starting with Wallet v0.0.7, all DAO managers will be able to take positions on other DAOs in https://t.co/EQqciErKVb, as requested by many creators

will this create a financial crisis due to DAO-over-indexing? probably. but we believe in the freedom to choose @daosdotfun

The power of a good BD isn’t to plan grand strategies

It’s to be just a text away from anyone important in the space

Strong network = shit gets done faster than competitors

Five years ago, before the launch of Uniswap v1, I deployed a token called HayCoin to use for testing. This was back when gas was so cheap that mainnet could be used as as a testnet. After the launch of v1, I created a small test liquidity pool with a tiny fraction of the total supply and left the remainder in my wallet. I also used it to test the migration contract from Uniswap v1 to v2.

Over the years, a few people have noticed it and bought it as a joke/for the novelty of it.

Was extremely surprised to see people buying and selling significant dollar amounts this past week, treating it like a memecoin. Crypto can be weird sometimes.

Ultimately, I’m uncomfortable owning almost the entire supply (~99.99%) of a token that people are memeing and speculating on, so I decided to burn the full amount in my wallet (”valued” at an absurd ~$650b).

To be extremely clear, I will have no future involvement, have burned all the HAY in my wallet, and think speculating on it is silly. Also prefer a new logo that is not my PFP - ultimately if my photo is used in this way I may consider image takedowns.

Is @LiquityProtocol v2 Solving the Stablecoin Trilemma through Delta Neutrality?

This 🧵 will cover the key concepts of v2 which enables a decentralized reserve-backed, delta-neutral hedged stablecoin.

TLDR:

• Abandon CDP and adopt reserve backing mechanism with 1:1 minting

• Launch in 2024 and will be independent product from v1

• Key ideas of V2: Dynamic Leverage Principal-Protected Positions (PPP)

Disclaimer: The diagrams and information presented below have been pieced together with limited documentation, Discord convos & @robert_lauko's talk. Will write another thread once official documentation is released!

Achieving Delta Neutrality in Reserves

As V2 transitions away from the over-collateralized CDP model of V1, the reserves, which composes of volatile assets (ETH/stETH) will be delta-neutral hedged.

• Today’s delta-neutral hedging relies on stablecoin protocol transferring all of its collateral positions’ upside/downside to third-party through selling leveraged long positions

• Leverage here is essential because the volume of capital committed to longing collateral ETH cannot always equal or be more than protocol’s total collateral

• However, leverage also presents very high risk to third-parties because downside is unlimited. There are limited number of investors ready to take on such risk, which limits protocol’s scalability

But what if the downside risk could be limited… or null? And what if upside could still be unlimited? Here is where Liquity steps in with their two innovations in Liquity V2:

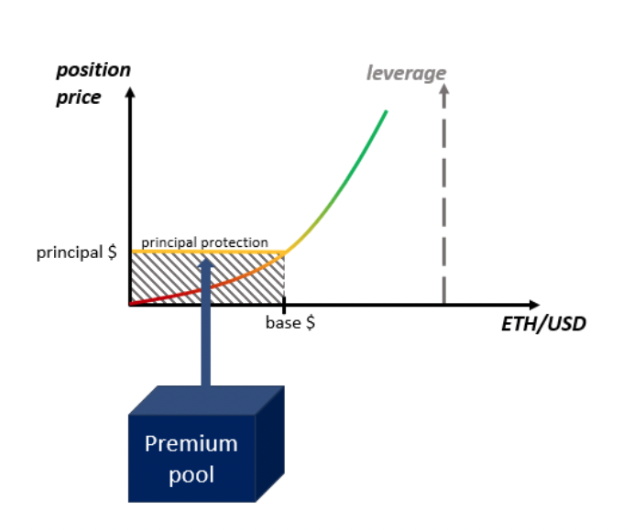

1️⃣ Dynamic Leverage

Refer to diagram #1 in the tweet

Imagine an isolated scenario where ETH price backing the stablecoin is relatively stable and is expected to remain around base $.

At base $, base V worth of capital is committed to leveraged longing ETH. (Total collateral / base V) provides base x leverage for each leveraged long position.

Then imagine that collateral can be redistributed among positions based on the changes in V, so leverage becomes dynamic (and inversely proportional to V capital committed to leveraged longing ETH)

In this scenario:

• A deviation down from the base price would incentivize more investors to commit more capital (V) to leverage long ETH

• As V deviates up from base V, (total collateral / V) decreases which means that leverage goes down

• Essentially, people rush into leveraged buy ETH low and dilute the volume of leveraging asset available to each individual

And when ETH rises:

• Investors begin exercising their positions, reducing V committed to leveraged longing ETH and increasing the leverage for those that still hold

Thus, dynamic leverage is achieved. Moreover, this kind of dynamic leverage is appealing from an investor's perspective because their expectable downside would always be lower than upside.

2️⃣ Principal Protection:

Refer to diagram #2 in the tweet

Principal protection is a tool that lets investors in Liquity v2 ETH leverage long positions to hedge all of the downside risk with a fee called “premium”.

Here is how it works:

• Firstly, in Liquity v2, a position's upside is unlimited, while the downside is limited to the position's principal. With dynamic leverage, it is only possible to lose roughly the amount one has invested.

• With a defined and limited downside, Liquity v2 can now afford to compensate every investor for any loss incurred by their position. To achieve this, investors are required to pay a premium, an additional amount above the principal, when opening a position.

• Premiums are pooled and once an investor attempts to liquidate a position with a market cost below its initial principal, an appropriate amount of funds is transferred from the premium pool into the position's principal to increase its market price. Thus, when said position eventually gets liquidated, its seller receives no less than the initial principal they committed. Moreover, there is no value leak from the protocol because instead of ending up in the seller's pocket, premium funds enter a long position’s principal.

Looking forward to reading the official documentation for v2 when it comes out. @robert_lauko@rick_liquity@bjnpck please feel free to add more color / clarity.