The financial system will eventually converge on a hyperfinancial singularity — one in which anything that can be financialized will be, driven by zero overhead coordination costs enabled by universal on-demand programmable cryptoeconomic trust.

3Jane has executed the first of several credit facilities to scale U.S. fintech lenders, starting with a $10M warehouse line giving LendSwift a cryptonative balance sheet to grow its consumer installment loan product that thousands of Americans already use.

LendSwift keeps doing what it does best: customer acquistion, underwriting, origination, & servicing. 3Jane provides structured debt financing behind it, collapsing the multi-year bank warehouse -> forward-flow -> asset-backed securitization gauntlet into a single pooled, revolving conduit.

Suppliers mint USD3/sUSD3 on Ethereum, capital is lent to LendSwift to fund end-borrowers, newly originated consumer receivables are pledged into a bankruptcy-remote SPV to collateralize the facility with the originator retaining first-loss equity, loans are repaid through borrower cash flows swept into a DACA-controlled account, & yield is distributed back via report().

Cryptonatives now have access to the full raw economics of high-yield structured credit that historically accrued to funds and banks. No intermediary credit fund, no synthetic exposure, no tokenized claim on someone else's assets.

Native asset issuance will become the gold standard for funding fintech lenders within 3 years.

The entire structure is visible on 3Jane's backing page: https://t.co/3T1DfLMbWE

3Jane has executed a $10M senior warehouse facility with LendSwift, a U.S. fintech consumer lender, to scale its loan portfolio

Funded by USD3/sUSD3 at a 15% coupon and secured by ~15,000 short-duration installment loans

Cryptonative capital now funds mainstream consumer credit

Crypto could really use a synthetic CDO on a megapool of 9,431 RBF loans to AI agent businesses run on @polsia, with maybe endogenous collateral & a cheeky CDP stable integration right now.

Structured credit changed your life more than Michael Jordan, the iPod, & Youtube put together by shaving 200bps off your mortgage.

ABS, CDOs, synthetics are complex forms of financial engineering, and we believe they are the most fertile breeding ground for the next era of DeFi innovation.

Learn about the risks below.

Structured financing for fintech lenders (ABF) is a $100B+ asset class with virtually no history of being exported into crypto markets, despite consistently generating 10%+ returns.

Releasing a deeper analysis ahead of public launch:

➝ ELI5 warehouse loans & forward-flows

➝ Where the yield comes from

➝ Structured credit risk profile & loss distribution

Full post below.

The quality of The Economist’s analysis - the supposed last bastion of ruthless empiricism - has dropped off a cliff over the past year. A once-sharp knife, devastatingly blunted . End of an era, @TheEconomist.

Index funds, ETFs, interest rate/credit default/currency swaps, structured securitizations, junk bonds, Bitcoin, and Ethereum were all invented in the past 50 years, more than 3,000+ years after Hammurabi’s Code.

Barring civilizational collapse, at the current rate of financial innovation, many of the financial primitives that dominate 100 years from now probably have not been invented yet or will not exist in their current form-factor.

15/ This allows Klarna to significantly bring down their cost of capital as well as scale their portfolio orders of magnitude to +$B's. In reality, this only works when you've bundled >$100m's of loans together, not $10.

16/ As the lender scales they converge on the originate-to-distribute (OTD) model. It moves a lender from balance-sheet-heavy growth to capital-light platform economics that produces high margins and in turn high valuation multiples.

14/ Klarna invests time into having lawyers structure a tranched asset-backed securitization of burrito receivables, pay a rating agency to rate the tranches, and have bank sponsors pitch and sell the senior to insurance and pension funds at 5% coupon.

13/ Asset-backed securitization (ABS) // 3

Klarna is now several years in business, proved out their loan tape, scaled to $15 purchases and wants to engineer an even lower cost of capital for themselves to keep a larger spread.

12/ The credit fund might offer to buy $10 worth of future burrito purchases for $9.85. Private credit fund gets their double-digit IRR and Klarna scales their loan book without tying up equity, keeps an origination/servicing fee, and recycles capital. Extremely capital-efficient

11/ Forward-Flow // 2

Klarna has purchased $4 of loans, proved their performance, & wants to scale to $10 of burrito purchases without raising equity to fund the warehouse first-loss slice. Klarna gets approached by a credit fund for a forward flow whole-loan purchase.

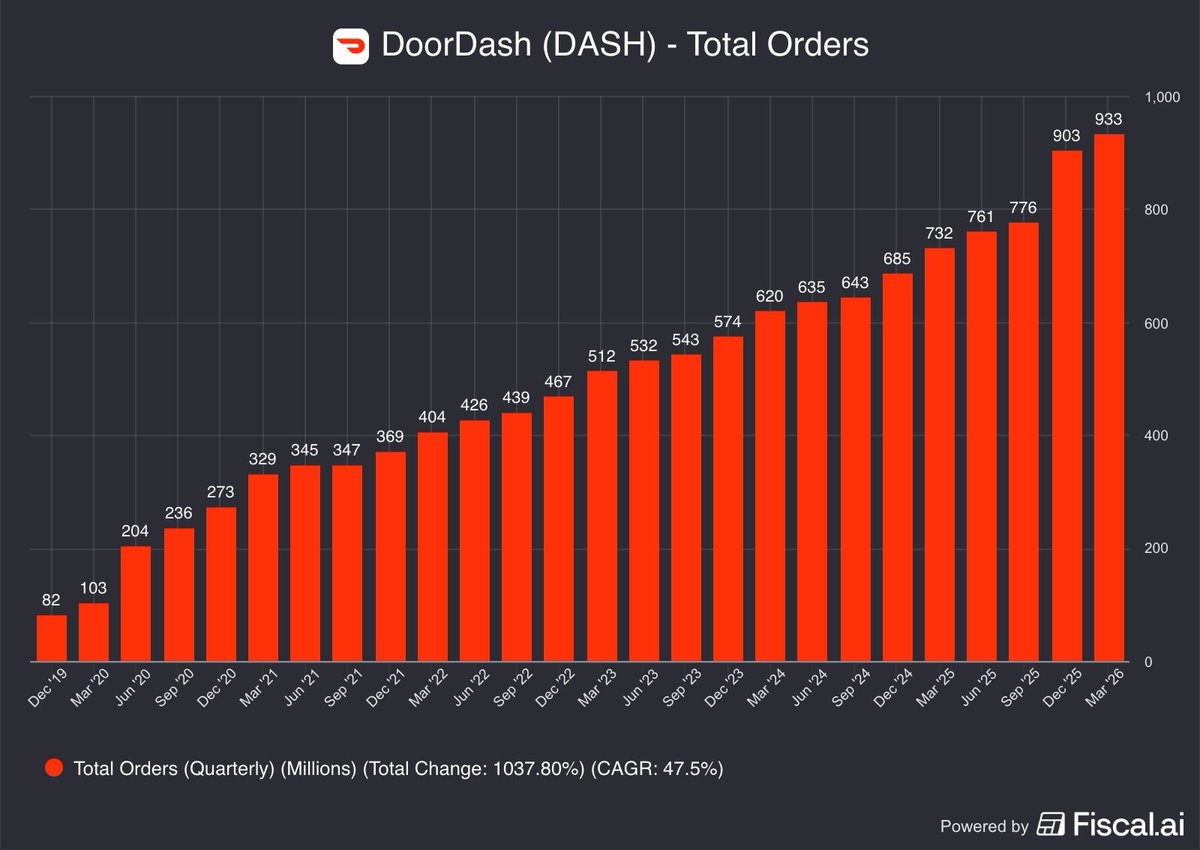

1/ DoorDash just reported 933M orders and $31.6B GOV in Q1.

In 2025 they added Klarna BNPL at checkout to drive growth. Most consumers still don't know who fronts the cash.

The capital markets rabbithole on how your burrito gets financed at 0% APR

10/ When Klarna started out in 2005, this was likely the only option they had given that it is the safest for the lenders/investors. Today, they still use this as a low-lift funding strategy to accumulate loans before reselling them in the broader ABS market (later).

9/ Instead, Klarna approaches the bank and borrows $3 with interest, funds the $4 burrito order, & pledges the receivables as collateral with the bank at a 75% advance rate, keeping a first loss slice. Bank gets their yield and Klarna scales their loan book w/o giving up equity.

8/ Warehouse // 1

Let's say Klarna wants to fund a $4 burrito order but only raised $1 in equity financing from VC A. So what do they do, do another round of diluting financing? No

7/ Instead, Klarna underwrites & originate loans, finances or sells them to outside investors, retains an origination fee, and repeats the process across millions of consumers.

In the U.S. they have a number of means at their disposal to fund their purchases.

6/ Generally fintech lenders try not to actually hold these loans on their own balance sheet. They are a platform business, not a balance sheet business.

5/ For a $100 order

Klarna pays DoorDash: $96.00

Consumer pays upfront: $25.00

Net day-0 capital out: $71.00

Then Klarna receives:

Day 14: $25.00

Day 28: $25.00

Day 42: $25.00

~105% gross effective APY before losses and costs