@CarsonTalkMoney Yes.

If a company is improving fundamentals yet its share price drops, AND your thesis hasn't changed, and you're considering selling, you shouldn't be holding individual stocks.

40% is the YTD return of our multibagger portfolio!!!

We'll soon do a rebalance, cutting some positions and adding some new ones.

We're looking to change 4-5 names in this portfolio, and our shortlist is filled with quality companies: $AAPL $MSFT $ASML $TSM $AMD $V $MA $COST $NFLX $AMD $CRM $KO $ADBE $BKNG $PLTR to name a few.

Would you add any to the shortlist? What are some stocks that you think will outperform in 2025?

In January 2024 I started the multibagger portfolio with 10 holdings and $10000 spread evenly between them.

In January 2025, I changed some of the names, but still ended up holding 10 companies.

I made no changes to it in 2026.

That portfolio is now up 2.5x in 2.5 years.

@la3ar0v@olaotantc@jack@blocks Well actually since 2023 operating and net income have increased, with total revenue largely flat. The stock price has also been pretty flat since 2023. The OP shows a 5 year time-frame, and suggests the company is struggling, when at worst it's flat, and at best profits are up

@olaotantc@jack@blocks The stock price and fundamental performance sometimes don't align. Just because the price is down doesn't mean the company is struggling or isn't growing.

@KowalBryan Exactly. I won't spend time to replicate a CRM system even if an agent can take me 90% of the way. I will use the agent to quickly integrate Salesforce's solution faster though.

Coding agents can now replicate 80% of existing SaaS functionality for a fraction of the cost. That doesn't mean companies will suddenly stop using $WDAY or $NOW or $CRM just because they can build the functionality in-house.

If anything, it just means lower cost for everyone involved.

I don't want to build, maintain, debug, add features, or have dedicated programmers for my in-house solution. I want the convenience. The value these major SaaS businesses bring isn't the code that they write, but the whole package.

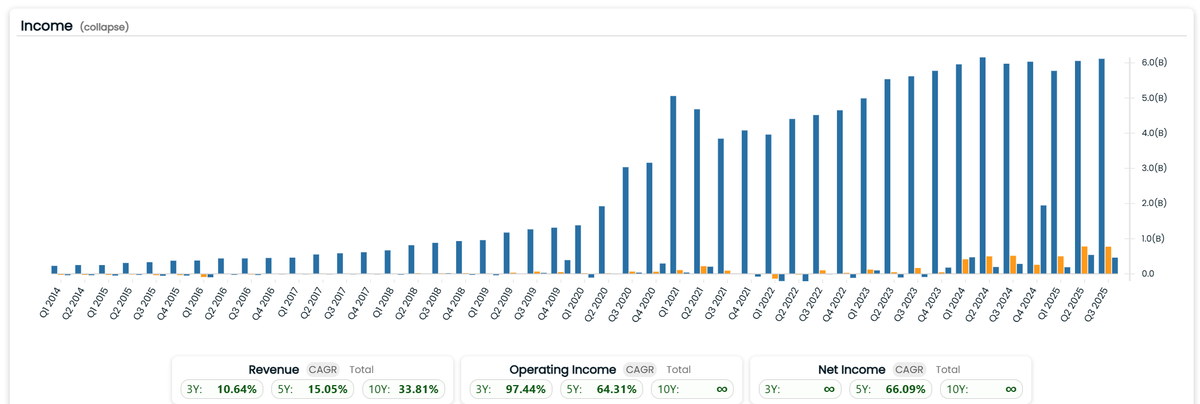

@DeepValueStonks Solid balance sheet, cash & st investments cover all liabilities 2x.

Consistent revenue & operating income growth (net income is skewed)

Growing number of users.

One fundamental risk I see is stock-based comp larger than what I like.

@mply_cap There were a lot of us that though the value was closer to $300 back in April, we were just given a discount.

The market is efficient. In the long-term.

$DUOL is finally in value territory. I liked the company before, but it was always too expensive for my taste. Starting position incoming.

✅Good gross margin & capital returns

✅Consistent growth (both in financials and active users)

✅Expected to grow top line 20% CAGR