Lets put this into context (numbers for Nifty).

After a great rally into closing yesterday, one might think, why not short Nifty puts with delta hedged for further vol compression on Friday open and you will mint millions!

Vanna, 2nd order option Greek - A Small 🧵

What is vanna? It is a 2nd order option Greek that can be interpreted in 2 ways:

Let f be the option price, σ be the volatility and S be the spot price. Then,

Vanna = ���2f/(∂S.∂σ) … 2nd order partial derivative

@SachaSucha@Nick_khandelwal Grind depends on roast level, darker roast has higher density with same grind setting as compared to light roast. Also let it rest at least 7 days to get all the real flavour.

AI-Powered Quant MCP Tool for Traders & Investors

✅ Optimize portfolios

✅ Compare stocks like INFY & NIFTY

✅ Analyze risk and stats

Just chat and get insights.

Video Demo Link : [https://t.co/k3ZMvcibIj]

🧵 on a few of the examples 1/n

@p_sharma8202 I don’t think it matters if it is a 251 days or 365 days model unless we are looking at cross assets with different expiries.

My original idea was to have a ballpark number of required move, vanna would complicate things significantly, also Vanna ATM is zero.

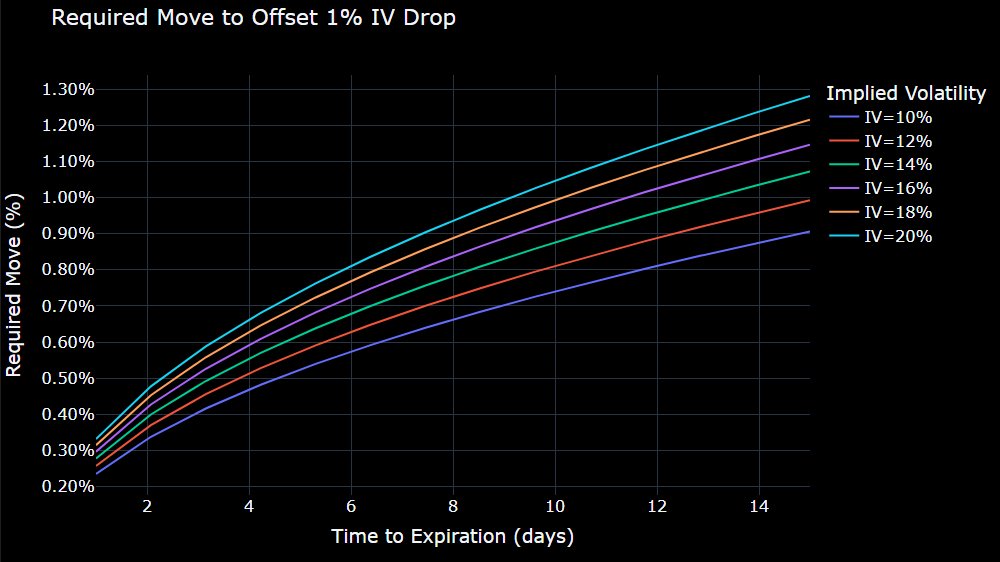

How much does the underlying need to move to offset a 1% drop in implied volatility (IV) when holding a delta-hedged, long gamma/vega position?

Gamma PnL ≈ ½ × Γ × (ΔS)²

Vega PnL ≈ Vega × Δσ

Set gamma PnL equal to vega PnL:

½ × Γ × (ΔS)² = Vega × Δσ

@Shivam_Pardesh Either you keep DTE constant at start of the day and track model intraday theta as Theta*hrs/24, or just recompute IV with reducing dte, this will bake in the IV changes along with theta.

Re-arrange and solve for percentage move ΔS/S when Δσ = 1%:

ΔS/S = √(0.02*Vega / Γ*S²)

This can be simplified further for ATM, where:

Vega ≈ S × √T × ϕ(d1)

Γ ≈ ϕ(d1) / (S × σ × √t)

So, breakeven move to cover 1% drop in IV for delta neutral ATM is

ΔS/S = √(0.02*σ*t)