Mon AM: the framework (Computational vs Physical Bottleneck).

Tue AM: three vectors named in three hyperscaler 10-Ks.

Tue PM: the single best primary-disclosure signal to track Vector 1 (ASIC substitution) as it plays out → AVGO custom silicon mix-of-revenue. 🧵

BofA/Hartnett’s "Flow Show" is clear: the 2026 playbook is defined by the 3 Cs—Conflict, Climate, and Commerce. While the S&P 500 tests highs, the real story is a barbell shift into cash ($56bn inflow) and Tech ($22bn inflow) over the last two weeks.

Yield in digital assets is transitioning from protocol-manufactured subsidies to service-based outcomes. The baseline shift for allocators is moving away from seeing capital as a loan and toward seeing it as a functional utility providing market-making and liquidity services.

The "next billion users" were never coming through today's wallets and DeFi apps.

They’re coming through systems they already use.

Tokenized rails embedded into banks, exchanges, and platforms scale faster than anything crypto-native has built so far.

Enterprise > Cypherpunk

JP Morgan just dropped a massive strategy note arguing for another V-shaped market recovery. While the geopolitical situation remains incredibly volatile they are explicitly telling allocators to use this weakness to buy the dip.

Hyperliquid just reached full on chain parity with Binance. Trade sizes up to one million dollars show identical nine to ten basis point slippage on BTC. While legacy DEXs break down at size especially on SOL Hyperliquid stays completely flat. Heavy lies the crown.

The inflation narrative is overwhelming the soft landing consensus. The divergence between physical commodities and forward equity multiples is massive. The market is pricing in pure perfection.

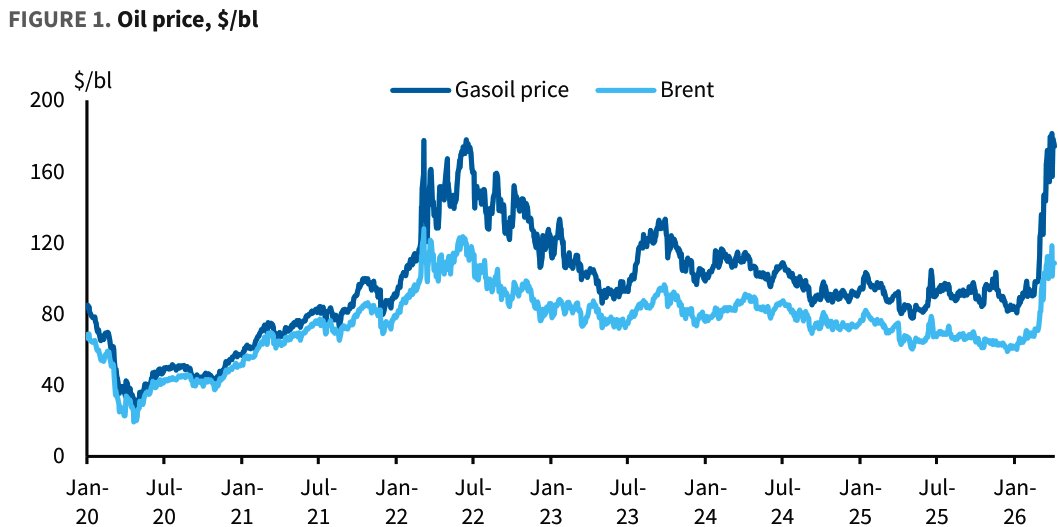

The headline crude price is completely hiding the real crisis. Diesel just breached $170/barrel. Refined products are facing a much more severe supply shock than crude. If the Strait remains closed the market will break within a month.

We are officially entering the cognitive layer of finance. The fintech platform @Worth_AI just closed a $30M Series A led by Fulcrum Equity Partners and Amex Ventures. They are building something that will define the next decade of capital markets.

There is a lot of noise around the Clarity Act and stablecoins. The primary concern is that idle balances will not be allowed to accrue interest in a straightforward way. Many frame this as a severe structural limitation, but that is... simply not the case.

The Basel III "Endgame" pivot on March 19 quietly reduced capital requirements for big U.S. banks. That is effectively more balance sheet "dry powder" after years of ratcheting standards higher. On its face, it is about easing pressure on lending and market making.

Mastercard is acquiring BVNK for up to $1.8B.

This is one of the clearest signals yet that stablecoins are moving into core payments infrastructure.

Not adjacent. Not experimental.

This is integration into the global system.

For years, institutional crypto conversations were about permission.

Can banks custody it?

Will regulators allow it?

How should it be accounted for?

Those questions dominated the last cycle.

The conversation has now shifted.

From permission → execution.

A few observations 🧵

Goldman’s Rich Privorotsky with the line of the week:

“The US is fighting a kinetic battle in Iran. Iran is at war with the SPX.”

Oil is the transmission channel.

Energy shocks tighten financial conditions and hit equities first.

Politicians want to keep their jobs.

Crypto spent years experimenting with governance and token-first structures. Some of that experimentation was necessary.

Buuut, if the goal is to build durable businesses that _compete_ with banks and fintechs, the structure has to support that.