At Sohn, Gavin Baker provided a pretty compelling argument as to why CoreWeave's $CRWV business model is differentiated and durable, lamenting that he couldn't invest in their 2023 round at a $1B valuation (due to a conflict stemming from an existing investment in competitor Crusoe).

"CoreWeave, Crusoe, Nebius, Lambda.. is the category durable today? Is it a transitional arbitrage on hyperscaler capex and token friction?"

"I absolutely think it's durable... The way to think of running one of these clusters is like driving a Formula 1 race car... It looks easy but it's really hard... The reason a company like CoreWeave can charge a huge premium for their GPU hours is because all GPU hours are not the same. And those CoreWeave GPUs are being utilized 2-3x more per hour on average than the GPUs from a bottom of the barrel provider. And by the way, this all goes for Crusoe and Nebius and the other high-quality neoclouds...

The hyperscalers were competing with people running these Formula 1 cars and they were doing overnight shifts in 18-wheelers trying to stay awake to deliver the lower cost. And that's not what AI is about. Now, I think they're making this mental and cultural shift and they've made it, but some of these neoclouds have a very durable business model."

$CRWV $NBIS

#Meta’s Hyperion Data Center in Louisiana. Quick walkthrough while reading some things:

Gross IT: 2GW

Capex / MW: ~$13.5M

Total Capex: $27.6B

$Meta + $OWL elected to hold a bond offering for the $27.6B, 2GW campus

75% leverage (bonds) at a 6.4% all-in yield

Equity split: 19% OWL / 7% META

The bonds have a 24-year term, while Meta’s lease term is only 4 years

To get debt holders comfort the structure includes a Residual Value Guarantee held by meta for the tail end duration of the life of the bonds until maturity (16 years)

If Meta walks after year 4, bondholders still need collateral value and lease coverage sufficient to support repayment of the $27B of leverage

So at bond maturity if the asset value is worth less than the the $27.3B of principal balance, Meta is obligated to pay the difference directly

In return Meta receives IG-credit financing economics

This is infra….

$GLXY @galaxyhq#DataCenterBusiness#Helios

Since some of my posts earlier this day may create some confusion, I want to make it up to you leaving a small research gold nugget.

I just identified a recent ERCOT document which shows that two possible large loads, which are related to the Wind Energy Transmission Texas (WETT), are eligible for ERCOT's batch zero.

There is a good chance that those two cases (1000MW & 800MW) belong to Galaxy's Helios campus. The 1000MW probably to the switching station Pitchfork (currently under construction) and the 800MW to the existing switching station Cottonwood. This is just an assumption, no guarantees.

@AOC The idea that all billionaires got their money by exploiting peopl doesn't hold up to any scrutiny.

JK Rowling wrote books about cheeky wizards. I invented a better way to make virtual reality headsets and games to play on them. We just made things people wanted.

Market is taking in a transfer of value from yield to longer duration and credit (i.e. better tenant quality)

Pretty outstanding that you are building at RE returns (9-11% YOC), financing at infra like leverage (80%+ LTC), and exiting like functional credit

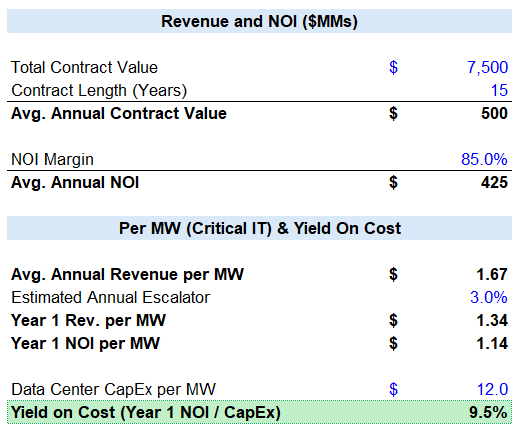

At first glance, the economics on this deal appear somewhat underwhelming with an estimated "yield-on-cost" of 9.5%. These economics are identical to the deal Applied announced in October 2025 with an unnamed "Investment-Grade Hyperscaler". What's interesting about this announcement is that Applied specifically refers to a "High Investment-Grade Hyperscaler".

A bit of digging and you can deduce that the October deal was with Oracle. "High" Investment-Grade Hyperscaler certainly refers to either Meta, Amazon, Microsoft, or Google.

Given the difference in financing costs and cap-rates for Oracle-related projects vs. those leased to Meta, Amazon, Microsoft, or Google, this most recently announced deal should result in notably higher levered returns for Applied.. So while the headline economics are unchanged from six months ago, this transaction is another data point suggesting the underlying equity returns to data center developers continue to improve.

$APLD $WULF $CORZ $GLXY $CIFR $HUT

SITUATION UPDATE: OpenAI CFO Sarah Friar pushes back on reports the company missed internal targets, saying OpenAI is facing “a vertical wall of demand” and if anything “doesn’t have enough compute.”

$/GPU/hour doesn't tell the whole story. If your AI cloud isn't purpose-built, you're paying for idle time.

A thread on the 5 factors for true AI TCO 🧵

New Anthropic research: Project Deal.

We created a marketplace for employees in our San Francisco office, with one big twist. We tasked Claude with buying, selling and negotiating on our colleagues’ behalf.

If you’d told me a few years ago this is where we’d be on Iran, I’d have said you were high:

1. Nuke program set back years. Enrichment and reprocessing gutted, weaponization sites destroyed, Fordow inoperable, Natanz in ruins, a generation of senior nuclear scientists eliminated.

2. Ballistic missile program crippled. Monthly production down from 100 to near zero. Roughly half the regime’s missiles and launchers destroyed. The IRGC Aerospace Force commander who ran the missile enterprise dead.

3. Air defenses devastated. American and Israeli airpower dominating Iranian skies, with strike aircraft operating over the country with near impunity.

4. Full economic warfare. Not just OFAC sanctions anymore, but military pressure layered on top: naval blockade, near-zero oil exports, choked imports, wrecked steel and petrochemical sectors, triple-digit inflation, and a currency that is effectively worthless.

5. Regime decapitation. Khamenei dead. Larijani dead. Hundreds of senior IRGC, intelligence, military, and Basij commanders dead including the IRGC commander-in-chief, the armed forces chief of staff, and the Aerospace Force commander. Mojtaba Khamenei inheriting a hollowed-out regime with no supreme authority and a gutted command structure.

6. The region turning on Tehran. Gulf states shutting down the sanctions-busting, money-laundering, and financial escape routes the regime has relied on for years. No Arab capital willing to throw Iran a lifeline. China and Russia providing limited support.

7. Proxy network shattered. Hezbollah and Hamas heavily degraded. Houthi political leadership taking direct Israeli strikes. The “Axis of Resistance” and “ring of fire” are now more slogans than real threats.

8. Syrian corridor severed. Assad is gone. The new government in Damascus is actively blocking Iranian arms transfers to Hezbollah: arresting smugglers and publicly declaring Syria will no longer serve as a transit corridor for Tehran’s terrorists. The land bridge to the Mediterranean that took decades to build is effectively closed.

9. Lebanon pivoting west. With Hezbollah battered and resupply choked, Israel and Lebanon have opened direct peace talks for the first time since 1983, aimed at a permanent agreement and Hezbollah’s disarmament. Beirut now asserting that the Lebanese armed forces alone are responsible for national defense. This is a direct repudiation of Hezbollah’s “resistance” claim. TBD.

10. Deterrence exposed as a bluff. Four direct attacks on Israel — April 2024, October 2024, June 2025, March 2026 — failed to impose strategic cost and instead triggered heavy retaliation. Iran couldn’t even use Syria as a launchpad.

11.Economy hollowed out from within. Power shortages, water crises, factory shutdowns, pension unrest, and mass protests. Nationwide demonstrations erupted in December 2025 after a year of economic freefall, with bazaaris, oil workers, and truckers, the regime’s traditional support base, joining strikes across all 31 provinces. Running out of oil storage space. Fuel shortages. The worst crisis since 1979.

12. Scientific and technical brain drain. Beyond the nuclear experts, Iran has lost a generation of irreplaceable expertise in missile design, centrifuge engineering, and weapons development. The survivors are harder to recruit and easier to deter.

13. Naval power decimated. The regular navy shattered, IRGC navy taking growing losses as CENTCOM moves to reopen Hormuz.

And against all of this: the regime forced to play its Hormuz card at its weakest possible moment when the U.S. has options instead of when we didn’t: namely, Tehran with nuclear-armed ICBMs, 10,000 ballistic missiles, a Chinese- and Russian-built military, hundreds of thousands of attack drones, a fully operational terror network, and hundreds of billions of dollars to harden its economy.

That’s the strategic picture. It’s extraordinary. Much more to do but I can’t comprehend how much has been achieved.

Ken Griffin is “appalled” that Zohran used his $238m Manhattan penthouse in his tax the rich promotional video

Citadel is now apparently considering bailing on their construction plans to build a new office in Midtown. The project would involve $6 billion in spending and would create 15k permanent jobs in NYC according to Citadel’s COO

"It is shameful that he used Ken's name as the example of those who supposedly aren't carrying their fair share of the burdens associated with New York City's often costly and wasteful spending," the email said. "In doing so, the mayor has once again manifested the ignorance and disdain of the elite political class towards those who have been consistently committed to building one of the greatest cities in the world."

Would be both incredibly petty but also hilarious if Citadel backed out of their plans over this

The Montreal Expos are exiting the baseball space. During Q2 and Q3 2026, we will transition to acquiring high-performance GPU assets. This is all part of our long-term vision to become a fully integrated GPU-as-a-Service (GPUaaS) and AI-native cloud solutions provider.

Biggest piece of alpha right now is stop anchoring to bank credit views on large offtakers

Focus on utility underwriting.

Across IA/PPA structures, LC sizing, collateral thresholds, and forward credit requirements are moving with load sometimes materially wider, sometimes tighter than lender frameworks depending on market and utility foresight

That dispersion isn’t being priced correctly.