Listen to this smart woman. It’s why the silent majority is not being heard right now. But history shows us this over & over, yet still we haven’t learnt.

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

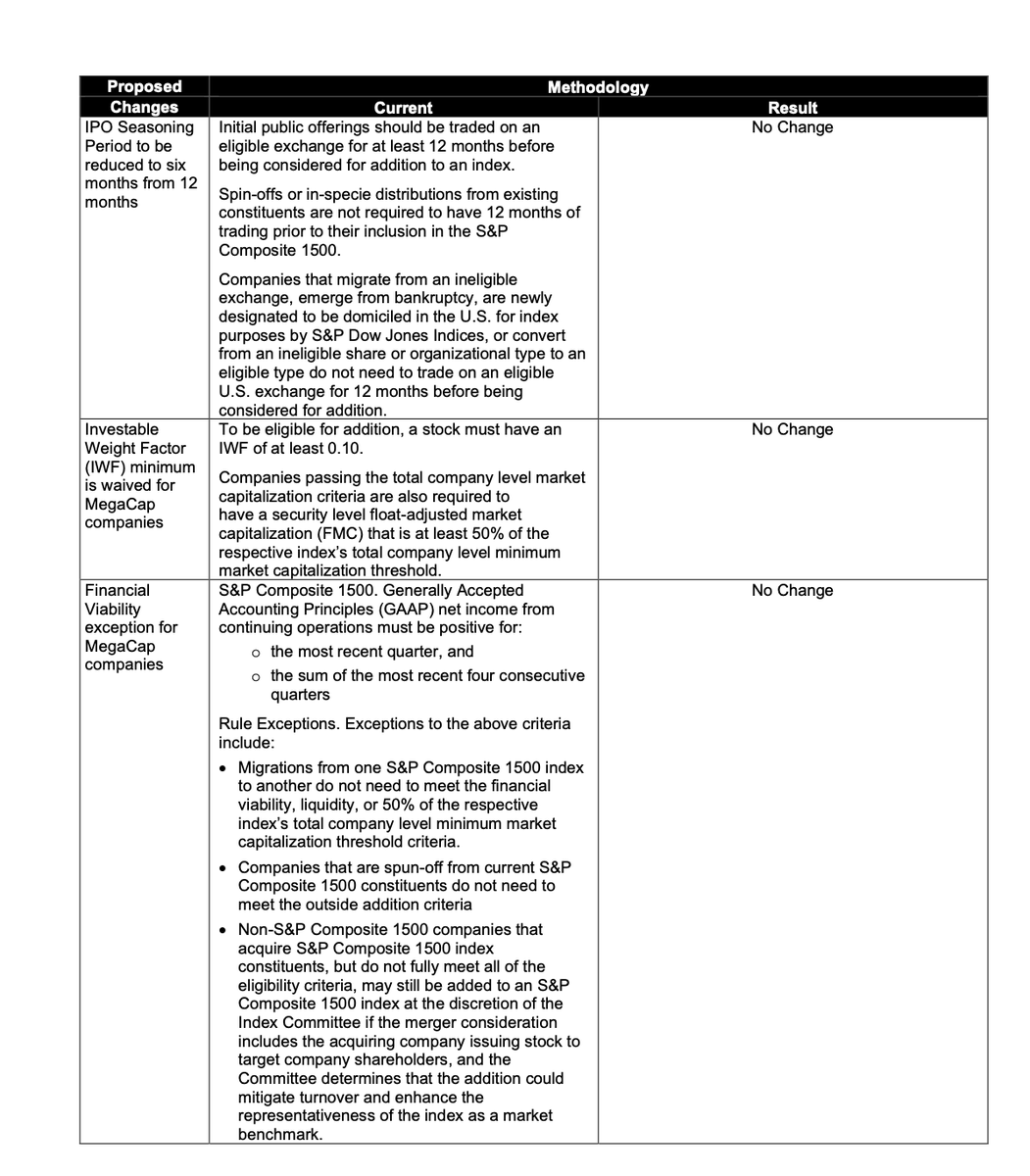

Their reasoning:

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

Croeso Isaac Murray-Macgregor

Looks like a similar player profile to Murray, will be interesting to see how much game time he gets at the start of the season.

He joins Ellis Mee, Blair Murray, Macs Page, Ioan Jones, Jac Davies, Toni Lewis and Callum Woolley as back 3 options

Food for thought.

Trump’s Abraham Gambit in the New Great Game

Halford Mackinder, not the United Nations, is the man to have in mind when looking at Trump’s Iran diplomacy. Mackinder understood that history belongs to those who organize the World Island, Europe, Asia, and Africa with the Middle East as the hinge, not to those who moralize about it from conference halls. Add Sun Tzu and Kipling’s Kim and the picture sharpens, the great struggles are won by those who quietly redraw the map and deny their adversaries the ground they once took for granted. Trump, whatever his critics say, is trying to do exactly that.

That is why he has inserted the Abraham Accords into the center of the Iran talks. This is not decoration on a nuclear file. It is the strategy, widen the Abraham framework, pull more Arab and Muslim states into open alignment with Israel, and force Tehran to face a region that is becoming harder to intimidate and harder to hold hostage through Hormuz panic or nuclear brinkmanship.

For forty years, the West treated Iran as a technical problem, counting centrifuges and tweaking sanctions while Iran built a business model of proxy war, maritime extortion, and a standing risk premium every time the Strait of Hormuz flashed red. That was its version of the Great Game, a quiet mastery of chaos and chokepoints while Western diplomats congratulated themselves on process.

Trump’s answer is to make that model obsolete. Israel, the UAE, Bahrain, Morocco, and Sudan form the Abraham core, with Saudi Arabia as the decisive prize, while Qatar, Egypt, Jordan, Turkey, and Pakistan are pressed toward a more openly pro‑Accords camp. On the periphery sit Japan and China, both with immense stakes in the energy routes and trade corridors that run through this same geography.

In a sense, the Abraham framework is a Middle Eastern echo of the old Helsinki Accords, economic cooperation and security guarantees used to buy stability, but without a single distant empire calling every shot and without pretending that abstract process is a substitute for hard power.

This is strategy in the old sense, change the terrain, align the coalition, and deny the adversary the fractured landscape on which he thrives. If it works, the Middle East stops being where growth goes to die every time Tehran rattles Hormuz and becomes the connective tissue of a harder, more productive order, a coherent zone across Mackinder’s World Island tied together not by slogans but by ports, pipelines, grids, shipping lanes, and capital disciplined by security.

Investors need to wake up. The rules of the game are changing in real time, the old world is not coming back. A new Great Game is underway, and the prize is no longer territory but the authority to price risk and allocate capital across the World Island.

Those still trading on the assumptions of the previous era are not positioning for the future, they are underwriting decline and clinging to a map history has already marked obsolete.

#CLX results deliver a return to growth that looks set to accelerate.

New markets such as Digital Infrastructure along with Government and Defence provide increasing opportunities.

Current forecasts leaving the door ajar for potential upgrades as momentum builds.

This @HedgieMarkets post illustrates where the infinity scalable asset-light technology model meets the physical realities of an asset-heavy business that faces an upward sloping supply curve.

We have long argued that AI compute is just another bit-atom commodity (like crypto) that uses a lot natural resources to create a valuable (unlike crypto) virtual asset.

On the bit side, Big Tech is a price-maker with fat margins. On the atom side, a price-taker.

Big Tech grew up in bits — search, social, e-commerce, office software: asset-light, infinitely scalable, natural monopolies. Build once, serve billions, watch costs fall every year. So they assume AI is the same game and will spend whatever it takes to own the market.

But inference is also atoms, i.e. land, critical minerals and electrons, which are mostly molecules. In the commodity world, competition drives price to marginal cost: P = MC, which is upward sloping as volume rises. The better the models get, the faster they compete their own margins down to the physical floor which rises with volume.

You can already see it. Microsoft just cancelled Claude Code because the cost to run it exceeded the value it returned — demand retreating the moment price met real cost. The irony: the customer pulling back was itself a hyperscaler. In April, Uber confirmed once again that AI compute demand is price elastic.

Bottom line: they assumed AI costs would keep falling like they always did on the bit side; however, on the atom side, there is a hard floor that likely rises in the short run.

I am not denying that the margins are still fat. But it’s not the same model. These guys are running towards obsolescing their own pricing power. Why did Rockefeller stop at the gas station and not vertically integrate into cars?

In Episode 80 of the Sceptic: Andrew Orlowski unpacks Palantir, AI and the truth about UK mobile phone signal. Plus: Dean Rainey on his follow-up film on vaccine injuries in Canada.

Live tomorrow at 11am (Friday 22nd May) on @VOXmarkets , I have the pleasure again of discussing all things smallcap with equity analyst & commentator Paul Scott.

As usual, we'll try to answer any of your investment questions too. Everyone is welcome.

https://t.co/P3UMvbKPA7

Live tomorrow at 11am (Friday 22nd May) on @VOXmarkets , I have the pleasure again of discussing all things smallcap with equity analyst & commentator Paul Scott.

As usual, we'll try to answer any of your investment questions too. Everyone is welcome.

https://t.co/P3UMvbKPA7

Die EU baut gerade die größte Bürokratiemaschine der Wirtschaftsgeschichte auf. Ab August 2026 droht tausenden kleinen Händlern faktisch das Aus im europäischen Binnenmarkt.

Die EU zerstört die gesamte Wirtschaft! So gibt es keine Chance mehr auf eine Rückkehr an die Weltspitze.

#PPWR #EU #Bürokratie #Amazon

Wahnsinn: Die neue EU Verpackungsverordnung zwingt Händler künftig dazu sich in jedem einzelnen EU Land separat zu registrieren und zusätzlich Bevollmächtigte zu benennen. Selbst kleine Onlinehändler sollen dadurch massive Zusatzkosten und einen enormen Verwaltungsaufwand tragen obwohl viele Betriebe bereits heute unter hohen Energie und Steuerkosten leiden.

Folgen: Die Verordnung betrifft praktisch alle Händler Hersteller Fulfillment Dienstleister und Marktplatzverkäufer in Europa. Zusätzlich kommen neue Recyclingquoten QR Codes Materialvorgaben und Dokumentationspflichten hinzu. Experten warnen bereits offen davor dass viele kleine Unternehmen wirtschaftlich aus dem EU Binnenmarkt gedrängt werden könnten.

Die EU verliert zunehmend jedes Gefühl für wirtschaftliche Realität und zerstört damit systematisch den europäischen Mittelstand.

Vielen Dank für den wichtigen Hinweis!

Quelle: (Händlerbund)

https://t.co/sMFVWBXyGF

Quite a rap sheet for Starmer here, though given his lack of interest in economic policy it's hard to know how much of this is actually down to Reeves, Rayner, Miliband...

#PEN excellent news this morning, a first win with a N. American military customer in the technical documentation space.

Demand as expected is clearly there and with what should become an integral part of Siemens Teamcenter, prospects look exciting.