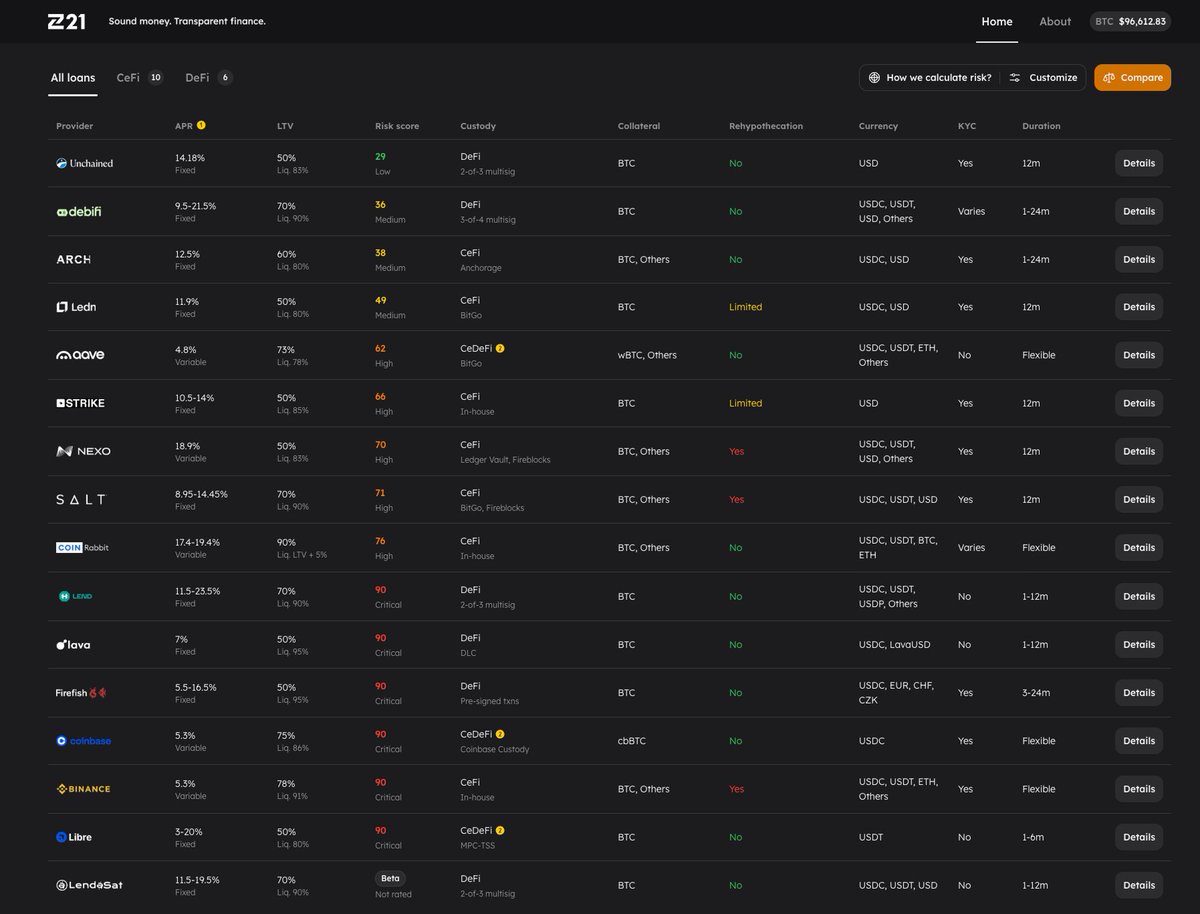

Need to borrow against your Bitcoin but unsure about the hidden risks?

Imagine instantly peeking under the hood of every Bitcoin-backed loan to understand exactly how risky it is.

Now you can.

Introducing Zone21.

Bitcoin-backed lending exploded last bull cycle, but unsafe practices caused tens of billions in losses (remember Celsius, BlockFi, Voyager?).

Now, new lenders promise better practices like minimal rehypothecation and Proof-of-Reserves, but many risks remain hidden and misunderstood.

Bitcoin lending combines two intricate worlds: Bitcoin technology (multisig, DLCs, custody solutions) and traditional finance (debt instruments, liquidity risks).

It's a minefield. Even savvy Bitcoiners struggle to untangle the complexity.

We built Zone21 to fix this.

Several of our team members spent years developing @nunchuk_io, a non-custodial Bitcoin wallet. It taught us the stark difference between real safety and security theater.

We now bring that rigor to analyzing Bitcoin-backed loans.

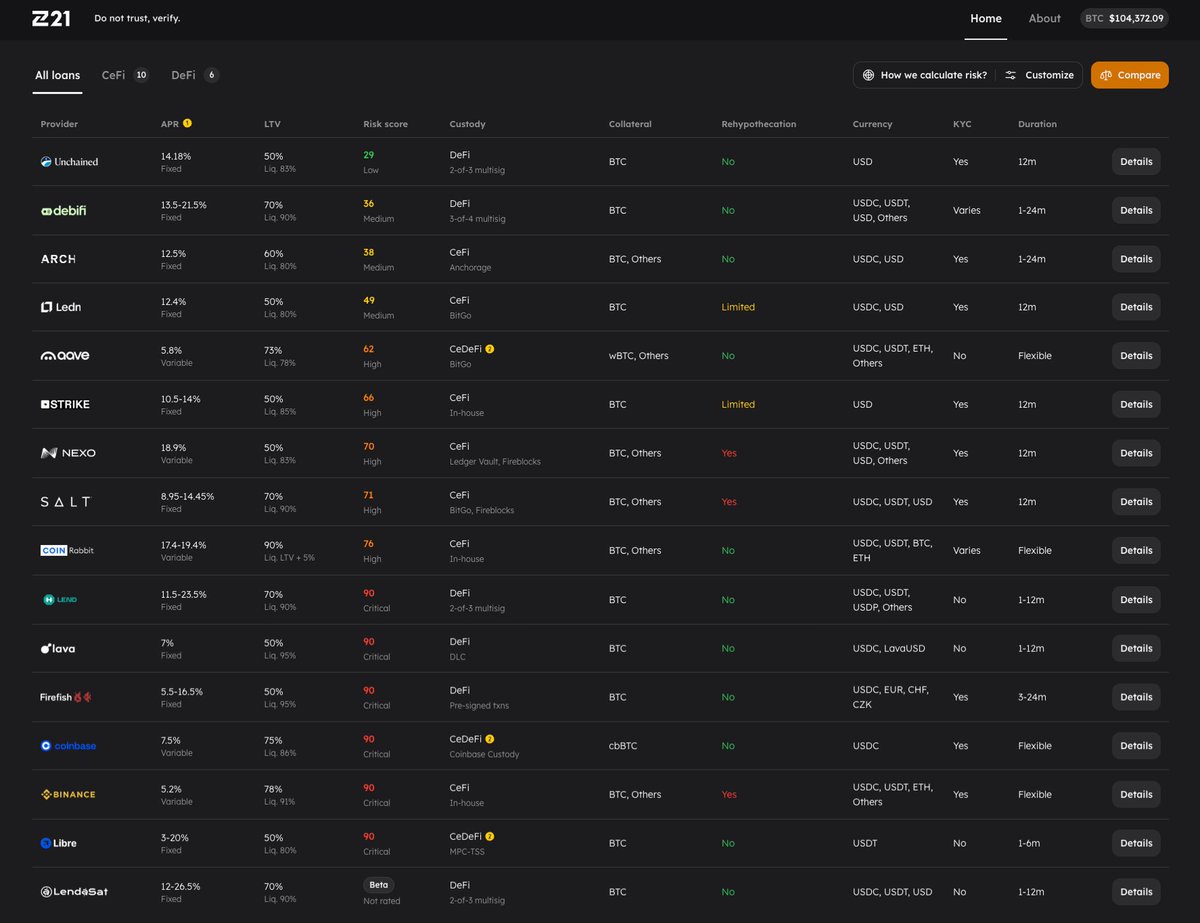

Our Risk Model scores Bitcoin loans across 13 critical factors:

• Collateral type

• Rehypothecation

• Custody

• Security & governance

• Platform reliability

• Oracle integrity

• Liquidation buffer

• Rate & terms

• Transparency

• Loan currency

• Privacy

• Provider history

• Jurisdiction

Each factor measures specific risks. For examples:

• Collateral: Native BTC safest; wrappers add risk.

• Rehypothecation: Hidden leverage amplifies blowups.

• Custody: Controls who can move coins and how safely.

• Transparency: Can outsiders verify code and solvency?

See full details at: https://t.co/AVNT8QG4eh

Zone21 is fully independent:

• No affiliation with lenders.

• No financial advice.

• Built by Bitcoiners, for Bitcoiners.

Our goal is transparent, informed choices when borrowing against your Bitcoin.

Our model isn't perfect; risks evolve continuously.

We welcome feedback, corrections, and insights, especially from lenders themselves.

Explore the model and contribute your thoughts: https://t.co/jTgHKYvErb

Next week, we'll publish a state-of-the-industry report on Bitcoin lending, guided by our Risk Model.

Give us a follow and turn on notifications to stay updated!

AI agents shouldn't get the full key to your kingdom.

Today we're releasing Nunchuk CLI: create a shared Bitcoin wallet with your agent, give it a spending budget, and keep the final say.

Build Bitcoin agents with bounded authority.

The standard for Bitcoin inheritance has officially been raised.

@BTCSessions does a deep dive into our On-Chain Inheritance Protocol: the ONLY solution that gives your heirs a guided experience without giving up your sovereignty.

Don't trust us. Trust the timelock.

Lava announced a $200M fund raise and a new Bitcoin Line of Credit (BLOC) product.

However, the thread below shows a painful, real-time example of the #1 risk in Bitcoin lending: counterparty risk hidden behind a veil of "trustless" marketing.

We are seeing several red flags from the @lava_xyz dispute:

• Users are alleging their collateral was moved to new addresses without their consent.

• The CEO admits the security model changed significantly, moving away from DLCs.

• This fundamental change to the trust model was apparently not communicated to users.

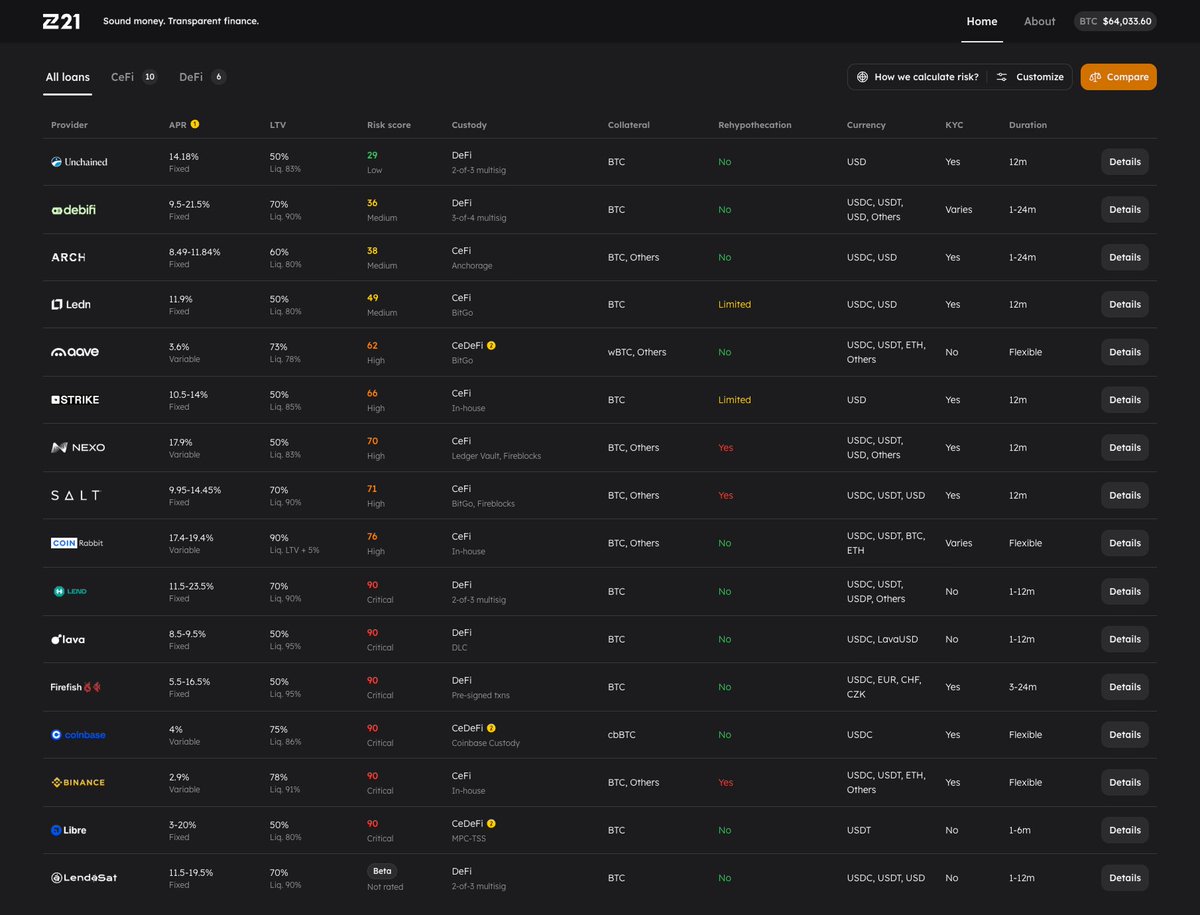

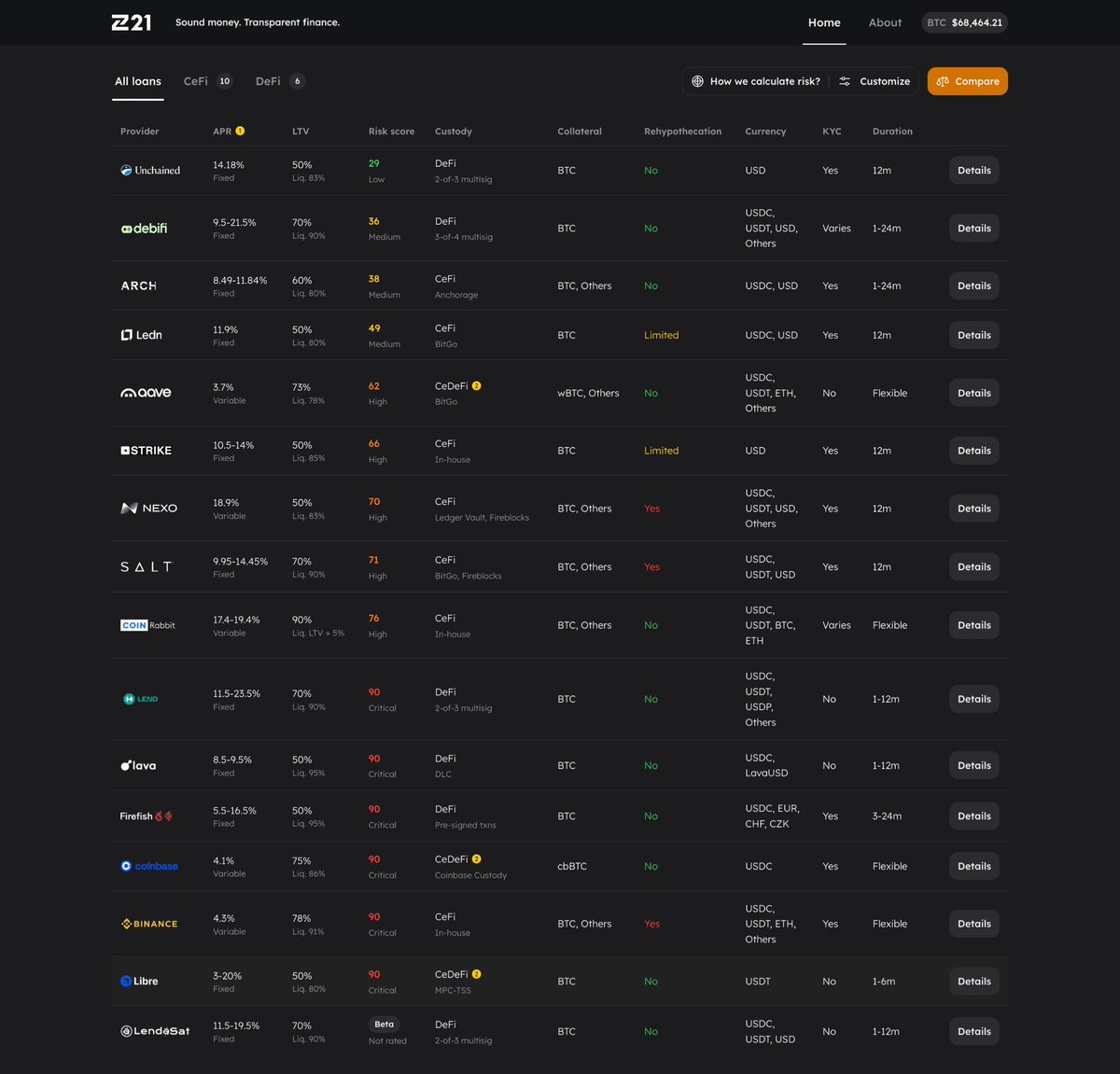

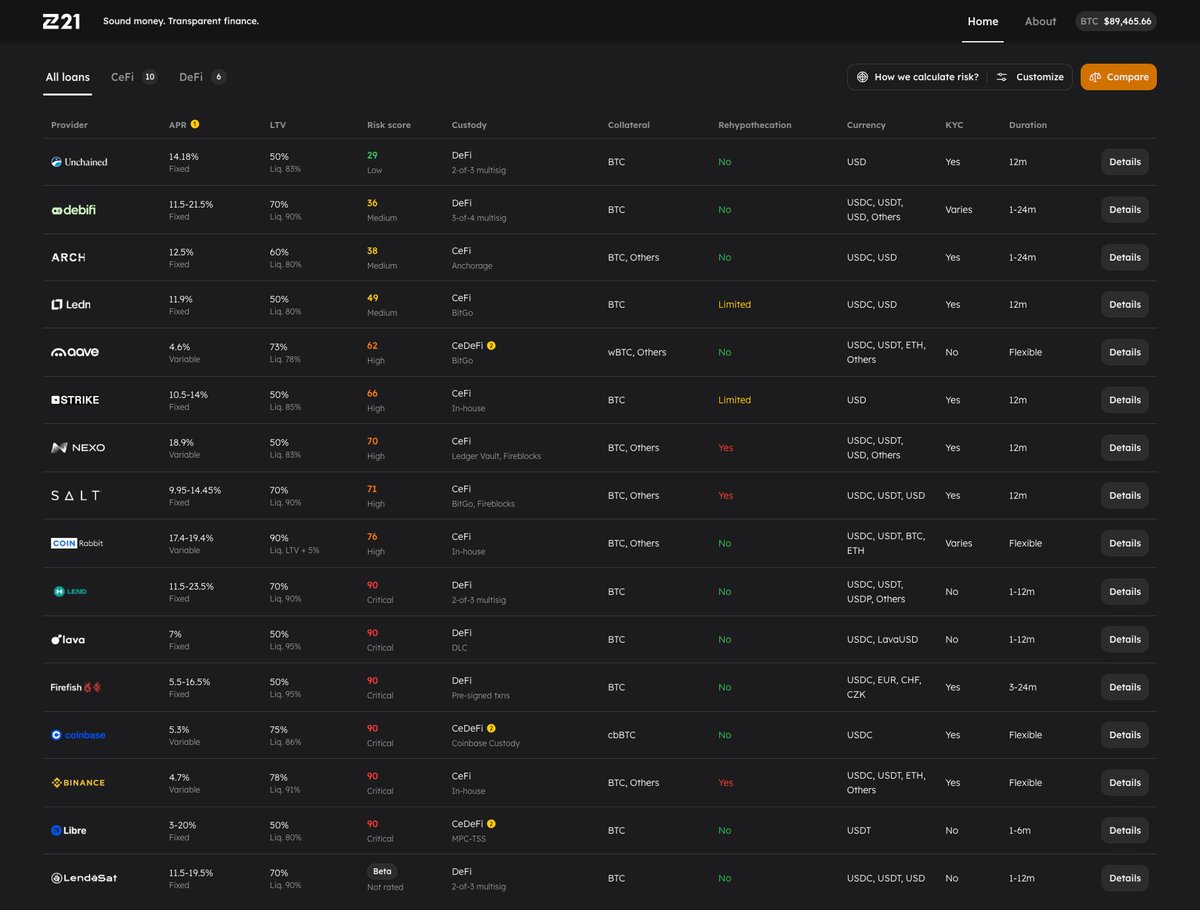

This situation is precisely why our security report 5 months ago assigned Lava a Risk Score of 90 (Critical).

We were bullish on their original DLC-based approach but identified the exact flaws that created this single-point-of-failure:

1. Closed-source key generation in the mobile app.

2. A single, in-house oracle.

The fact that Lava could unilaterally move user collateral confirms this. It implies only two possibilities:

1. The user's private keys were never private.

2. The Lava-controlled oracle published false data to move the funds.

Both scenarios mean the product was never truly self-custodial.

This is why we are building Zone21. The gap between marketing promises and technical reality can be catastrophic. Independent, in-depth risk analysis is essential for the entire space.

Hold on. Lava was founded as DLC based and "non custodial"; ie local keys (for what that's worth - not 100% accurate whilst lender is also the oracle, but, baby steps).

1. I have an active loan.

2. I used to have "contracts updating, please wait" type loading screens.

3. There was a forced migration process a few weeks ago.

4. There are forced updates in-app; black screen making it unusable until you update.

5. I no longer have the "contracts updating" screen.

You say now you don't use DLCs and there's a bunch of corporate speak about trust and audits or something.

Shehzan, did you make me install an update where my own app ended my DLC based loan arrangement and enter this new arrangement?

Did you change the trust model without telling the customer?

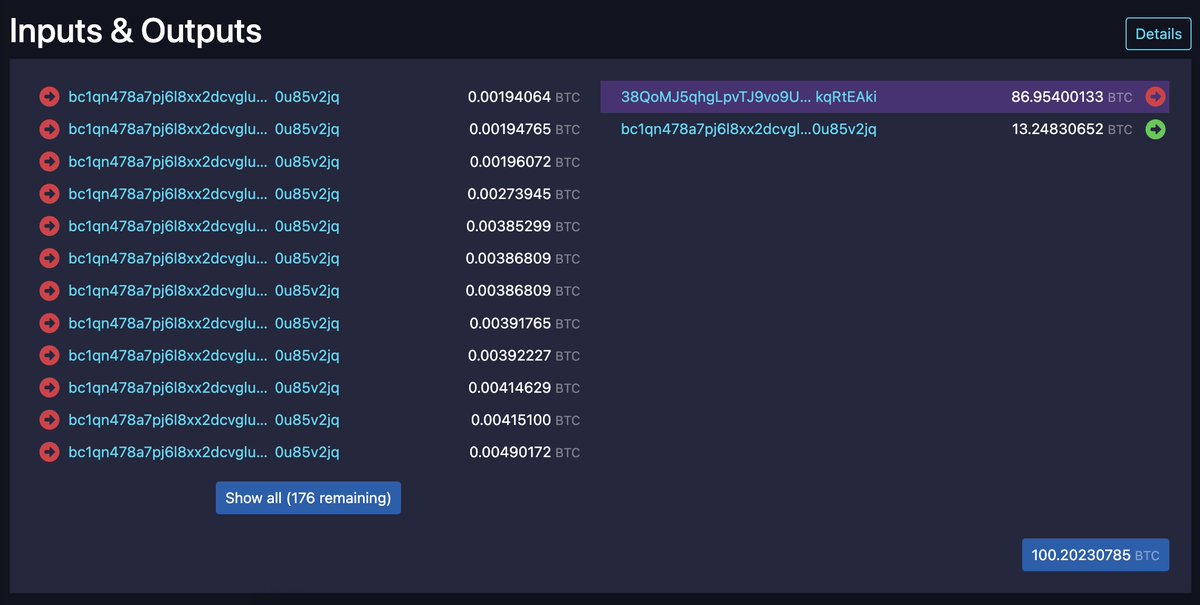

Doing some @mempool sleuthing on @lava_xyz

Looks like they originally were self-custodial, your loan would be made by locking your collateral in a 2-of-2 multisig

However, post "upgrade" funds are held in a pooled single-sig address that regularly consolidates to @krakenfx

Doing some @mempool sleuthing on @lava_xyz

Looks like they originally were self-custodial, your loan would be made by locking your collateral in a 2-of-2 multisig

However, post "upgrade" funds are held in a pooled single-sig address that regularly consolidates to @krakenfx

The specific timelock/refund feature was from their claimed model (i.e., their whitepapers). Their GitHub repo also has a fork of rust-dlc.

We also tried out their product around the same time. That's how we verified other things, like their use of a privately-issued LavaUSD.

But we were unable to verify their core DLC mechanics. The app is a closed-source black box.

The fact that their core security model was unverifiable is precisely why it was assigned a Critical (90) score. If we can't verify it, we have to assume it's trust-based.

The Jurisdiction score reflects which laws protect the borrower when something goes wrong (e.g., stable courts, clear bankruptcy process, strong creditor rights). In that sense, a US/Delaware entity is strong.

It does not rate the company's operational compliance, like switching from DeFi to CeFi without the proper money transmitter licenses.

That's a completely different (and massive) risk that could get them into legal troubles, which is what Cory talks about here.

Also note that Lava's current report page is regarding their old setup. It will be updated once there's clarity on this new centralized setup.

Our Bitcoin-Backed Lending 2025 report covers everything you need to know about CeFi, CeDeFi, and True DeFi lending options. Including cost vs control trade-offs, hidden risks, and future outlook.

Read the complete analysis here:

https://t.co/DtWzAZjCmi

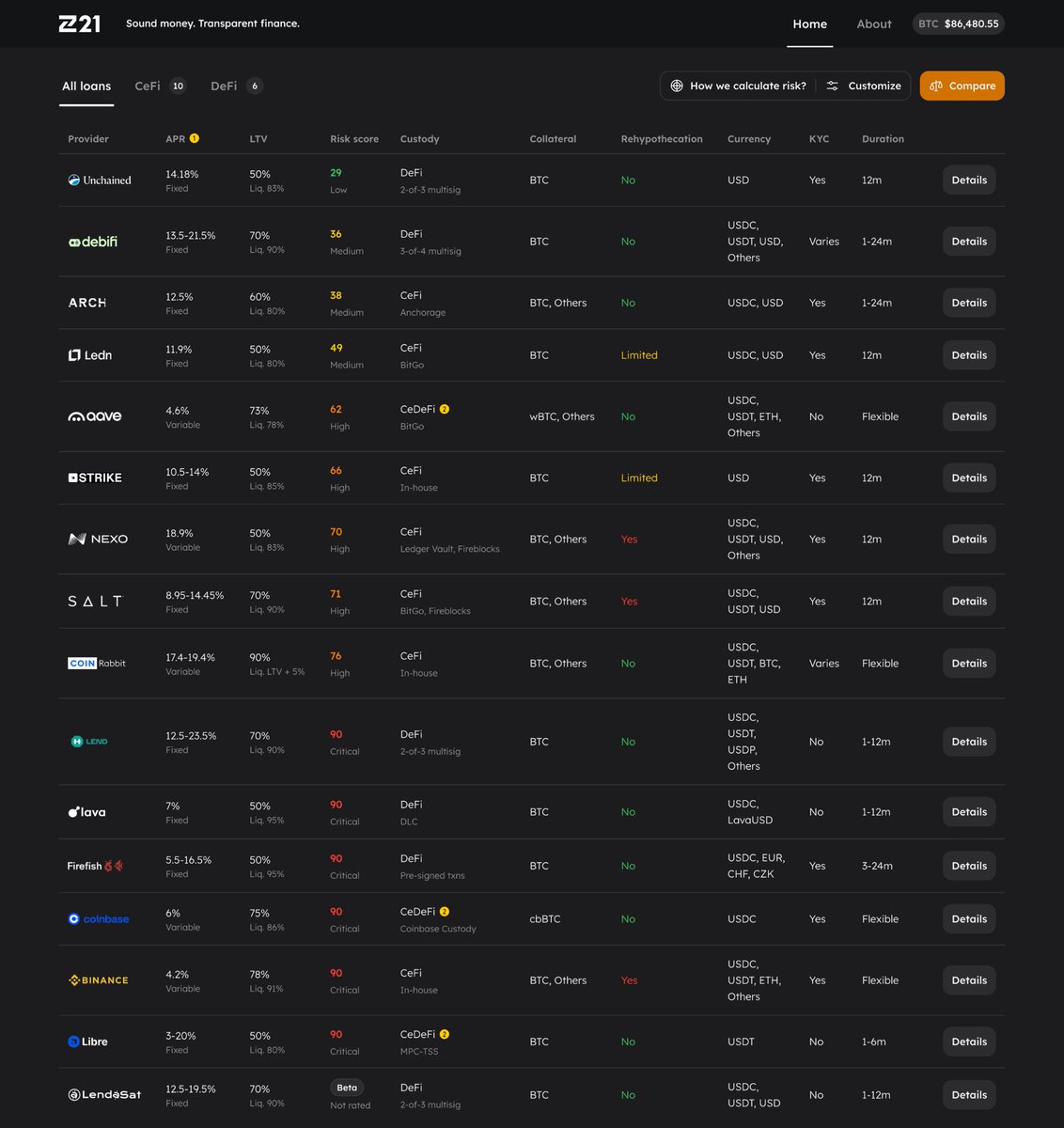

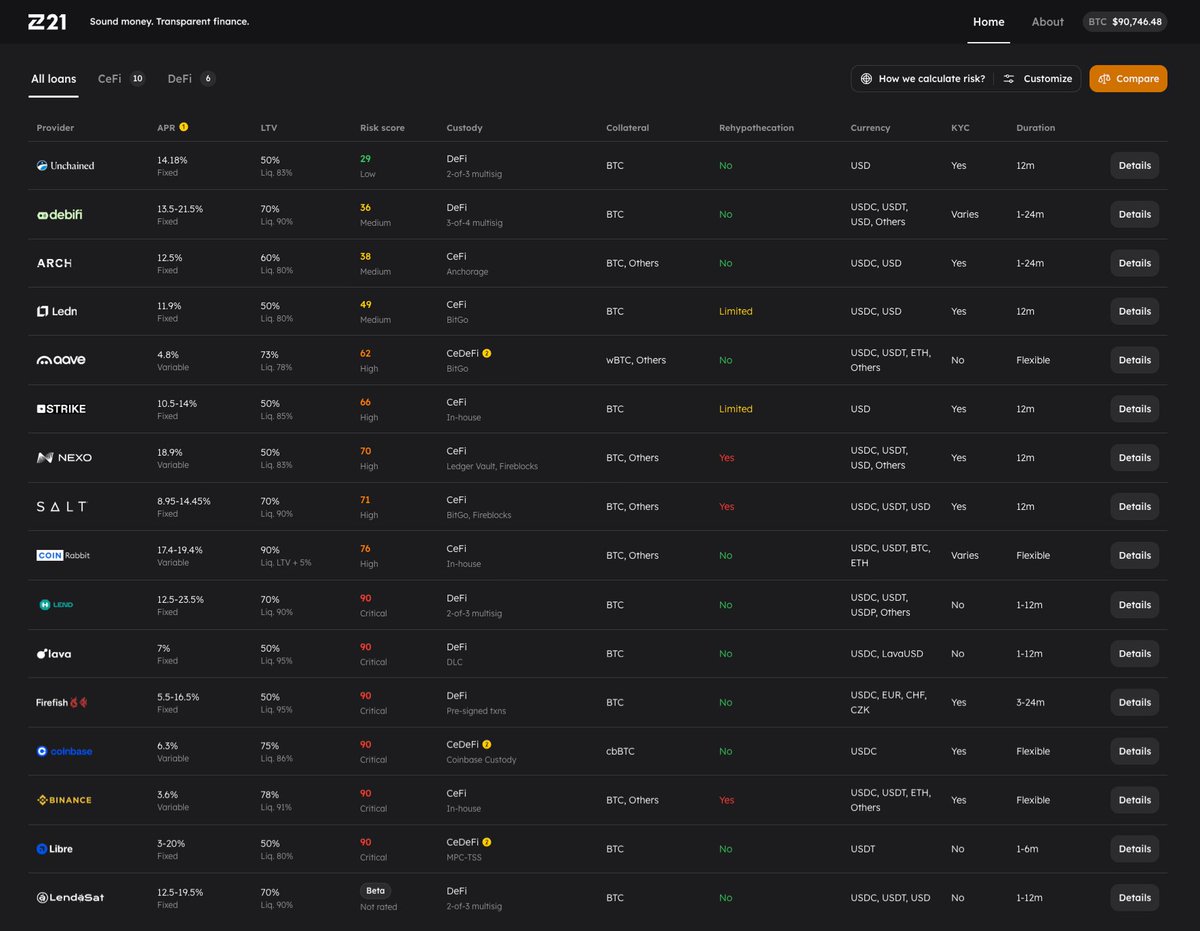

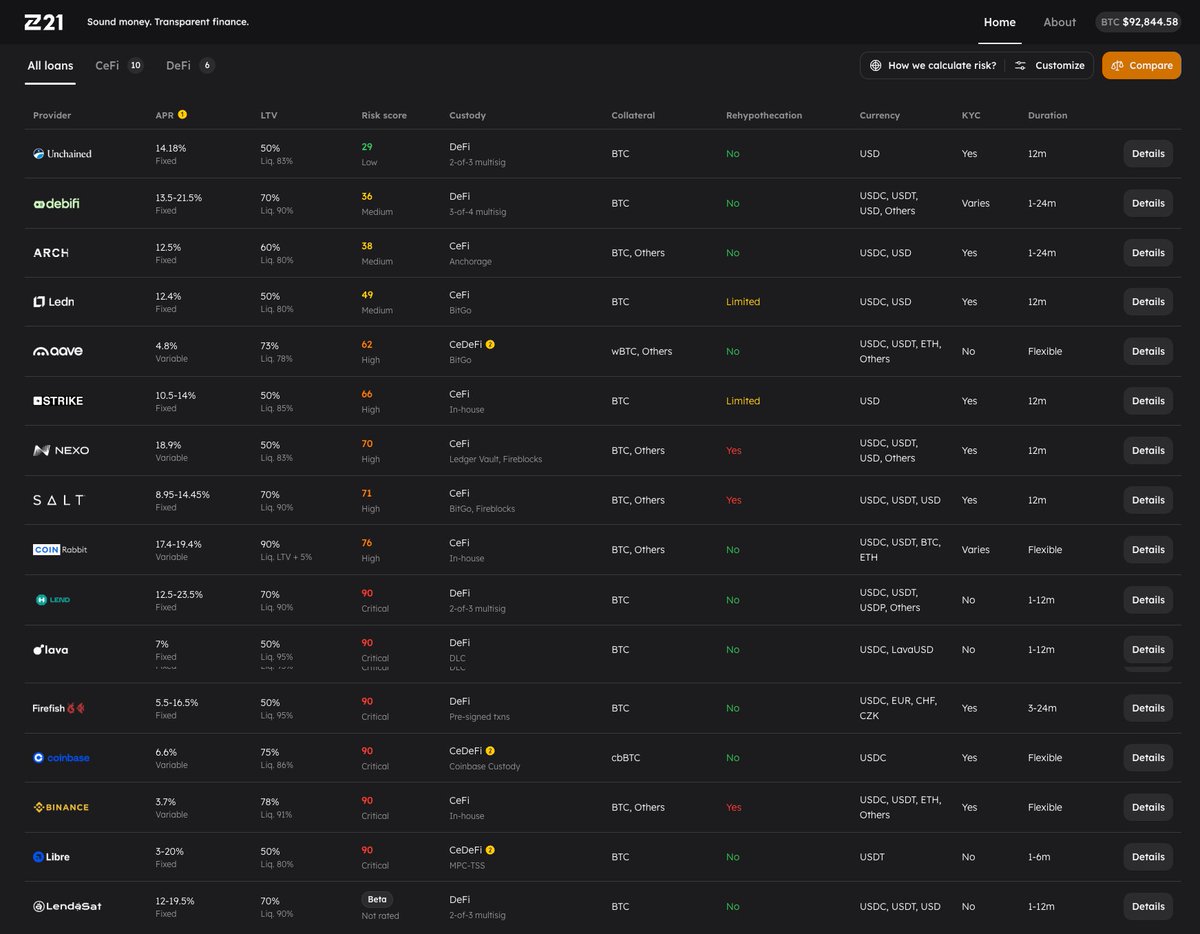

Need to borrow against your Bitcoin but unsure about the hidden risks?

Imagine instantly peeking under the hood of every Bitcoin-backed loan to understand exactly how risky it is.

Now you can.

Introducing Zone21.

Bitcoin-backed lending exploded last bull cycle, but unsafe practices caused tens of billions in losses (remember Celsius, BlockFi, Voyager?).

Now, new lenders promise better practices like minimal rehypothecation and Proof-of-Reserves, but many risks remain hidden and misunderstood.

Bitcoin lending combines two intricate worlds: Bitcoin technology (multisig, DLCs, custody solutions) and traditional finance (debt instruments, liquidity risks).

It's a minefield. Even savvy Bitcoiners struggle to untangle the complexity.

We built Zone21 to fix this.

Several of our team members spent years developing @nunchuk_io, a non-custodial Bitcoin wallet. It taught us the stark difference between real safety and security theater.

We now bring that rigor to analyzing Bitcoin-backed loans.

Our Risk Model scores Bitcoin loans across 13 critical factors:

• Collateral type

• Rehypothecation

• Custody

• Security & governance

• Platform reliability

• Oracle integrity

• Liquidation buffer

• Rate & terms

• Transparency

• Loan currency

• Privacy

• Provider history

• Jurisdiction

Each factor measures specific risks. For examples:

• Collateral: Native BTC safest; wrappers add risk.

• Rehypothecation: Hidden leverage amplifies blowups.

• Custody: Controls who can move coins and how safely.

• Transparency: Can outsiders verify code and solvency?

See full details at: https://t.co/AVNT8QG4eh

Zone21 is fully independent:

• No affiliation with lenders.

• No financial advice.

• Built by Bitcoiners, for Bitcoiners.

Our goal is transparent, informed choices when borrowing against your Bitcoin.

Our model isn't perfect; risks evolve continuously.

We welcome feedback, corrections, and insights, especially from lenders themselves.

Explore the model and contribute your thoughts: https://t.co/jTgHKYvErb

Next week, we'll publish a state-of-the-industry report on Bitcoin lending, guided by our Risk Model.

Give us a follow and turn on notifications to stay updated!