How do you think TradFi entrants into the crypto options market would affect the market? How do you think it would affect DeFi options protocols? (4/4)

#Crypto#DOVs#CryptoOptions#Volhalla#Volatility

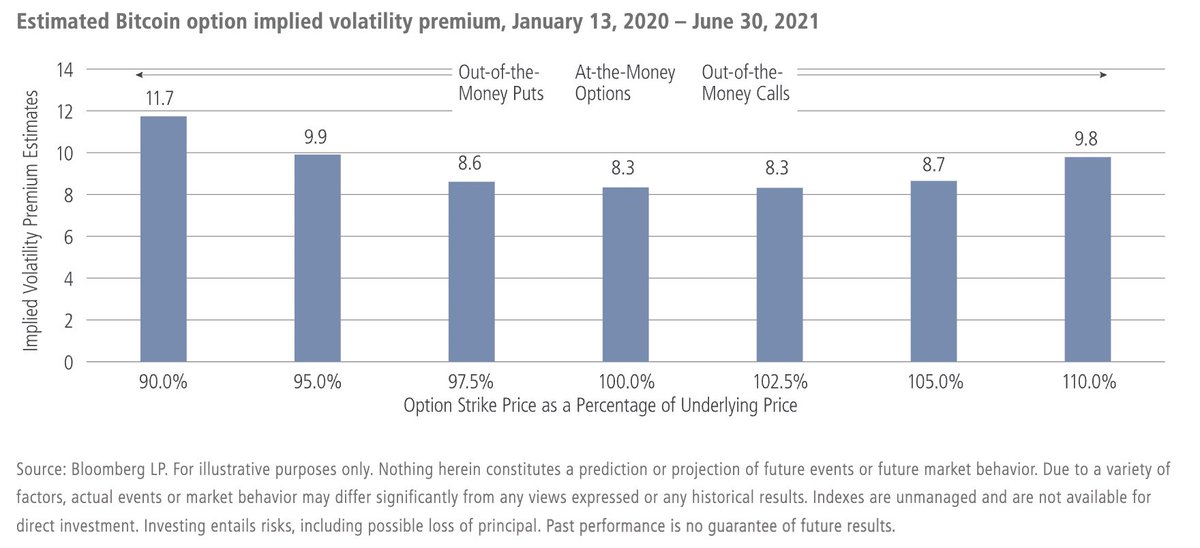

Sunday reading: Neuberger Berman, $460bn AUM asset manager, describing how a strategy of systematic selling BTC options can provide “rare, new and unique implied volatility premium”.

https://t.co/bo8bmh7MS4

DOVs give everyone the ability to harvest this vol premium!

(1/4)

As BTC gets more institutionalized the demand for protection via put buying may increase. This is one reason for the higher vol premium in BTC puts. They write that “digital assets, led by Bitcoin, could provide a rich source of uncorrelated premiums for years to come.” (3/4)

1/ Butterfly Spreads 🦋

In the natural world, a butterfly is a spineless four-winged insect with a strong thorax.

A butterfly spread, however, is a risk-reward defined directionally neutral options strategy.

🧵���️

@0xBirds Capital efficiency definitely a wider problem that the DeFi options community needs to figure out, but we have ideas on how to minimize collateral requirements via limited loss formats of common spreads and multi leg structures. More to come stay tuned!

Is selling crypto options for yield an attractive strategy?

With the rapid growth of DeFi Option Vaults (DOVs), you may be wondering whether this is an attractive risk-reward strategy to generate income. A thread (1/9)

@mihai673@0xBirds DOV auctions have been fair based on comparisons to Deribit pricing at the time of trade. But we do agree that having all auctions on a day like Friday results in probably suboptimal pricing. We have ideas on how to make this more efficient. Will have more to share 👀

@mihai673@0xBirds 3) The option need not end up in the money for a market maker to make money. They can recycle the risk to another buyer. They can also trade the gamma and potentially recoup more than the premium even if the option ends up out of the money.

@mihai673@0xBirds 2) The market has various views on risk premium itself. It’s hard to value the VRP and depending on your view and wider mkt conditions you can have diff conclusions on what the VRP is. This is a great podcast that describes this phenomenon https://t.co/drS7ukJse3

@mihai673@0xBirds Great qn! I wouldn’t say that option buying is a negative expected value pursuit. 1) not all market participants have the same risk preferences, which results in differing levels of demand for options. A miner who is hedging has a diff willingness to pay vs a hedge fund.

DOVs make this easy but not all vol selling strategies are created equal. Stay tuned to hear more about how Volhalla will offer the next generation of volatility selling strategies via strangles, spreads, and exotics.

Please retweet if you found this thread helpful.

(9/9)