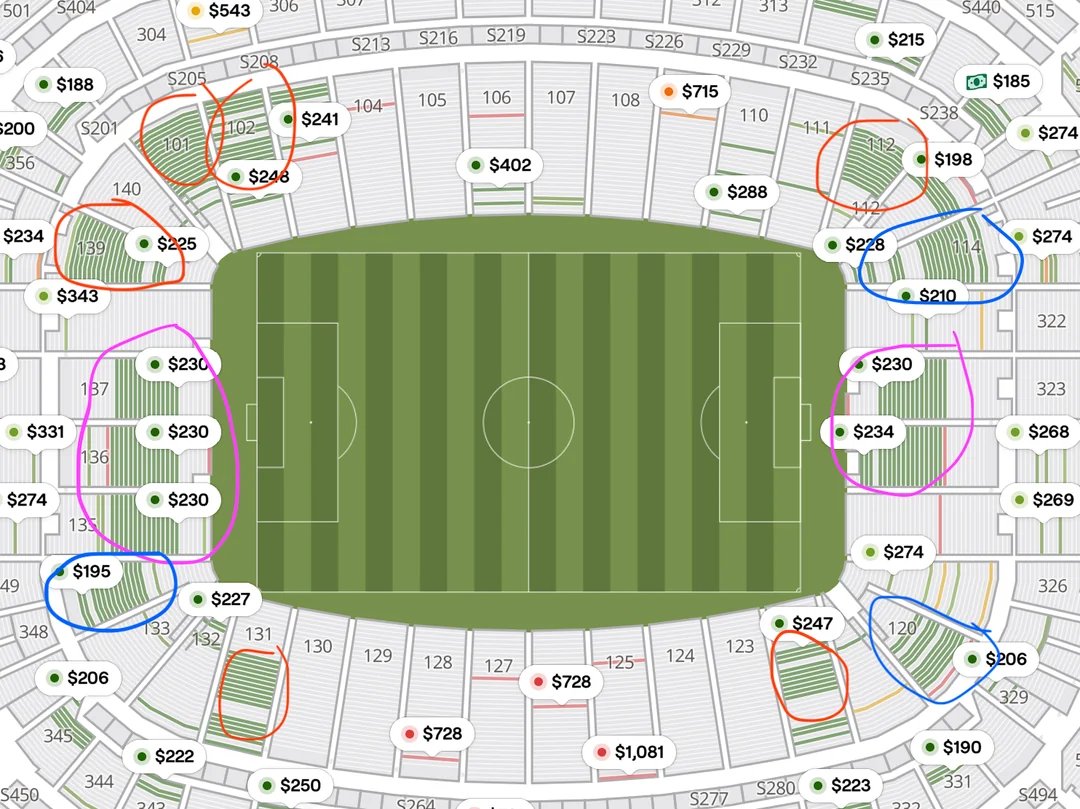

I believe we now have evidence of FIFA's World Cup ticketing shell game: FIFA is colluding with third-party resale platforms for its own supply management.

Look at this SeatGeek map (secondary market!) for Saudi Arabia vs Cape Verde. The circled areas are not random single resale tickets, but large, contiguous blocks of seats: entire rows and swaths in sections 101/102, 112/113, 119/120, 134–137, 139, ...

The blue circles appeared weeks ago, then the purple blocks suddenly showed up a day or two ago, and the red blocks seem to have appeared recently too.

That's not what ordinary fan or even commercial scalper resale looks like who resell pairs, fours, and scattered seats. Instead, this looks like inventory being dumped in bulk onto secondary markets, at prices below FIFA's official site.

Why doesn't FIFA just lower prices on its own site Probably because official price cuts could trigger refund demands, chargebacks, or consumer-protection headaches from fans who already bought at much higher prices.

Instead FIFA keeps official prices high, avoids openly admitting the market-clearing price is lower, and moves unsold inventory through third-party resale platforms instead.

Some people are optimistic about stock returns, some are pessimistic. And, when presented with a similar menu of investment options, investors will make very different choices.

In this paper, we try to make progress toward understanding why, using the actual decisions that investors make in their 401(k) retirement plans. We extend demand estimation techniques to portfolio choice using a new identification strategy. This allows us to recover varying expectations across investors for different assets.

Some people are optimistic about stock returns, some are pessimistic. And, when presented with a similar menu of investment options, investors will make very different choices.

In this paper, we try to make progress toward understanding why, using the actual decisions that investors make in their 401(k) retirement plans. We extend demand estimation techniques to portfolio choice using a new identification strategy. This allows us to recover varying expectations across investors for different assets.

Our estimates indicate that investors vary widely in their expectations, and that expectations are predictable by the industry investors work in, local economic conditions, and the recent performance of investors’ employers.

Heterogeneity in beliefs (or disagreement) is costly for investors, reducing risk adjusted returns by about 0.7 percent per year. However, the limited menu of choices offered by retirement plans may help insulate investors from larger mistakes they might if individual stocks and bonds were featured on the plan menu.

Congratulations to my colleague @JonathanColmer and co-authors for being recognized with an AEJ Best Paper award for their paper "Do Carbon Offsets Offset Carbon?" in AEJ: Applied!

Paper is here: https://t.co/Wrk6nVYLnS

State-dependent pricing matters most when trend inflation is high... but that's also when menu cost models are least tractable.

I make progress in a new paper, solving the mean field game analytically and deriving a tractable linear Phillips curve for menu cost models:🧵

1/12

Very happy to be joining @UVAEcon as an AP this fall!

Thank you to all the amazing people I met on the job market, and to my advisors Florian & Kaspar (not on Twitter), @k_sonin and @evajanster.

They each have a series of papers that cover multiple fields. Check out their websites here:

- https://t.co/8tDDqxdMqU

- https://t.co/tBmPbPULGH

They will contribute to an exciting body of research by junior faculty at Virginia Econ!

https://t.co/Y3I4fVLwQi

I'm thrilled that David Van Dijcke (@packlesshepherd) and Francesco Ruggieri (@_FRuggieri) will be joining @UVAEcon this fall.

You may know their work! David's JMP extends RDD to distributional outcomes. Francesco's quantifies the effects of taxes for *all* local US governments.

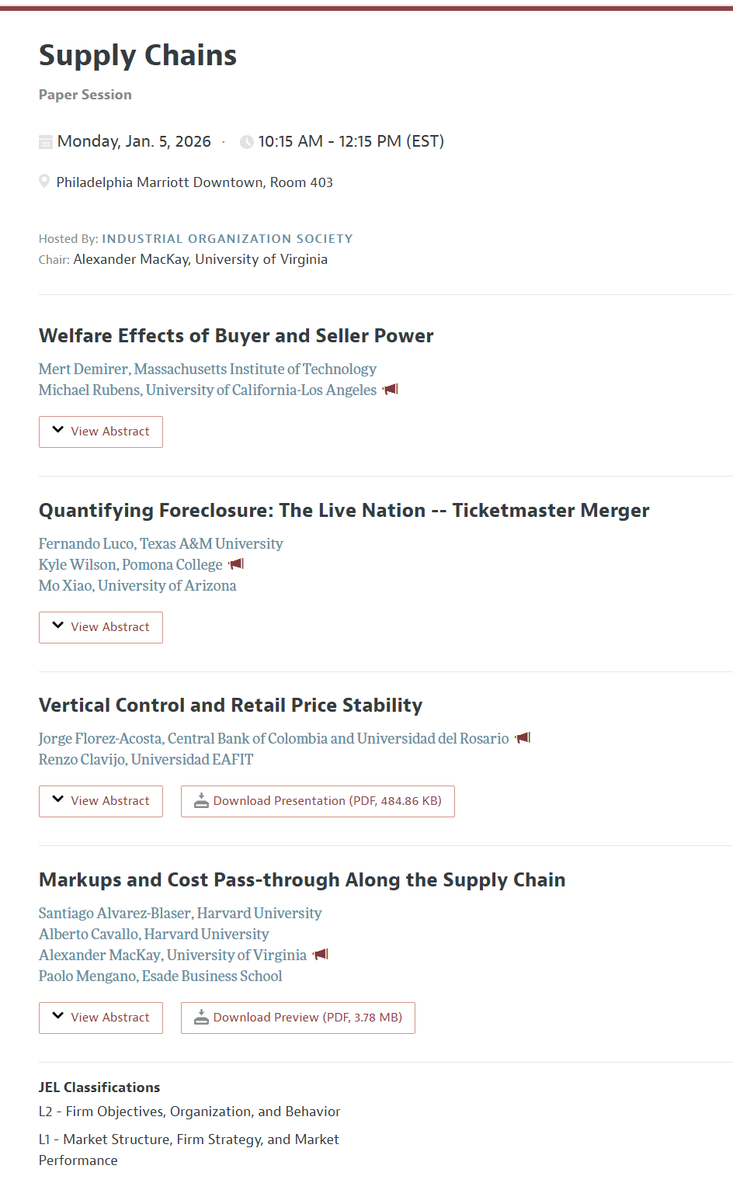

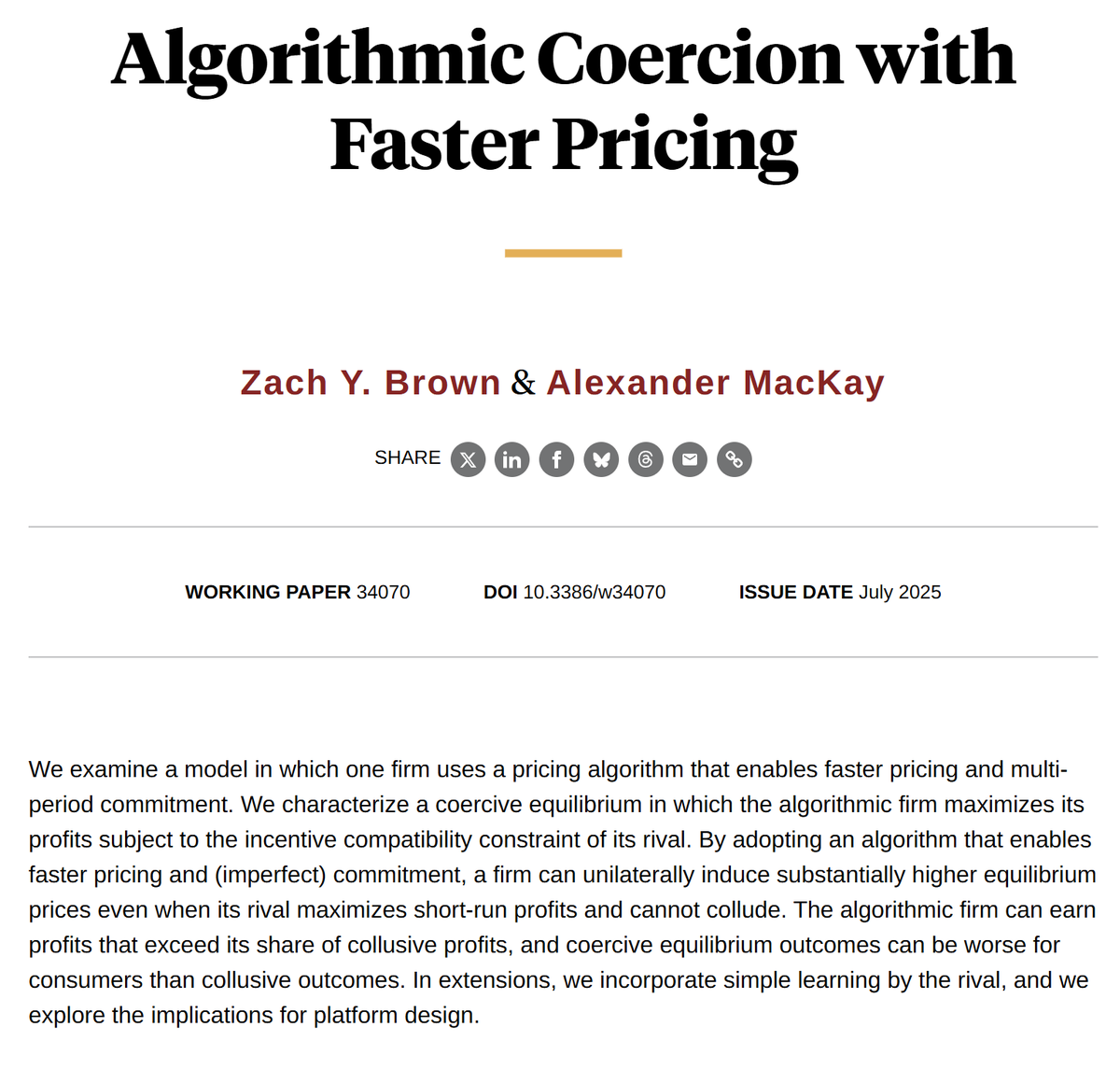

New NBER WP on algorithmic "coercion."

Unlike collusion, coercion can be achieved by a single firm's pricing algorithm.

It can be worse for consumers than collusion.

@nberpubs

Same product. Same store. Same time. But on Instacart, different customers may see different prices.

My story on a fascinating new experiment from @Groundwork & @ConsumerReports, and on how the idea of a single price is breaking down in the digital age:

Same product. Same store. Same time. But on Instacart, different customers may see different prices.

My story on a fascinating new experiment from @Groundwork & @ConsumerReports, and on how the idea of a single price is breaking down in the digital age:

Tomorrow, I'm joining a panel of lawyers in NYC to talk about algorithmic collusion and coercion. If you are a interested in the current cases and law around pricing algorithms, you can sign up through the NYSBA website here:

https://t.co/S24WPfQ7yg