FANNIE MAE/FREDDIE MAC fair market ADVOCATE. Don't tell me O had no scandals, if I go off on you, you definitely earned it. I Follow back MAGA patriots.

@Rainmaker1973 Please put your seats up, and your trays in the upright and locked positions. Keep arms hands and extremities inside the vehicle at all times and do not exit until the vehicle has come to a complete stop.

The math on Fannie and Freddie is so dislocated it looks like a pricing error.

Fannie printed $14.4 billion in net income last year. Freddie printed $10.7 billion. Combined market cap on the pink sheets right now: ~$12 billion. The market is pricing $25 billion in annual earnings at a 0.48x multiple. Find me another 0.48x earnings multiple anywhere in American finance. It doesn't exist.

The dilution fear is the reason the stock is cheap and the reason the stock is wrong. Treasury put in $187 billion. The GSEs have swept back over $300 billion since 2012. That's an 11.6% IRR. If Treasury exercises its 79.9% warrants at today's price, the government's stake is worth ~$9.6 billion. If it exercises post-relist at 10x earnings, that stake is worth $200 billion. The difference is $190 billion. Washington doesn't leave $190 billion on the table to spite penny stock holders.

Capital requirements look scary until you do the arithmetic. The ERCF says $334 billion. They have $179 billion. The FHFA can lower Tier 1 to 2.5% without Congress. New target: ~$190 billion. Gap: $11 billion. One IPO closes it. One year of retained earnings closes it twice.

G-fees are already at 65 bps. Pre-crisis they were 20. The GSEs have been charging privatized pricing inside a conservatorship for 14 years. Credit losses outside of 2008 average under 5 bps. The margin is so fat that mortgage rates don't move at all on release.

So what are you actually buying at $5? A royalty on the American mortgage system. 65 bps on $7.5 trillion in outstanding MBS. $48 billion in gross annual revenue. Under 5 bps in historical losses. The most predictable spread in finance, backstopped by a guarantee both parties have publicly committed to preserving.

JPMorgan trades at 13x and takes real credit risk. Utilities trade at 15x with half the visibility. These two trade at 0.48x collecting tolls on other people's risk.

The second those warrants convert and the NYSE listing goes live, every index fund and pension fund with a financial sector mandate has to buy. Two of the ten most profitable companies in America, sitting on the pink sheets, waiting for one signature.

$fnma this is such bull shit ... they can provide 200b to lower interest rates, they can now accept crypto which is crazy ... but they can't trade on NYSE? Has this administration done anything or took any actual step that helps shareholders besides trumps 2 tweets months ago?

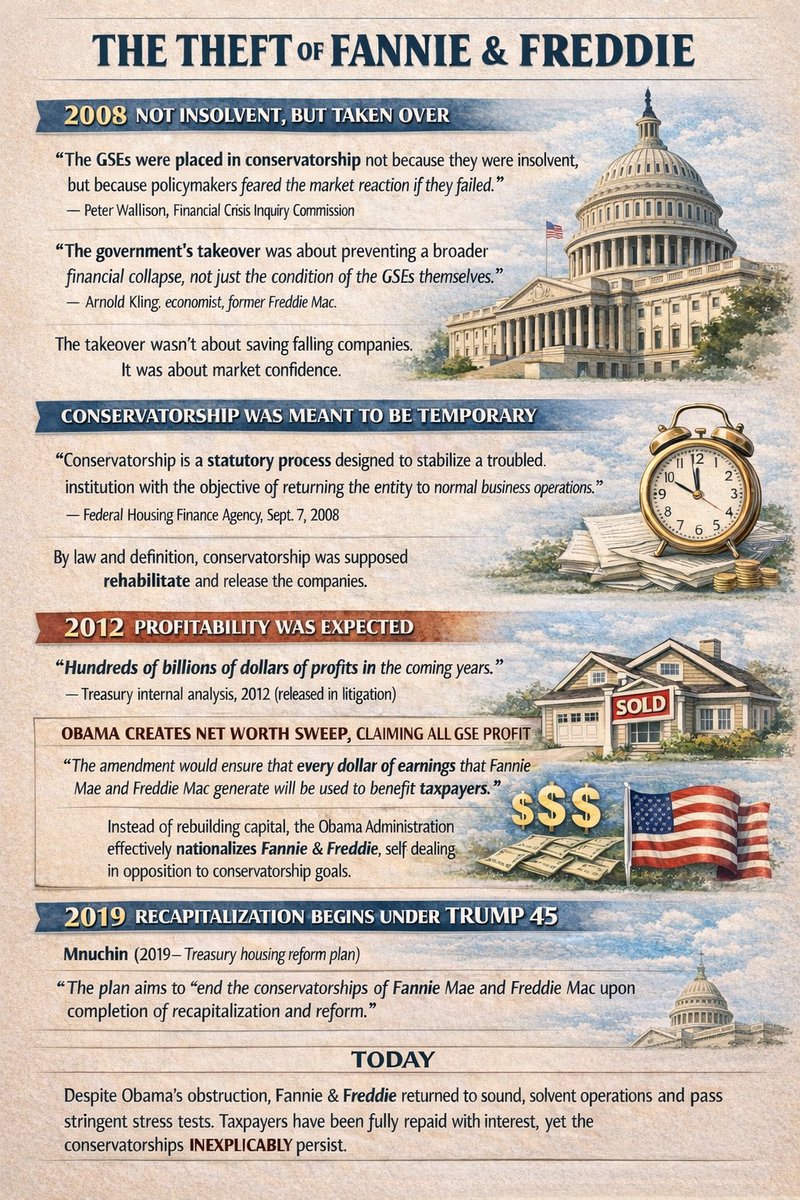

For the financially illiterate… $FNMA & $FMCC were placed in conservatorship to get them sound & solvent. They repaid their bailout and more. Once they started making big money, Obama changed the terms and stole the profits. F&F shareholders just want their property back.

If bartenders can go to jail for over-serving alcohol to someone who then kills another person, judges should go to jail for releasing criminals who do the same.

As a long-time shareholder in Fannie Mae $FNMA, I want to thank Mr. Ackman for his perseverance and activism on behalf of shareholders. I have been in this investment for nearly two decades and, as an individual shareholder, in 2013 I met with lawmakers in Washington, D.C. to discuss my individual shareholder perspective as part of a group named Shareholders United.

The facts and circumstances of this seemingly endless conservatorship are so bizarre and unnecessarily complicated that they do not lend themselves easily to the common everyday social media post and, as informative and comprehensive as Mr. Ackman’s piece is there is much, much more to say on the matter.

While this is no longer the headline story, for much of the conservatorship, at least politically, F2 (Fannie Mae & Freddie Mac) was considered to be Villain #1 in Great Financial Crisis – ostensibly, the cause for the 2008 near collapse of the global financial system. Nothing, nothing could be further from the truth. Without misguided financial deregulation, derivative instruments run amok, a great deal of malfeasance in banking institutions, the derivatives industry, and ratings agencies, and almost nonexistent regulatory oversight of said entities there would have been NO GREAT FINANCIAL CRISIS – but more on this later in the piece.

Essentially, from the earliest stages of the government response to the crisis, the American public was bamboozled with the F2 villain narrative by a tightknit group of political and financial ne’er-do-wells, which has been the basis for the mistreatment Mr. Ackman so adroitly and comprehensively lays out. This is the part of the story that I would like to tell and, for all intents and purposes, negates any defensible reason F2’s captors have for said mistreatment (especially with regard to shareholders) and the continued conservatorship.

First, allow me to add some startling figures to Mr. Ackman’s accounting. Since the conservatorship began F2 have earned, and shareholders have been deprived of, nearly $500B in profits that have gone directly (via the net worth sweep) or indirectly (establishment of the government “liquidation preference”) to the government, in addition to not receiving credit for tens of billions of dollars (more likely upwards of $100B) in fraudulent or bad mortgage loans the banking system off-loaded on F2, on top of spending billions of shareholder funds in establishing what began as the common securitization platform and what is now U.S. Financial Technology (U.S. Fintech: https://t.co/wrAAy52XeV) - a fully-fledged company ready for spin-off (of which current shareholders should rightly own a piece).

All told, this is somewhere in the ball park of $750B lost to shareholders. (Notes: ~$300B returned directly to U.S. Treasury via the net worth sweep; ~$170B “retained” by F2 since the net worth sweep as of Q4 2025, but according to F2’s Q4 2025 financial statements still subject to U.S. Treasury ownership due to the establishment of the “Liquidation Preference”; FHFA settled with large banking institutions long ago for the bad mortgage loans off-loaded to F2 at hugely discounted values, and lumped in the settlement with LIBOR lawsuits settlements while F2 never received credit for those settlements; and finally, I do not know of any independent valuation of U.S. Fintech – but surely this entity provides a great deal of value that rightly belongs to shareholders.)

Now, on to the meat of the matter. The Great Financial Crisis fire, metaphorically speaking, started in the basement of the house with the home mortgage loan, more correctly subprime mortgage loans, and the repackaging of millions of those loans into mortgage-backed securities (MBS), the long-standing F2 staple line of business which was so deceptively manufactured, by politicians, regulators, the financial establishment and the media into the big lie that F2 was the villain of the crisis. (Note: private banking institutions also engage in the repackaging of these loans into what are known as private label mortgage-backed securities – PLMBS). F2 was a politically convenient scapegoat and a readily available piggybank which effectively diverted attention away from and funded the bailout of the true causes of the conflagration that engulfed the entire financial system: financial deregulation, the subprime loan industry, derivatives, ratings agencies, and almost nonexistent regulatory oversight of these elements.

This was the era of the NINJA loan – no income, no job, no assets – these “subprime” loans became the crisis fire kindling and, mixing metaphors here, the virus that infected mortgage-backed securities investments. But here is the relevant crux of the matter, every single one of these subprime loans were made by banking institutions, mortgage companies, or other entities which originate mortgage loans, NOT F2, Fannie Mae and Freddie Mac, do not and never have originated mortgage loans. In as much as they engaged in the repackaging of these loans into their agency mortgage-backed securities let us not forget the fraudulent banking institution loans that were offloaded on F2, but more importantly, the fact that PLMBS failed at more than five times the rate of F2 agency MBS.

But the story gets even uglier for the original political-financial establishment faux F2 villain narrative. If subprime loans and the associated MBS would have been the only game in town, good proactive regulatory oversight should have caught this long before any significant problems could have arisen and even allowing for genuine regulatory missteps or allowances for well-intentioned government homeownership policies, the fire should and could have easily been contained to a manageable neighborhood of the financial sector. Enter financial industry deregulation, institutional malfeasance, and the Great Financial Crisis uranium fission material – the derivative.

Although each of these pieces cannot be done justice in a piece of this length, already too long for most, the long and short of it absolving F2 of any semblance of culpability played out along the following lines:

An entire subprime mortgage loan industry arose around well-intentioned government home ownership policies and expanded well-beyond all reasonable or financially prudent application (NINJA loans) due to what can at best be described as lackadaisical regulatory oversight. Investment banking institutions created pipelines directly from both legitimate banking institutions originating mortgage loans and fly-by-night mortgage companies (Countrywide Mortgage, anyone?) to earn tens of billions, if not hundreds of billions in profit by assembly line packaging of these loans into PLMBS and other derivative instruments for resale to investors world-wide. All while the ratings agencies blessed these instruments with AAA (triple-A) ratings. You can look up those still existing ratings agencies; I will not name them here, but they are well-known, and they are notorious for their actions and culpability for the 2008 crisis.

(Note: one, now defunct investment bank alone, in one year, did tens of billions of this business through a derivative security known as the CDOs (collateralized debt obligations). Multiply this activity by dozens of large global investment banking institutions and the thousands of legitimate banking institution mortgage loan originators (plus a handful illegitimate fly-by-night mortgage loan companies) and you have a true global crisis in the making.

But the nuclear chain reaction, that 2008 mushroom cloud, was ignited by supposedly respectable investment banking firms and other financial institutions lying to their clients, to each other, and to investors about the true depth and breadth of their exposure, their knowledge and culpability in these arrangements, and then creating derivative instruments (namely the credit default swap) to game the financial system, shareholders, counter party institutions and the government (for undeserved, but necessary bailouts). The notional value of these credit default swaps alone was 60-70 TRILLION DOLLARS! This was more than 4 times the 2008 U.S. GDP, and anywhere from 12 to 15 times the entire combined 2008 F2 mortgage credit books! Throw in some shoddy financial deregulation interconnecting the worst aspects of each industry segment’s profit seeking motives, hundreds of billions in profits to protect, and asleep at the wheel regulatory oversight agencies, and voila – you have the Doomsday Machine – the true reason the financial system nearly collapsed.

Now, look me in the eye and tell me with a straight face F2 was the cause of or significantly contributed to the financial system collapse. I can elaborate much further on each aspect outline in this piece; however, it is long enough already and should raise the ire of even the most casual observer. But let me finish by addressing the current administration.

As of now, the Trump administration bears no culpability for any aspect of the Great Financial Crisis. I voted for President Trump three times and believe he will be one of the most consequential pro-American, pro-business presidents in our country’s 250 year-young eminence. As far F2 is concerned, I viewed President Trump, Secretary Bessent, and Director Pulte as the Dream Team, and had the hopefully, not misplaced confidence, they would research, learn and fully understand this conservatorship’s true history, and have the fortitude, power, and sagacity to put things right for shareholders, conservatorship, and constitutional law (5th amendment Takings Clause). My suspicion is that special interests and inside financial establishment players are or have been hamstringing the Dream Team.

President Bush allowed then Treasury Secretary Hank Paulson to favor his Wall Street cronies by putting F2 in conservatorship and swiping their capital.

“We’re going to move quickly and take them by surprise. The first sound they’ll hear is their heads hitting the floor.” --- Hank Paulson, from his 2010 memoir On the Brink: Inside the Race to Stop the Collapse of the Global Financial System

President Obama instituted the net worth sweep – taking F2’s entire annual profits into the U.S. Treasury, and President Biden slept through his entire presidency.

Time is running out and all eyes are on President Trump, our distinguished Treasury Secretary Bessent, and the ever-Trump loyal and competent FHFA commander Director Pulte to rise above and distinguish themselves from the past bad actors and administrations. F2 was not culpable for the financial crisis, in fact, their seizure and 20-year flow of hundreds of billions of dollars into the U.S. Treasury (fungibility of money anyone?) was a significant factor into alleviating the distress of the wider financial institutional banking system via U.S. Treasury bailouts. Finally, U.S. Constitutional Law (5thAmendment Takings Clause) and long-standing shareholder rights laws rightly demand that investors fully share in, at worst, a minimally diluted value of the hundreds of billions these companies have earned and would have properly shared with investors as freely operating, publicly owned companies.

$FNMA $FMCC @BillAckman@michaeljburry@pulte@SecScottBessent@POTUS@FHFA

A number of press reports have characterized our and other shareholders’ efforts on behalf of Fannie and Freddie (F2) as seeking a ‘gift’ or ‘handout’ from the government. We, the shareholders of F2, seek no such thing.

Hundreds of financial institutions were bailed out during the GFC by the U.S. Treasury. Nearly all of the financial institution bailouts during the GFC involved an injection of capital in the form of senior preferred stock by Treasury at an interest rate of 5%, plus warrants to acquire common stock in an amount equal to 15% of the face amount of the preferred with an exercise price at the then-current stock price of the rescued institution.

For example, Treasury’s preferred stock investment in Goldman Sachs was in an amount of $10 billion and, in addition, Treasury received warrants on $1.5 billion of GS' common stock at its then market price.

The bailout terms for F2 were materially more burdensome and expensive, with a higher interest rate and substantially more warrant coverage, than that of every other financial institution (other than those of AIG whose terms were similar). Despite the F2 bailouts’ massively more burdensome terms, shareholders are not complaining about the original terms.

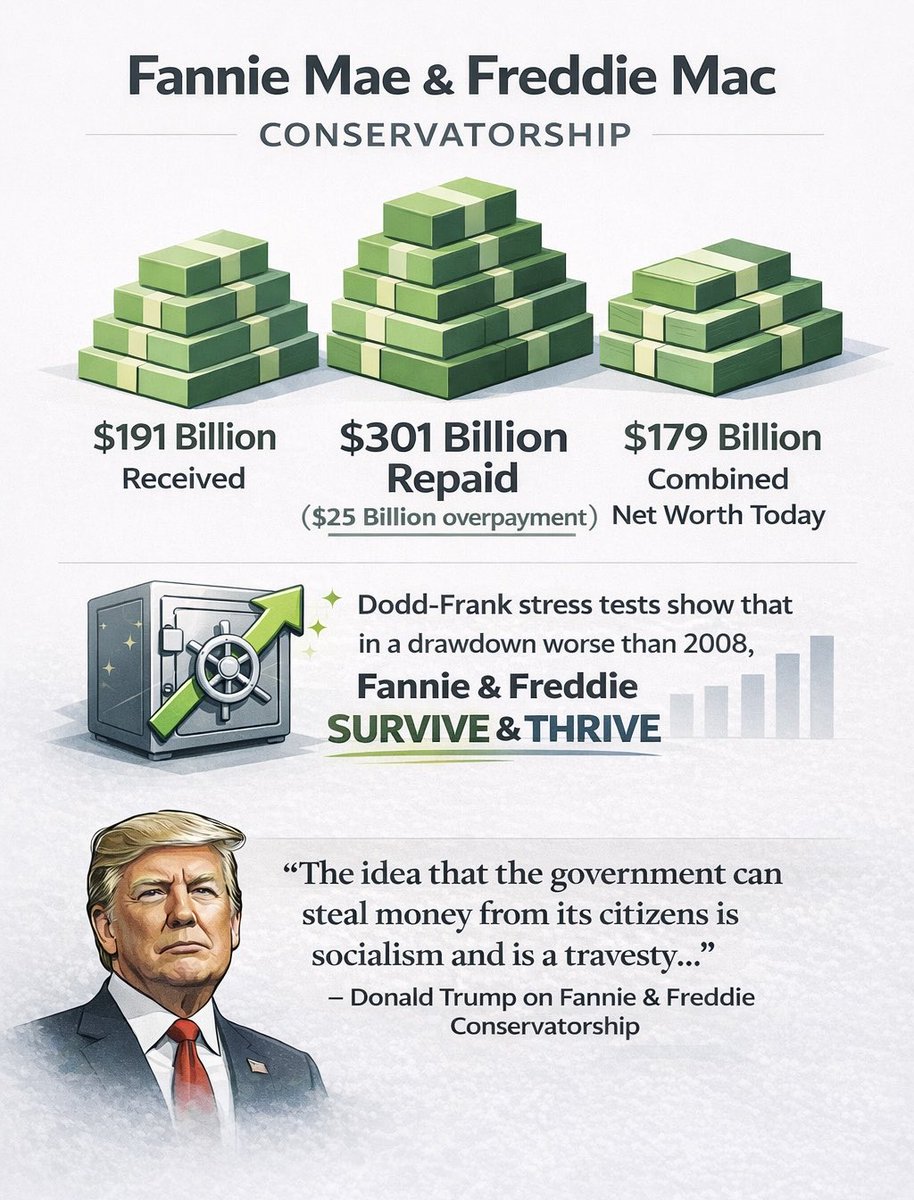

Treasury invested $193 billion in F2 in the form of senior preferred stock (SPS), including funding for $2 billion of commitment fees, with a 10% coupon (twice that of the banks). Treasury also received warrants on 79.9% of both companies’ outstanding shares.

Fannie and Freddie have since repaid Treasury $301 billion, which includes interest on the SPS at a blended rate of 11.6%, an interest rate which is 160 basis points more per annum, and have returned the entire $193 billion of outstanding principal, $25 billion in excess of what was contractually owed. In summary, the F2 SPS has been fully repaid according to its original contractual terms plus an extra $25 billion.

Despite the fact that the SPS has been more than repaid in full, Fannie and Freddie have not accounted for these payments on their respective balance sheets, and the $193 billion of SPS remains an outstanding liability as if no principal payments had ever been made.

How can it be, you might ask, if indeed F2 have repaid $301 billion to Treasury when only $276 billion was due could there be any remaining balance of the SPS on the F2 balance sheets?

The answer relates to something called the ‘Net Worth Sweep (NWS).’

During the second term of the Obama administration, on August 12, 2012, two quarters after F2 returned to profitability, Treasury announced that it was unilaterally amending the terms of the SPS stock to provide that Treasury would take 100% of the profits of F2 each quarter in lieu of the 10% annual dividend rate. This was not a negotiated resolution with F2. It was a unilateral amendment of the original terms of the SPS that was done in bad faith.

The supposed rationale for the amended terms of the SPS was akin to the IRS garnishing the wages of someone who will never be able to pay the taxes that they owe. That is, the Treasury said F2 will never be able to pay the 10% coupon, let alone the SPS’ $193 billion principal balance, so it decided instead to ‘settle’ for 100% of F2’s profits forever.

In discovery, shareholders learned that the stated justification for the amendment was false. In mid 2012, the Obama administration had come to learn that both companies would soon be reversing tens of billions of reserves on their balance sheets as housing values had increased and the reserves taken during the GFC had been excessive. The NWS was instituted by Obama to forestall F2 from forever being able to recapitalize and be released from conservatorship. The NWS was not a ‘settlement’ for a lesser amount of future payments. It was the outright theft of the forever profits of both companies.

Never before or since has the government ‘swept’ 100% of the profits of any company, let alone a financial institution in conservatorship, a form of government intervention where the goal is rehabilitation of the institution, and where the hierarchy of corporate claims has always been respected.

The accounting for the NWS payments while it was in effect (until Secretary Mnuchin terminated the NWS in Trump’s first term) was also unusual. The NWS was treated by F2 as a quarterly adjustment to the dividend rate on the SPS such that the dividend amount owed was made equal to the after-tax profits of F2 for that quarter with no limitation.

In other words, regardless of the amount of profit F2 generated for the quarter – whether or not it was in excess of the original 10% annual dividend – the dividend payable under the NWS was made equal to the quarterly profit. The absurd terms of the NWS sweep therefore made it impossible for any partial or full repayment of the SPS to take place as every dollar paid to the Treasury on the amended terms of the SPS was considered a dividend payment, even if the amount was massively in excess of the original contractual SPS terms.

The absurdity of the NWS was made clear just two quarters after the NWS went into effect. Fannie Mae generated a profit of $59 billion in the first quarter of 2013, and the SPS dividend rate for that quarter was set at $59 billion so the entire amount was swept to the government, more than 10 times the contractual dividend rate.

I had the opportunity to discuss F2 and the NWS with Warren Buffett about a decade ago and he said that he “couldn’t believe what the government had done.”

In short, the shareholders of F2 are simply asking the government to respect the original and highly burdensome terms of the SPS. There is no dispute that Treasury has received more than the original 10% coupon and full repayment of principal of the SPS, that is, an extra $25 billion.

We and the millions of other shareholders of F2 are simply asking the administration to honor the original SPS terms and properly account for the $301 billion of payments, thereby eliminating the SPS liability from both companies’ balance sheets.

Shareholders have not asked for the extra $25 billion to be returned to the two companies. Treasury can decide whether to keep those funds or return them to the companies.

Accounting for the repayment of the SPS has other important implications. Namely, it is critically important that conservatorships respect the rule of law, in particular, the contractual terms of corporate instruments and the hierarchy of claims. Otherwise, no financial institution that gets into trouble will be able to raise rescue capital in the private markets.

Notably, the treatment of F2 in conservatorship explains why Silicon Valley Bank and other recent large bank failures since the GFC were unable to raise private capital and avoid government intervention or a forced sale to J.P. Morgan. If the government with the stroke of a pen during conservatorship can at a whim wipe out common and preferred shareholders, no one is going to step in to try to save a financial institution that gets into trouble, and only the top few banks will be possible rescuers of big banks that fail.

Furthermore, because of F2’s history, their reputation in the capital markets has been greatly damaged. F2 raised $22 billion of preferred stock in the year or so prior to conservatorship as the government pressed both companies to raise capital. Institutions were willing to invest billions of dollars of capital into both institutions before they failed because, based on all precedent conservatorships, the contractual terms of all financial instruments and the hierarchy of claims had been preserved. Unfortunately, in light of the precedent of the net worth sweep, no investor can be confident that they won’t be wiped out in a future conservatorship so none has been willing to take the risk.

Some have proposed that Treasury simply convert the SPS into junior preferred and common stock and massively dilute shareholders. Putting aside the potential legal challenges to this approach, the result will be that Treasury will at best own something approaching 95% of both companies rather than 79.9%.

While the government’s percentage ownership stake would be larger in the SPS conversion approach, the value of the government’s larger stake would be considerably lower as the companies would become un-investable. Who would invest in F2 alongside the government when they just wiped out the previous owners?

In the SPS conversion scenario, the government’s stake, at best, if it could be sold, would trade at a massively discounted valuation, well below the value of the government's stake if Treasury retained only its contracted for 79.9% stake and respected the original terms of the SPS. In other words, a slightly smaller ownership stake of much more highly valued companies would equate to considerably more value for Treasury and taxpayers.

In a public letter to Rand Paul after his first term in November of 2021, President Trump recognized that the net worth sweep was theft from the shareholders of Fannie and Freddie. He wrote:

“Another Obama/Biden scam in legal trouble was when they allowed the Federal Housing Finance Agency (FHFA) to steal the retirement savings of hardworking Americans who had invested in Fannie Mae and Freddie Mac…The idea that the government can steal money from its citizens is socialism and is a travesty brought to you by the Obama/Biden administration. My Administration was denied the time it needed to fix this problem because of the unconstitutional restriction on firing Mel Watt. It has to come to an end and courts must protect our citizens.”

I couldn’t have said it better than President Trump.

Now that you have the time, Mr. President, let’s Stop the Steal!