FYI I’m ALL in with $ZBCN I don’t need to diversify because I have that much conviction in THIS project.

@WarrenBuffett famously believes that "diversification is protection against ignorance". I’ll live this way and go all in to something rather than sprinkle my money around.

I WILL add to MY bags for a shorter distance to MY goals. I’m in this for me and MY tribe and the circle of MY friends. Any more questions regarding my loyalty?

Where’s yours to @ZebecNation?

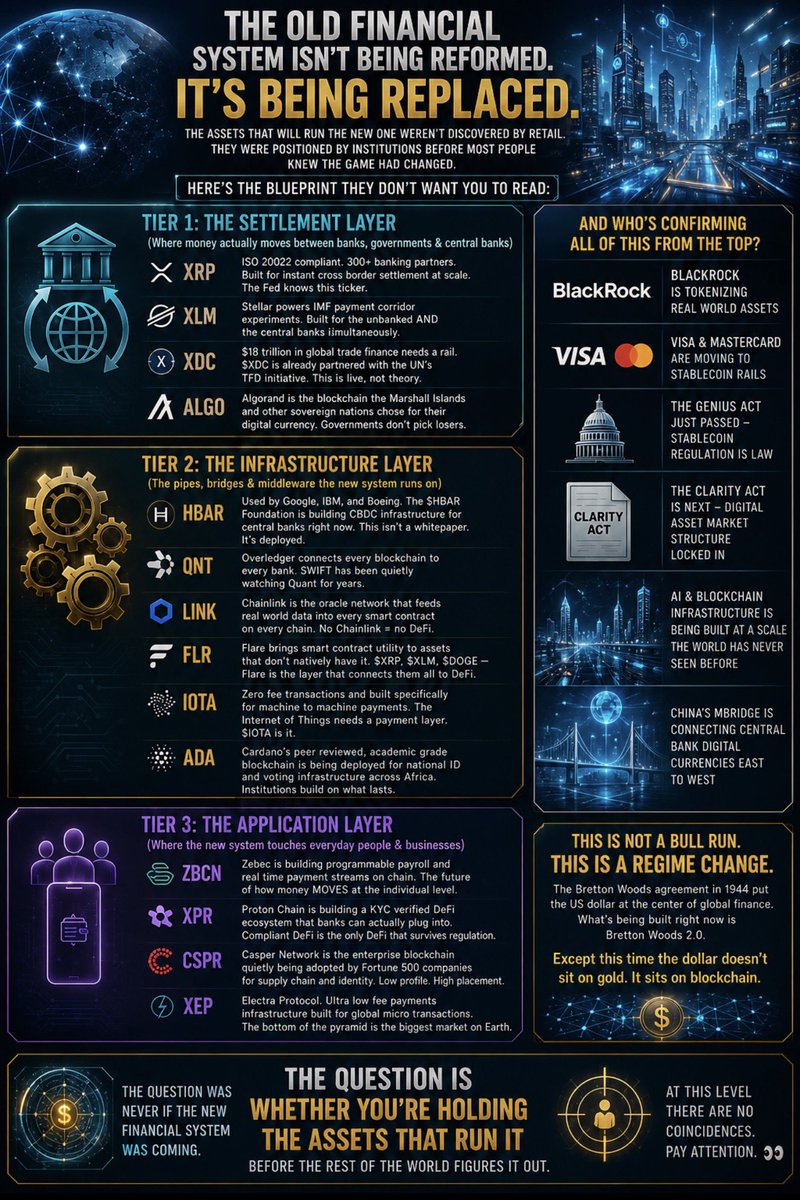

🚨 THE OLD FINANCIAL SYSTEM ISN’T BEING REFORMED.

It’s being replaced.

The assets that will run the new one weren’t discovered by retail.

Here’s the blueprint 👇

⚙️ TIER 1: THE SETTLEMENT LAYER

🔗 $XRP — ISO 20022 compliant. 300+ banking partners. Built for instant cross border settlement at scale. The Fed knows this ticker.

🔗 $XLM — Stellar powers IMF payment corridor experiments. Built for the unbanked AND the central banks simultaneously.

🔗 $XDC — $18 trillion in global trade finance needs a rail. $XDC is already partnered with the UN’s TFD Initiative.

🔗 $ALGO — Algorand is the blockchain the Marshall Islands and other sovereign nations chose for their digital currency.

🏗️ TIER 2: THE INFRASTRUCTURE LAYER

🔗 $HBAR — Used by Google, IBM, and Boeing. The $HBAR Foundation is building CBDC infrastructure for central banks right now.

🔗 $QNT — Overledger connects every blockchain to every bank. SWIFT has been quietly watching Quant for years.

🔗 $LINK — Chainlink is the oracle network that feeds real world data into every smart contract on every chain.

🔗 $FLR — Flare brings smart contract utility to assets that don’t natively have it. $XRP, $XLM, $DOGE — Flare is the layer that connects them all to DeFi.

🔗 $IOTA — Zero fee transactions and built specifically for machine to machine payments. The Internet of Things needs a payment layer. $IOTA is it.

🔗 $ADA — Cardano’s peer reviewed, academic grade blockchain is being deployed for national ID and voting infrastructure across Africa. Institutions build on what lasts.

💸 TIER 3: THE APPLICATION LAYER (Where the new system touches everyday people & businesses)

🔗 $ZBCN — Zebec is building programmable payroll and real time payment streams on chain.

🔗 $XPR — Proton Chain is building a KYC verified DeFi ecosystem that banks can actually plug into.

🔗 $CSPR — Casper Network is the enterprise blockchain quietly being adopted by Fortune 500 companies for supply chain and identity.

🔗 $XEP — Electra Protocol. Ultra low fee payments infrastructure built for global micro transactions.

And who’s confirming all of it?

👉 BlackRock is tokenizing real world assets 👉 Visa & Mastercard are moving to stablecoin rails 👉 The GENIUS Act just passed — stablecoin regulation is law 👉 The CLARITY Act is next — digital asset market structure locked in 👉 Trump flew to Beijing with Larry Fink, Jensen Huang, Tim Cook & the entire US financial power structure on one plane 👉 China’s mBridge is connecting central bank digital currencies East to West

This is not a bull run.

This is a regime change.

The question was never IF the new financial system was coming. It was when.

🤖 TIER 4: THE INTELLIGENCE LAYER

This is the piece nobody’s talking about yet. Settlement layers, infrastructure, applications none of it reaches its potential if humans are still manually operating it.

That’s where AI agents come in.

🔗 Autonomous treasury management Where AI agents will monitor liquidity across chains in real time, rebalancing institutional portfolios without human latency. What takes a team of analysts days happens in milliseconds.

🔗 Cross-border compliance — Agents will handle KYC/AML checks, sanctions screening, and regulatory reporting across jurisdictions simultaneously. The compliance bottleneck that slows global finance disappears.

🔗 Smart contract execution — Agents won’t just read Chainlink oracle data. They’ll act on it. Automatically triggering settlements, collateral calls, and payment streams the moment real-world conditions are met.

🔗 Programmable payroll & streams — AI agents managing on-chain payroll won’t just send money. They’ll optimize timing, currency conversion, and tax routing for every single transaction.

🔗 Central bank policy execution — CBDCs don’t need human intermediaries to distribute stimulus, adjust money supply, or enforce spending parameters. Agents do it at scale, instantly.

The new financial system isn’t just decentralized.

It’s autonomous.

For those that may have missed it go check out the latest episode of The Zebec Gazette from @ZebecNation featuring @XRPZBCNLANTERN and @589CryptoMatt 👇

https://t.co/DPnYiXZSdI

For those that may have missed it go check out the latest episode of The Zebec Gazette from @ZebecNation featuring @XRPZBCNLANTERN and @589CryptoMatt 👇

https://t.co/YiPKu7mS23

🔥 @ZebecNation PODCAST ALERT!

Get ready to level up because we’re locking in with @SatShihan, CEO of @LatticeCash for an absolute FIRE episode of the Zebec Nation Podcast! Podcast will drop June 3rd!! LFG

🚨 @simonb_ldn just walked out of Google HQ London.

One photo. Zero explanation.

Let me tell you why this might be the most important meeting in Web3 payments this year.

Google is racing to launch GCUL, their own Layer-1 blockchain for financial institutions. They need a LIVE payroll use case to beat Stripe & Circle to market.

Zebec already has:

✅ Real-time payroll streaming running TODAY

✅ $85T ACH network access (Nacha member)

✅ $170B+ NatPay integration done

✅ Cards live on Google Pay via Mastercard

✅ Multi-chain across Solana, Base, ETH, BNB

Google doesn’t partner with projects that aren’t ready.

This could be:

→ Zebec payroll rails NATIVE on Google Cloud

→ Zebec integrated into Google Pay for 150M+ users

→ Zebec powering AI agent payments on Google’s UCP protocol

→ Google Cloud as Zebec’s institutional backbone

The timing? Google’s GCUL commercial launch is 2026.

Zebec’s final token unlock just completed. Fully deflationary NOW.

One word: convergence.

$ZBCN @Zebec_HQ@Google

NFA. But pay attention.

🚨 @Google JUST LIT THE FUSE FOR AGENTIC COMMERCE AND @Zebec_HQ MAY BE THE PAYMENT RAILS BENEATH IT 🚨

Most people are focused on Google’s new Universal Cart Platform (UCP).

They’re missing the MUCH bigger story.

🧵👇

1/ Google is building the demand-side AI commerce layer.

With UCP, users can:

• Discover products through Search/Gemini/Maps

• Add items across merchants into one cart

• Checkout in a few taps with Google Pay

Nike. Walmart. Target. Sephora. Shopify merchants.

And it’s expanding into:

• hotel bookings

• local food delivery

• AI-powered purchasing directly from conversations

This is AGENTIC COMMERCE.

AI doesn’t just recommend anymore.

It EXECUTES purchases for you.

2/ But there’s a major problem:

Google controls discovery + checkout…

…but settlement still runs through legacy rails.

That means:

• delayed merchant payouts

• batch processing

• fragmented loyalty systems

• T+1/T+2 settlement delays

• zero real-time cash flow programmability

AI commerce is moving at machine speed.

Traditional finance still moves in batches.

That’s the bottleneck.

3/ This is where Zebec becomes incredibly interesting.

$ZBCN isn’t competing with Google.

It sits UNDER the checkout experience as programmable settlement infrastructure.

Google handles:

→ discovery

→ recommendation

→ execution

Zebec handles:

→ real-time settlement

→ streaming money movement

→ programmable rewards

→ instant liquidity

4/ Imagine the flow:

You tell Gemini:

“Reorder my protein powder.”

AI executes the transaction through Google UCP instantly.

Instead of waiting days for settlement…

Zebec rails stream funds in real time.

Merchant receives liquidity immediately.

No legacy banking lag.

5/ Now the flywheel starts.

Google UCP already supports loyalty integrations.

But traditional rewards systems are static and delayed.

Zebec changes that.

Cashback and rewards could stream back continuously in real time:

• instantly usable

• immediately spendable

• dynamically programmable

AI commerce becomes a closed-loop liquidity engine.