Yes and even with this markets are pricing equities and credit for perfection, not caring about inflation pass throug, not caring about PMIs dropping, not caring about volatility to level ratio… I discuss those elements here if you want to understand more 👇 https://t.co/ZyHJebUU9x

@KobeissiLetter Funny to see markets so high and so tights despite decent probability for further escalation. FOMO and buy the dip mentality have been very impressive since COVID…

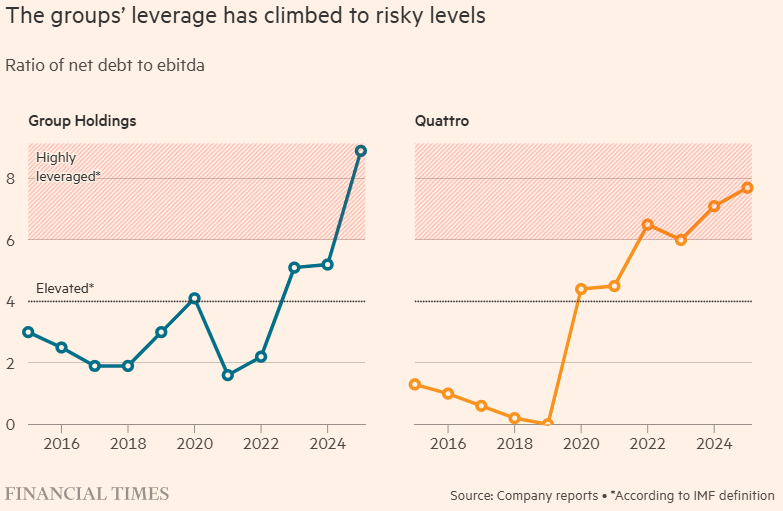

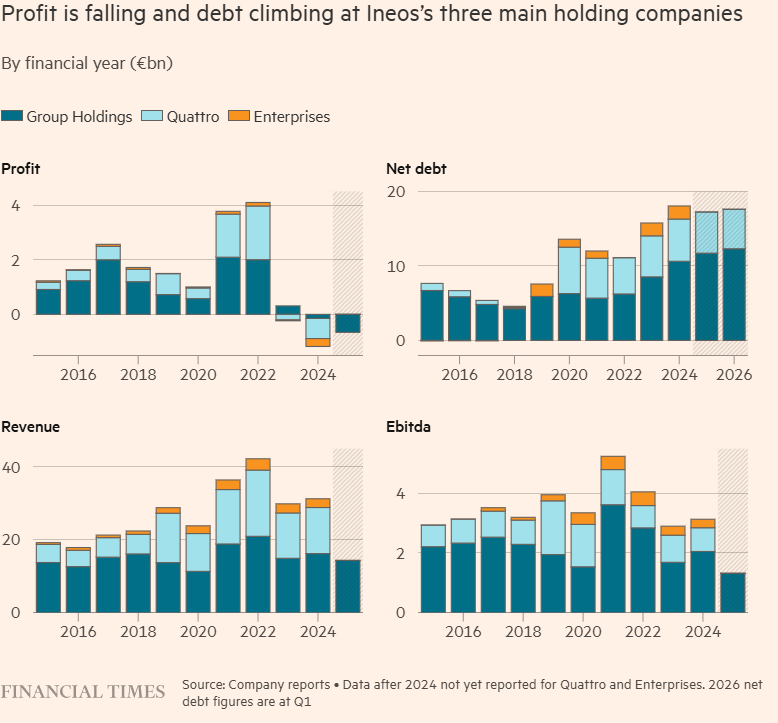

🔥 INEOS credit: hedge funds shorting it got SQUEEZED by the Middle East war — now investors are sharply divided on whether Ratcliffe's $19bn debt pile survives

The setup:

🔴 BOTH main divisions lossmaking — Group Holdings -€650mn, Quattro -€800mn in 2025

🔴 Leverage surging as debt nearly DOUBLED since 2021 (Project One capex)

🔴 €1.35bn maturities coming 2027 across both entities

🔴 Annual interest: €1.33bn combined

The reprieve:

✅ Group Holdings just refinanced €700mn OVERSUBSCRIBED last month

✅ Iran war disruption reversed capacity overhang — olefins/polymers prices surging in North America while feedstock stayed cheap

✅ Q1 2026: €421mn EBITDA + €400mn expected in April (war boost)

✅ Hedge fund shorts forced to unwind positions

The make-or-break bet: Project One €4.8bn Antwerp plant (Europe's first new cracker in 20+ years) completes end of 2026. Expected to add €700mn annual EBITDA from 2027. Designed to exploit US gas/EU chemicals price spread 💰

The problem child: Quattro can't access primary bond markets per multiple credit investors. Structurally cash flow negative, closing plants, selling assets. Has €2bn cash cushion (equity injection + inventory financing) but bleeding 🩸

Credit investors DIVIDED:

🐻 "Debt unsustainable, Quattro heading for restructuring"

🐂 "Scale and competitive edge will carry it through, Project One fixes the balance sheet"

💭 My View: This is a war-driven reprieve on borrowed time. The fact they got €700mn done oversubscribed is impressive, but both divisions are STILL lossmaking with €1.33bn annual interest expense. Project One better deliver that €700mn EBITDA boost in 2027 or Group Holdings joins Quattro in restructuring territory. The olefins price surge is 100% driven by Iran war supply disruption — when that fades, spreads compress and you're back to structural overcapacity in Europe competing with cheap Middle East/Asia supply. Quattro is toast without asset sales or a restructuring. The shorts got squeezed but the fundamental credit story hasn't changed.

Are you buying the war bounce or fading this as temporary?

📉 Credit spreads are just 16% of global IG corporate bond yields.

The lowest reading since July 2007 😱

The other 84%? Pure govies.

Meanwhile EUR IG just traded in a 4.5bp range over the past month — a decade low for realised vol 😎

Record supply. Record ECB QT. Primary NICs at March wides. Book covers at 2-year lows. Inflation picking up, PMI going down.

And secondary refuses to move 😅

My full weekly breakdown 👇

https://t.co/9OQp6RN99U

@unusual_whales They have a point but I think it’s a bit exaggerated ! I answer and discuss inflation, credit level, rates, earnings and more in my newsletter 👇

https://t.co/8NToFPpAcI

📉 Credit spreads are just 16% of global IG corporate bond yields.

The lowest reading since July 2007 😱

The other 84%? Pure govies.

Meanwhile EUR IG just traded in a 4.5bp range over the past month — a decade low for realised vol 😎

Record supply. Record ECB QT. Primary NICs at March wides. Book covers at 2-year lows. Inflation picking up, PMI going down.

And secondary refuses to move 😅

My full weekly breakdown 👇

https://t.co/9OQp6RN99U

OBR admitting they got 2022 wrong — while UK Sterling IG trades at ALL-TIME TIGHT vs rates vol 🤯

The credit playbook here isn't the spread, it's the curve:

-90bp of BoE hikes already priced

-UK 10y at decade highs

-Bund 2s10s flattening fast

In 2022, flat curves made deposits > IG bonds. Retail money fled credit. Technicals collapsed.

Speed of the curve flattening is the warning, not the level 🚨

Which BoE repricing scenario breaks the IG bid first?

👉 Follow me @ZeGoodTrader for more on Credit, Equities & Financial Markets

JPM says money is still entering Credit funds! 📈

Weekend 03 June flow check-in:

- 💶 Euro IG funds took in €624mm (+0.2% of AUM).

- 💷 Sterling IG funds were basically flat: +£12mm (~0% of AUM).

- 📈 European HY funds drew €296mm (+0.3% of AUM).

- 🧠 European strategic funds inched up €66mm (~0% of AUM).

📉 Credit spreads are just 16% of global IG corporate bond yields.

The lowest reading since July 2007 😱

The other 84%? Pure govies.

Meanwhile EUR IG just traded in a 4.5bp range over the past month — a decade low for realised vol 😎

Record supply. Record ECB QT. Primary NICs at March wides. Book covers at 2-year lows. Inflation picking up, PMI going down.

And secondary refuses to move 😅

My full weekly breakdown 👇

https://t.co/9OQp6RN99U

🏦 European bank bonds: AT1s leading with 2.2% excess returns YTD vs 0.6% senior and 0.7% T2 — but the carry story is compressing FAST

The setup:

✅ AT1 carry ~5.2% (vs sovereign bonds)

✅ Strong April/May reversed weak Q1

✅ Demand technicals strong, supply benign

The problem:

🔴 AT1 carry was 8% start of 2024 → 6% during Iran war March → 5.2% now

🔴 350bp of carry compression in 18 months = most gains already realized

🔴 Returns "highly sensitive to geopolitical risk and weaker macro" per @Bloomberg

🤯 Hyperscalers are only ~3% of the global IG market.

But they're 11% of the Euro IG 15+yr non-financial market.

The whole AI capex debt binge isn't sitting evenly across the curve. It's piled into the very long end where Reverse Yankees live 🏗️

If 2H supply slows (frontloading done, cash flows strong), this corner of the market is set up for a rally.

Long-end Euro credit → the asymmetric 2H trade?