What drove macroeconomic fluctuations over the past 700 years?

In our 🚨 new working paper 🚨 “A Millennium of UK Business Cycles: Insights from Structural VAR Analysis” (with haroon Mumtaz and @_Gabor_Pinter_ ), we show:

🧵SWP 1045 by Rodrigo Guimaraes, Gabor Pinter + Jean-Charles Wijnandts (all BoE) explores how bond market liquidity affects how long-term treasury yields reacts to US monetary policy shocks.

https://t.co/mEEvwE7UNh

📢 We are hiring📢

A great chance to be part of our diverse + talented research team at a really interesting time. If you have a PhD / will have one by end 2024 please apply! Deadline is 13 Nov

https://t.co/EMpUZQFPRF

More details + application form at: https://t.co/mvJVADaROA

If you are an economist interested in machine learning, or AI more generally, here you can find a beautiful discussion by Thomas Sargent on the origins of ML/AI and its economic applications/developments.

Link: https://t.co/iZm9DNoDAW

Really interesting reading. #EconTwitter

The trading activity of LDIs and pension funds (especially their linker flows) can explain this relative mispricing. Hedge funds respond to mispricing but it doesn't constitute arbitrage – they adjust their bond portfolios appropriately, but don't hedge it with inflation swaps.

Our paper uses UK micro data to study the relative mispricing of inflation-linked bonds, nominal bonds and inflation swaps - one of the largest examples of the violation of the law of one price (Fleckenstein, Longstaff, and @HannoLustig , 2014).

https://t.co/5zuXlqD7r1

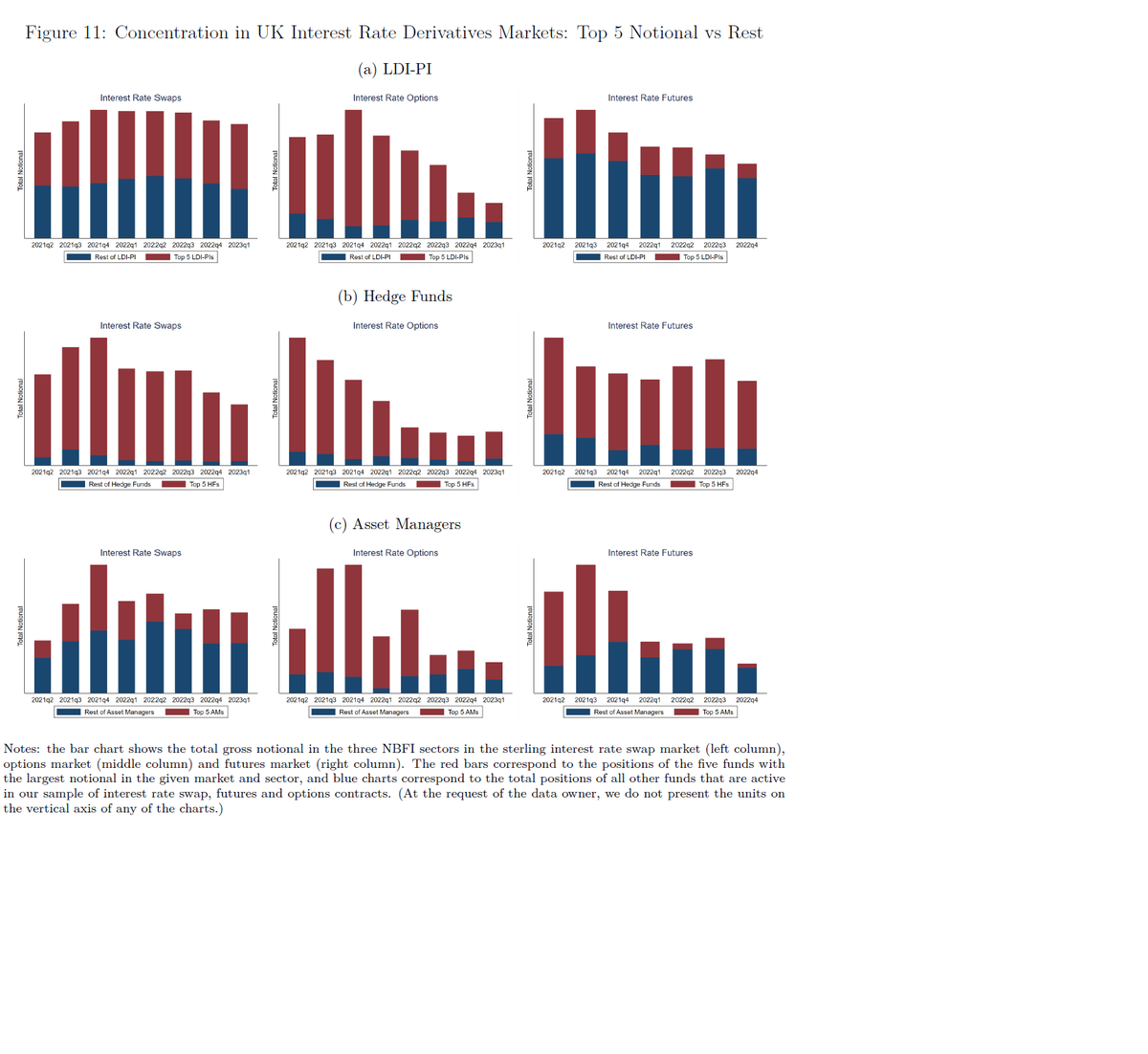

🧵SWP 1032 by Gabor Pinter + Danny Walker (both BoE) looks at interest rate risk across non-bank financial intermediaries using transaction level data on gilt, interest rate swap, futures + options market

https://t.co/6b5pp0ge5q

@TomW100@BoE_Research thank you for the comments, Tom! The analysis in the paper uses a subsample of SMMD where repo counterparties could be matched with gilt transactions during the crisis period. In future revisions, I’ll try to improve this match.

🧵SWP 1019 by Gabor Pintér combines several sources of transaction level data to sketch out a narrative of September 2022 gilt market crisis and documents a number of key stylised facts about how it played out…

https://t.co/vVmCSaqZFW

We are pleased to announce that Nobuhiro Kiyotaki will be joining the Finance Group next year as the 2023/24 Fischer Black Chair! Nobuhiro Kiyotaki is the Harold H. Helm 1920 Professor of Economics and Banking at Princeton. Learn more about his research: https://t.co/ggn43Wo0za

Want to learn more about #CBDC, #stablecoins, #cryptocurrencies and #decentralisedfinance (#defi)? Join us (in person or virtually) for our flagship conference on "New Digital Technologies and the Future Financial Landscape" in London, Feb 27-28. Programme and registration link:

Call for Papers: Workshop on Non-Bank Financial Intermediaries on 4/21 @ChicagoFed (in-person), organized by Ralf Meisenzahl, @rkoijen, @motoyogo. Submit by email to [email protected] (deadline 2/15). We welcome papers on insurers, pension funds, mutual funds, ETFs.

1/8 This is a great discussion, so I shall continue. Second round answer to @IvanWerning. I like very much the Werning-Lorenzoni framework. https://t.co/HA0EA5drYq One of its merits is indeed to show that thinking in terms of distributional conflict is totally mainstream.