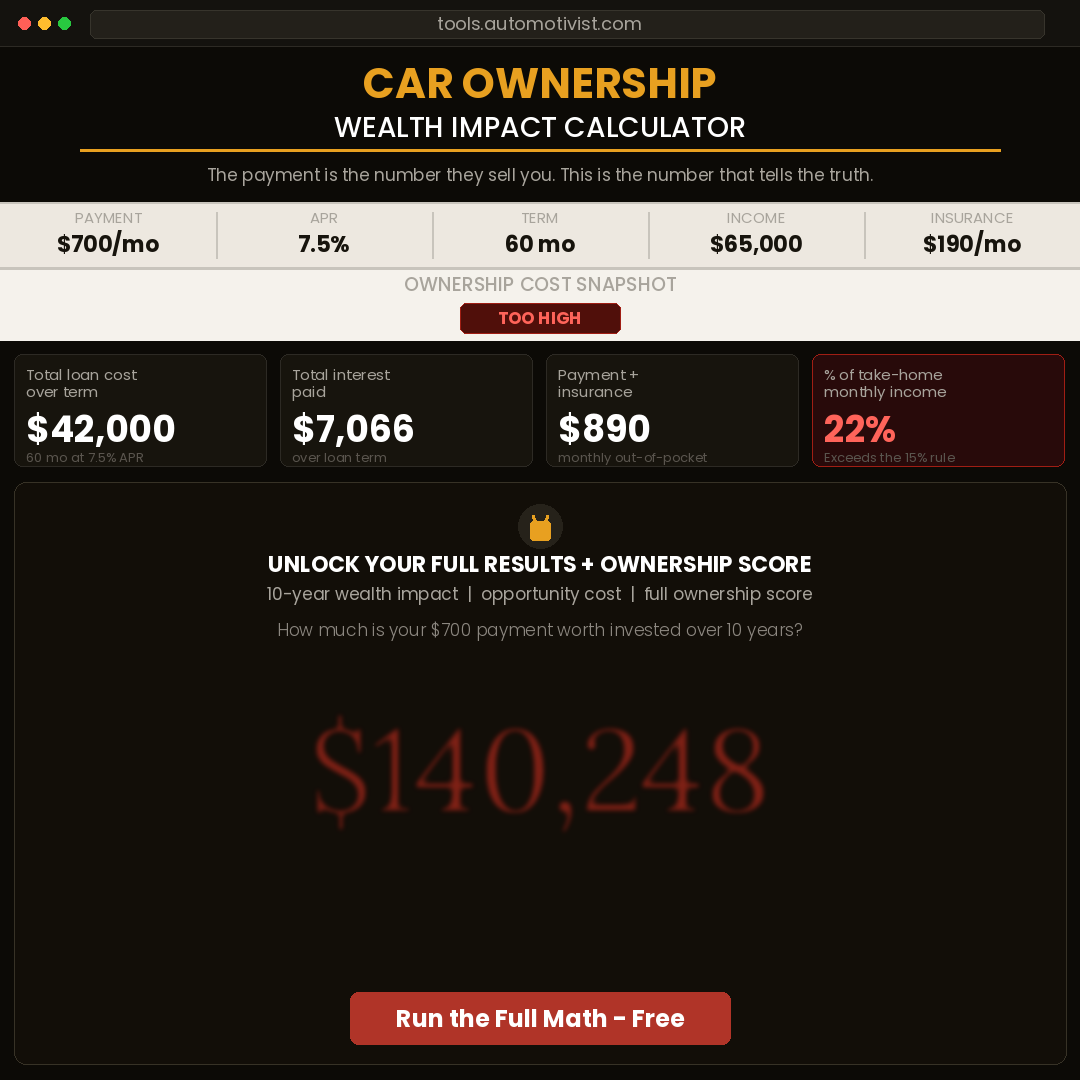

The number your dealership will never show you.

Not your payment. Not your rate. Not your trade-in.

The number that tells you what your car is actually costing you

in wealth you will never build.

I put it in a free calculator. 2 minutes. Run it.

Insurance: $188/month. Gas at current prices: roughly $150. Maintenance arrives on its own schedule.

Not one of those lines came up in the room where you signed.

The payment was built to fit a room, not a budget.

AAA tracked what a new car actually costs to own in 2026: $964/month.

The finance office quoted $680.

That $284 difference - insurance, gas, maintenance - never appeared in the room where you signed.

Sold the G35 for $12,000. The modifications cost more than that.

Never technically underwater on the loan. But total money in versus what came back - nobody ran that number at trade-in.

Every car decision I make now starts there. I break the framework down every Friday.

I break down the full negative equity exit math every Friday - payoff vs. market value, when rolling makes sense and when it does not, the equity threshold before any deal works in your favor. Friday's issue has the framework.

That $159 gap is not the new car. It is ownership drag from the one they traded in, repackaged as a fresh monthly number.

The equity position before any trade-in conversation is the calculation the finance office will not run for you.

$932/month. That is what Q1 buyers paid when they rolled negative equity forward.

Typical new-car buyer: $773. The $159 gap is debt from the last deal.

Their APR: 7.9%. Market average: 6.9%.

Source: Edmunds, Q1 2026.

https://t.co/9y3yCESQf5

30.9% of Q1 2026 trade-ins were underwater. Average negative equity: $7,183 - an all-time Q1 record.

90.2% financed at 72 months or longer. 43% went to 84.

Average payment when it rolls forward: $932/month. Buyer without negative equity: $773.

Source: Edmunds, Q1 2026.

Three years into this Tesla and I know every line of what it costs me monthly. Payment. Insurance. Home charging on solar - close to zero. License tabs.

The G35 I barely knew the payment.

The finance office sells you one number because one number is what moves you toward the signature. Everything else is ownership drag that arrives after you leave the lot.

That full stack breakdown runs every Friday in the newsletter.

The finance office did not forget to include insurance in your payment.

They built the payment they needed you to say yes to. Insurance arrives on a different bill. That is not an oversight. It is the design.

$181 a month. That is what car insurance costs on average in 2026 - up 18% from last year.

Add it to the $680 average payment: $861 before gas, before maintenance.

The finance office quoted one of those three lines.

Source: The Zebra, 2026.

https://t.co/ODM1TRByPD

The GT3 has a payment. On a 36-month lease it is around ,800 a month. I know that number because it makes the goal concrete instead of aspirational. Most people let ownership drag keep them from ever running it. I run that framework every Friday in the newsletter.

Two hours negotiating the sticker. Twenty-three minutes in the F&I office.

The second room is where the deal actually happens. I spent a year working the first one.

Marcus. 36. Atlanta. $88,000/year.

2025 Toyota Camry XSE. $673/month payment. $483/month in insurance, gas, and maintenance.

Total: $1,156/month. 15.8% of gross.

Owes $32,500. Worth $29,800. Underwater $2,700.

He negotiated $1,100 off. Dealer rate: 8.9%. His credit union was at 5.9%. That difference over 60 months: $2,800.

He won the negotiation. He did not know there were two of them.

https://t.co/aTMh2IXNO6

Walked into the Cayenne deal with my own financing at 4.49%. The dealer offered 7.8%.

I had already sat in the car for 45 minutes by then. I knew what they expected me to say.

The test drive is designed to close you before the rate conversation. Knowing that does not make the car less beautiful. It just changes the math you walk in with.

I break the full pre-deal checklist down every week in the newsletter.

20.3% of new-car buyers in Q4 2025 left the lot paying over $1,000 a month. An all-time record.

On $65K, the 15% ceiling is $812. A $1,000 payment is $188 over. That is $2,256 a year.

Payment brain made the number feel normal before they left the showroom. The lot never corrected them.

Source: Edmunds, Q4 2025.

https://t.co/aWfk1nuhKP