Gold is entering a historically favorable period of the year:

Gold prices have gained +1.5% in July on average over the last 20 years, making it the 2nd-strongest month of the year.

Gold prices have also recorded positive returns in 65% of July months, the 2nd-best win rate of any month.

The strongest July over this period was in 2020, when gold returned +10.7%.

The only better month historically has been August, with an average gain of +1.6% since 2005.

August also posted a 55% win rate, with its strongest year coming in 2011, when gold returned +12.1%.

By comparison, June has historically been the weakest month, with an average decline of -0.4% and just 40% positive readings since 2005.

Seasonality is turning in favor of gold bulls.

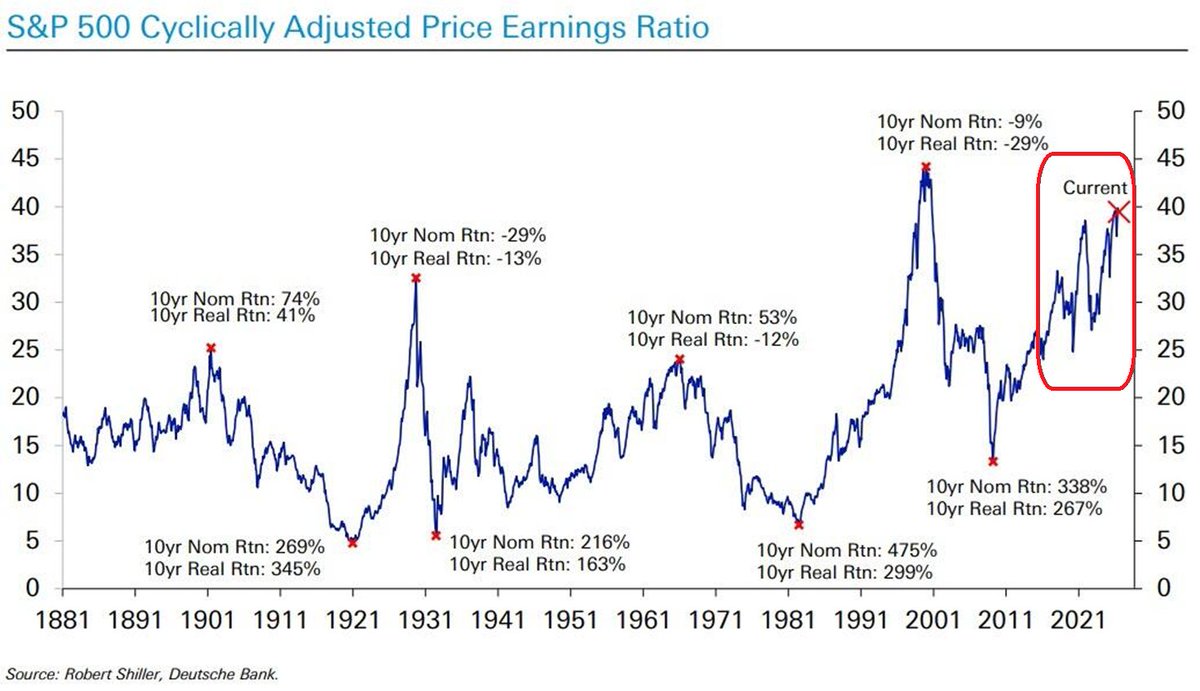

🔴Long-term market valuations are flashing a historic warning for US stocks:

The S&P 500's cyclically adjusted price-to-earnings ratio (CAPE) rose above 40x, the highest since the 2000 Dot-Com Bubble.

Excluding 2000, this is above every other market peak recorded over the last ~140 years.

Following the 2000 peak, the S&P 500 delivered a -9% cumulative nominal return and a -29% cumulative real (after inflation) return over the next 10 years.

At the only other comparable valuation extreme in 1929, the index returned -29% nominal and -13% real over the following decade.

By contrast, buying after major market bottoms has historically produced some of the strongest long-term returns, including a +475% nominal gain following the 1982 low.

History suggests that extreme valuations have consistently led to weak long-term returns.

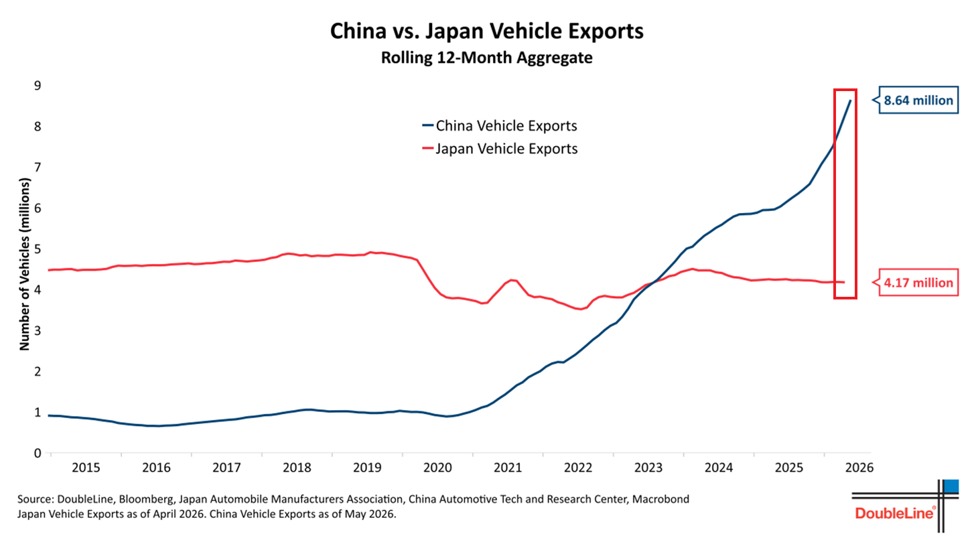

China is now dominating the global auto market:

China's vehicle exports jumped +68.7% YoY in May, to ~930,000.

This is almost +1,100% above levels seen in May 2019.

This comes as new EV exports surged +112.6% YoY, to 424,000, accounting for ~46% of the total.

As a result, China exported a record 8.6 million vehicles in the 12 months ending May.

By comparison, Japan exported just 4.2 million, or -51% fewer, during the same period.

To put this into perspective, China exported just 1.0 million vehicles in 2019, while Japan exported 4.8 million, or +380% more.

China is now the undisputed leader of the global car market.

The single biggest disconnect in markets at the moment is this: oil prices drove the Dollar up when they were rising, but they've not pulled the Dollar back down now that they've fallen sharply. Markets are wrongly fixated on Fed hikes. Won't happen...

https://t.co/7UrzrNNYsi

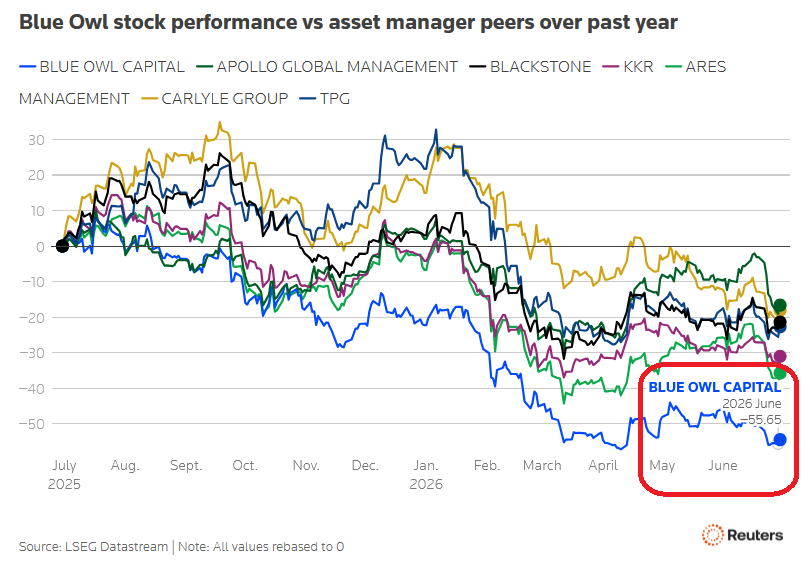

🚨US private credit stocks are plummeting:

Blue Owl Capital shares are down -55.6% over the past 12 months.

This dramatically underperforms Apollo, Blackstone, KKR, Ares, Carlyle, and TPG, all of which are down roughly -17% to -38% over the same period.

This comes as redemption requests at Blue Owl's 2 largest funds totaled $4.7 billion in Q2, still far above the funds' 5% quarterly withdrawal cap.

Its technology-focused fund, OTIC, saw the greatest pressure, with 38.1% of shares tendered for redemption, more than double the 9% to 17% range seen at the largest peer funds that have reported Q2 results.

Its flagship fund, OCIC, saw redemption requests reach 18.8% of shares, alongside $660 million in net outflows.

Across the broader private credit industry, investors requested a record $15.6 billion in redemptions in Q2, with only 38% of requests met, leaving $9.7 billion unmet, the highest amount on record.

The $2 trillion private credit industry crisis is getting worse.