Trump appears totally out of his depth in managing the Gulf crisis. DJT typically lies & bullshits his way thru life but the Gulf crisis & the war in Ukraine, exposes the limits to DJT’s approach. Eventually depth, intellect & strategy are needed. He has none

@ChrisB_IG That crunch point is surely when the northern hemisphere enters into heating season and then its Oil & Gas prices surging; the latter has been compressed so far by demand destruction but can’t go on forever.

@ChrisB_IG The only way this gets resolved is a non-linear reaction. Iran knows duration is its most effective tool, Trump needs to combat with either escalation or capitulation… this middle ground is perfect for Tehran.

This article pretty much covers the push back we’ve been receiving on our ECB call, ranging from growth to political blocking and Strait reopening hopes.

There are still dovish views that can be flushed away by Lagarde and the ECB’s projections Thursday. https://t.co/Tp0dq7EC1c

This is something people pointing to China's demographic decline often forget: for the next few years - at least until the late 2030s (if not early 2040s) - the number of people entering the workforce in China is set to INCREASE, not decrease.

For instance do you know which years recorded the highest birth rates in China in the 21st century? It was, in order, 2012 (14.57 births per thousand), 2014 (13.83) and 2016 (13.57). (src: https://t.co/cTotmhsxLj)

This results in the fact that, as you can see in the age pyramid below 👇, the 10-14 age cohort (kids born in 2012-2016) is actually **larger** than the 3 cohorts preceding it.

2016 kids - for instance - will reach 18 in 2034, and those studying at university (the majority of them) will reach the workforce at the very end of the 2030s, and the early 2040s.

The only cohort that's really dramatically shrunk compared to others is the 0-4 one, meaning China will really only start to have significant significant drops in workforce entrants in the late 2040s.

@ClausVistesen Very interesting and well written piece! Saw the other day that birth rates are diverging in the US but the other way around, however. Keen to get your view on that!

You can keep updated on our inflation and central bank tracking either through our Substack (https://t.co/sGEx9bcBZ8) or via our App, where you will have access to broader economic research (https://t.co/sxXIEmqgv0)

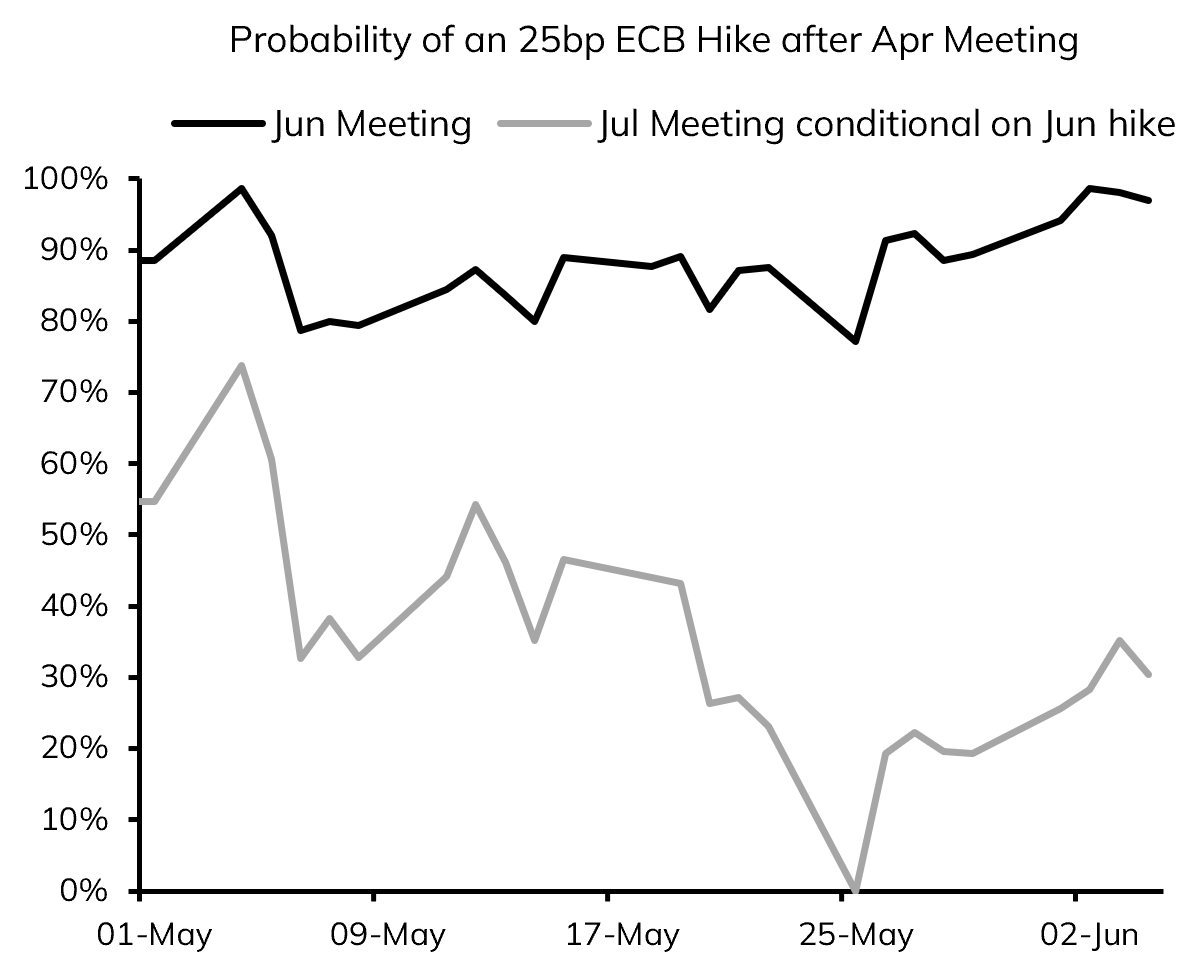

In the aftermath of the shock, we were early in calling for the commencement of rate hikes, beginning in Jun for the ECB - after the pullback in oil prices allowed the ECB to "skip" an Apr hike - Jul for the BoE, and Sep for the Fed.

Markets are now converging on these calls.

Markets are turning increasingly hawkish on central banks, as we have been arguing. Pricing of back-to-back ECB hikes has increased, from 0% last week, to 30%. Meanwhile, that of a Sep Fed hike, our modal view, is on the rise, now at 25%. We think both still possess upside.

CHART OF THE DAY: Perhaps the most important story in global markets / geopolitics right now.

China's oil imports plunged to ~6.6m b/d in May, according to @Vortexa data, down ~38% vs 2025 average (or ~4m b/d).

I wrote this @Opinion column in early May: https://t.co/XK71uh81m1

A 2nd FOMC voter—Dallas's Lorie Logan—indicates rate hikes "this year" may be warranted

"I am increasingly concerned that higher interest rates could be necessary later this year to fully restore price stability...."

@samueltombs@KevRGordon Sure, in isolation one-month indications from JOLTs is always subject to a lot of noise, but we're also seeing a pick-up in sectoral payrolls on a trend basis - seems like the AI disruption fears were overblown.

EZ May inflation showed Core - which is a better reflection of the inflation environment given fiscal offsets for energy in Ger, Spain, Italy etc - rising from 2.2% to nearly 2.6% y/y.

This brings the Q2 tracking up to 2.4%, i.e. above the ECB's Mar "baseline" and "adverse"

In this light, understandable that the Governing Council have become more vocal in supporting a 25bp hike - in line with our views since mid-Mar. A 50bp looks off the cards at this point due to Brent <$100 and inflation expectations stabilising for now.