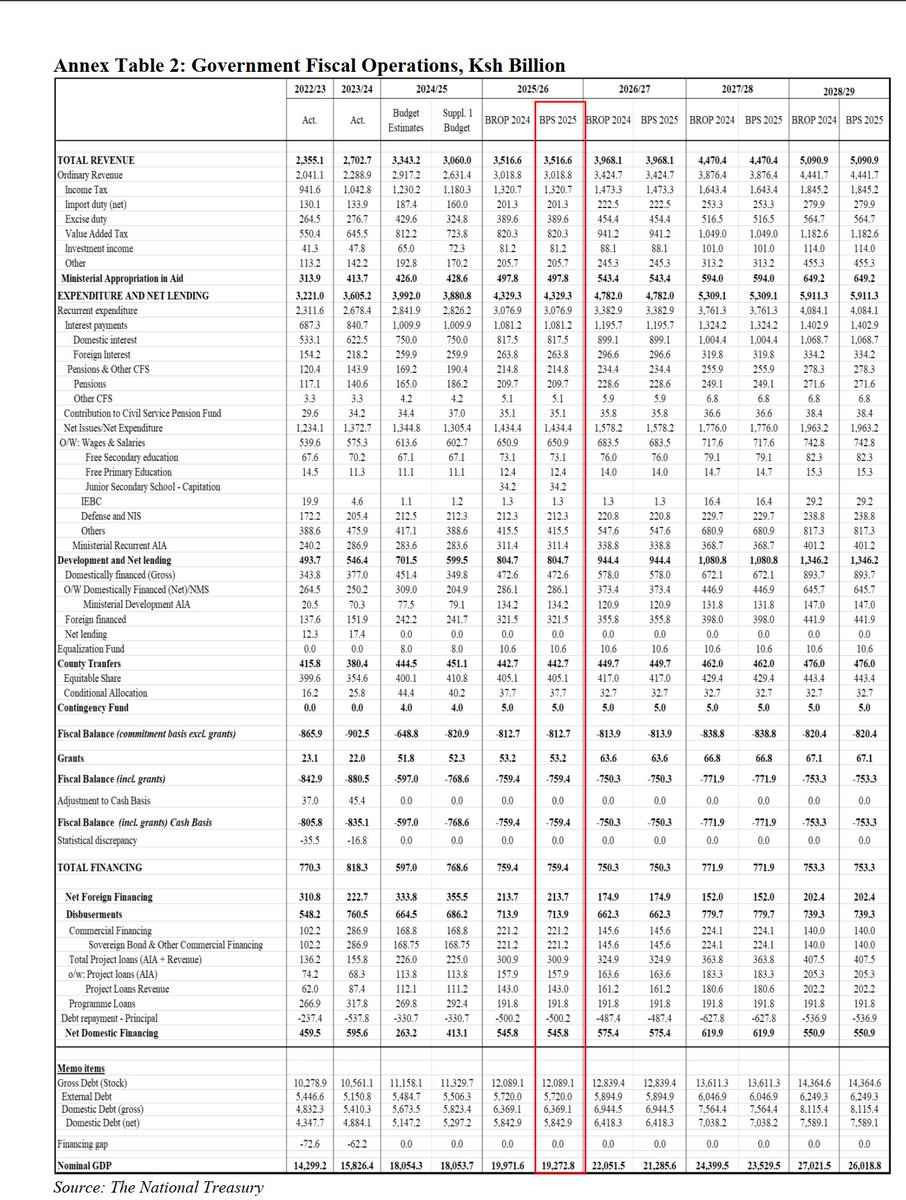

Kenya's FY 25/26 Budget Highlights (BPS):

Total Expenditures ofKES 4.329T composed of:

—📈 Recurrent spending: KES 3.077T.

—📊 Development spending: KES 804.7B.

—🏛️ Transfers to counties: KES 442.7B

Total revenues of KES 3.517T composed of:

—💸 Ordinary: KES 3.019T (Tax: KES 2.732T)

—📈 Appropriations in Aid: KES 497.8B

Fiscal deficit of KES 759.4B to be financed by:

—🌍 External borrowing: KES 213.7B

—🏦 Domestic borrowing: KES 545.8B

Summary of notable changes being proposed:

· Confusion on higher excise duty on air time & internet is here to stay. On one hand, Committee endorses the proposed increase, on the other hand it seems to reject it

· The Committee recommends that Significant Economic Presence Tax only applies to businesses whose annual turnover >Kes5.0M

· The Committee is recommending the dropping of the proposed imposition of excise duty on imported pasta (Spaghetti, Noodles, Macaroni)

· Committee recommends that 5.0% withholding tax on infrastructure bonds be dropped

· The Committee has rejected proposals to explicitly have Affordable Housing Contribution as an allowable deduction applying to all incomes. They say the Affordable Housing Act addressed this

· The Committee has rejected proposals to retain Railway Development Levy at 1.5%. However, it proposes a lower rate of 2.0% as opposed to the Bill's proposed 2.5%

· The Committee has endorsed a proposal to introduce Withholding Tax at a rate of 1.5% of gross as a final tax for the sale of scrap

· Excise on imported glass bottles is switching from purely ad valorem to a hybrid of ad valorem & specific at US$160/tonne. Total chaos here

· Multinationals take note , Minimum Top Up Tax at 15.0% is here to stay following endorsement by the Committee

· Excise duty on betting is shooting up to 15.0%. Quite an unpredictable environment here given the Finance Act '23 changes

· Family trusts have been granted reprieve. Committee recommends a halt on the proposed rationalisation of exemptions from tax

· Park entry fees et al have been spared the rationalisation of the 1st Schedule of the VAT Act

· Imported ceramics, sinks & wash basins have been spared the proposed introduction of excise

· Animal feeds have been spared the migration from zero-rating to exempt status on VAT

Day 4 of Phase 2 of public participation on the Tax Laws (Amendment) Bill 2024 & Tax Procedures (Amendment) Bill 2024 took place yesterday.

Here's a summary of some of the key issues that emerged during yesterday's submissions.

A quick 🧵

Day 1 of Phase 2 of public participation on the Tax Laws (Amendment) Bill 2024 & Tax Procedures (Amendment) Bill 2024 kicked off.

Some issues that stood out for me from the submissions made so far.

A quick 🧵

Day 2 of Phase 2 of public participation on the Tax Laws (Amendment) Bill 2024 & Tax Procedures (Amendment) Bill 2024 took place yesterday.

Here's a summary of some of the key issues that emerged during yesterday's submissions.

A quick 🧵

Safaricom HY2025 earnings.

By & large, strong momentum at the top:

· Group Service Revenue: 14.0% up y/y to Kes 181.4 billion

· Ethiopia contributing 10.0% of the growth of the group service revenue

· Safaricom Kenya Service Revenue: Kes 177.5 billion, up 12.9% y/y

· Safaricom Kenya free cashflow: Kes 80.6 billion, up 41.4%

· Total transaction value on MPesa rose 10.8% y/y to Kes 20.84 trillion

A 🧵

Away from the impeachment & term limits, Sessional Paper No.4/2024 - Government Transport Policy, is out in Draft form.

I haven't seen an invitation for the public to submit comments but I suppose that will be coming any time now.

Considering how much the tax payer shoulders in financing government transport, this is an important document.

Key highlights, a🧵