A new, leaner identity for https://t.co/Nfz0mvwjgz.

Fresh website, new challenges, and a never-ending desire to accelerate growth.

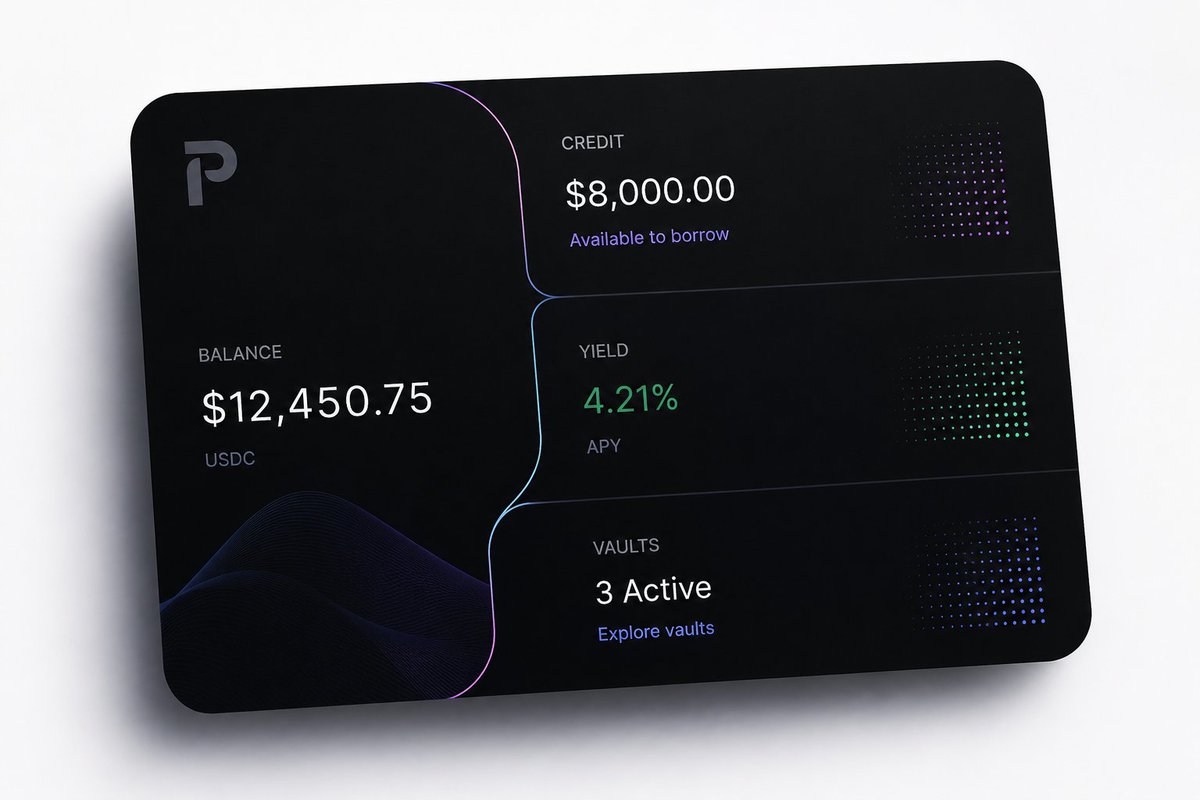

/Infra • AI primitives • Payments rails • Consumer/

Hi, I'm Ivan, @PulsarMoneyApp new CMO. Two weeks in, already cooking collabs and updates I can't wait to share.

Spent the last 6 months enjoying the work-life balance of fractional leadership for Web3 and AI projects. Then @Alex__Radu & @stefanabnc dm'ed me and said they needed me to build the story around a crypto card the whole world would want to know about.

When I thought I was out, they pulled me back in lol. Feels very good to be back, ct!

Clicked with the team instantly. The product is super ambitious. Partners have been warm everywhere we've shown up.

Less football and sleep in the coming weeks I guess, more coffee and stories worth telling.

How many crypto cards is enough? At Pulsar, we think that one should be enough :) tell me about yours

Let's gooooo

it was a real pleasure presenting @PulsarMoneyApp at La Maison PSG hub in New York

PSG is much more than one of Europe’s best teams: it’s a community, a fanbase, a network of hubs, flagship spaces, initiatives, tech labs & ventures and much more

Pulsar is built around communities, making money more efficient and fun. absolutely loved the energy and see some great intersections here for sure!

thanks @helgosson and @jessiexiao_eth for the opportunity!

We back teams that build strong payment infrastructure.

Today @xMoney_com became the first @Mastercard issuer worldwide to launch Payment Passkey.

Tokenized payments with biometric auth at checkout, reducing checkout drop rate for merchants by 50%. 👏

A global first for xMoney 🚀

We are proud to become the first @Mastercard issuer in the world to launch Mastercard Payment Passkey, the next-generation authentication solution for tokenized online payments.

Combined with Click to Pay, already available through xMoney, we're helping set a new standard for secure, seamless online checkout.

✅ Biometric authentication

✅ Faster payment confirmation

✅ Reduced fraud risk

✅ Less friction at checkout

A huge thank you to Mastercard for partnering with us on this milestone.

does the behavior survive when rewards end?

here's the only question that matters when you put gamification mechanics into a money app: does the behavior survive when the reward is removed?

run that test on most reward-led fintech and almost everything fails. the points, the cashback chase, the referral bonus, the spin-to-win. the behavior dies the same day, because people weren't saving or spending smarter. they were collecting a payout

web3 is a live experiment in what happens when you reward everything. quests, points, leaderboards, token drops. and it's the same movie every time: if the underlying behavior has no substance, the conversion never becomes valuable long-term

there were numerous eras of this in the industry:

- DeFi summer, crazy yields and liquidity rewards

- chain airdrops and liquidity hijacks

- SocialFi and yapping

- points and quest farming

it's fascinating how this market evolved, because there were also great examples of rewards done right. every time it worked long-term, there was sustainable growth behind it and a real business underneath

one of the best examples from DeFi summer is @aave. the yields and rewards were connected to a sound business model, a real revenue model, and smart economics. they did not just create temporary activity. they taught behavior and helped create an industry

Pulsar started with a B2B vertical and one of the service lines was loyalty infrastructure for banks, festivals, neobanks and web3 projects. the team ran infrastructure behind many companies and different economic models. that is where you learn the real lesson: whenever you put rewards or loyalty infrastructure behind a product, it has to sit behind a business model and a revenue stream. otherwise, it is very hard for it to be successful long-term

so the version we want to build further has to sit on real product value. the problem is that trying anything new takes effort, and people resist change even when it's good for them

that's all the gamified layer is for: getting someone over that first bump, long enough to feel the value for themselves. the game gets them in the door; the value keeps them there. in doing so, you end up with people who are better with money than the day they signed up

that's what drives real product growth

i'm really curious to learn more about this, and I’d be glad to put down a full article on the lessons from what we built, what we saw, some of the crazy stories behind it, and what we are working on now as a new generation of loyalty infrastructure

but my ask is simpler: what do you think is the most important part of rewards and loyalty in fintech?

what are you most excited to see?

and what would you actually want inside your money app at the intersection of rewards, behavior, and fintech?

The next step for stablecoins is accessibility.

With WCP, Pulsar users will be able to spend directly from their Pulsar account, across wallets and merchants worldwide.

A fintech experience, abstracting the settlement through @privy_io & @WalletConnect.

really enjoyed this article from @sserrano44 and the reactions & perspectives around it

my take is that this exact opportunity, smashing fees and making UX better, is fueling the current consumer fintech app cycle

I have been fascinated by onchain FX because it feels like one of the major use cases for stablecoins. not because it makes FX a little cheaper, but because it changes what has to exist for money to move between currencies and opening up some interesting new business models

in the old model, every corridor is an operating business. BRL to ARS means bank relationships, prefunded accounts, payout partners, compliance, cutoff times and liquidity on both sides. add another corridor and you rebuild the machine again

onchain, and inside this new fintech wave, the scheme is different. you operate access into each currency, and the FX leg in the middle can clear through a market. quote, execution and settlement collapse into one swap

liquidity for non-USD stablecoins is still a constraint, and adoption even more so. local currency pools are thin today. but once local stablecoins get real depth, the product surface changes

this is also why i find @circle, @arc and StableFX interesting. local stables do not weaken USDC. they probably distribute it. most liquidity still routes through dollars, so BRL, ARS, MXN, COP, EUR and other local stables become the front door, while USD stablecoins become the liquidity layer behind them

then the user experience gets interesting. local currency in. global liquidity behind it. local spending and payout on the other side

the fintech layer is what makes that liquidity useful every day: cards, payroll, merchant settlement, PSP routing, bank connections, neobanks, and all the infrastructure that hides the fragmentation

in short, the fintech mania right now is the cycle connecting stablecoin infrastructure to actual use cases

The agentic economy will grow through products that everyday consumers can actually use.

@fastxyz has been quietly building a powerful stack, and Fast Shop feels like the first glimpse of what it can unlock.

Underneath the simple shopping experience is infrastructure for payments, interoperability, and AI-native work.

Looking forward to seeing the rest come online. 👏

Across 2 days in Paris, @proofoftalk brings together:

→ 60+ partners

→ 2,500 attendees

→ 200+ journalists

From partner coordination to attendee flows and on-site operations, Rhuna helps power the infrastructure behind one of Europe’s leading Web3 events.

This week, the Pulsar Money team is heading to several events across EU & US.

From Paris to New York, we’ll be on the ground talking about what comes next for money movement, stablecoins, and the infra needed to make the next generation of fintech usable in everyday life.

new generation of fintech

the Revolut & Wise generation was incredible. they disrupted a conservative market ruled by dinosaurs by making money movement feel natural. better onboarding, better FX, cleaner cards, faster notifications, a nicer app on top of a very old stack

but the next wave is different because the stack itself has completely changed:

→ stablecoins make settlement global and 24/7

→ self-custody lets the account belong to the user instead of the institution

→ bank rails and cards can sit at the edges of a stablecoin-native balance

→ DeFi protocols can sit underneath the account for swaps, yield, trading and credit

→ agents can start acting on clear rules and limits instead of leaving the user to manually move money between 5 products

the old fintech product was: take the bank, make it mobile

the new fintech product is: rebuild the financial account around money that moves, earns, settles and can be routed

the line I keep coming back to is:

→ everyone earns on your money. except you

banks earn on idle balances. card networks earn on every swipe. FX providers earn on every border. platforms earn on your deposits, transactions and data. the user is usually the last person to benefit from their own financial activity

that's why the next generation of fintech that wins will be the one that inverts that

your money should work for you first. it should earn while it waits, move globally when needed, stay under your control, and connect to the best financial infrastructure without forcing you to become a DeFi power user

Pulsar is our view on the consumer side of this

→ a stablecoin-native money app where your balance can spend, send, earn and eventually route itself more intelligently, while still feeling like a normal everyday app

and it all comes down to executing on that vision with surgical precision, because make no mistake, average consumers will accept nothing less

one thing after watching stablecoin cards lately

in the US, credit is the default. people "put it on the card" and the card almost always means credit. rewards, points, credit score, the whole social contract of how you spend lives there.

in most of europe and a lot of asia, the opposite. the card is debit. you spend what you have. credit is a separate product you opt into.

and i think this is what's actually shaping stablecoin cards right now

because the first wave of stablecoin cards is basically the european version. debit-style, spend crypto through a card. you swipe, your balance drops, you sold an asset to buy a coffee. useful, but it's the smaller version of the product

the next wave is the american version. credit attached to the account. you don't sell when you spend, you borrow against what you hold.

onchain, that architecture can actually be cleaner than the legacy version

collateral is liquid, transparent, programmable and composable. credit lines can sit behind the user experience, while settlement still happens in the format merchants already understand

this is why infra like @sprinter_ux is interesting

one credit line, collateral across chains, USDC drawn to a receiver address. for a card program, that receiver can simply be the settlement layer. user taps, USDC settles, the credit line sits behind the experience, and the user never has to think about chains

@Morpho matters for the same reason

not as the card layer, but as part of the credit and yield layer underneath the account. if stablecoin apps become real financial accounts, they need lending markets, curated vaults and idle-balance yield underneath them

so the cards are the interface people already understand, while the account behind the card is the actual product.

the goal is to make that feel normal to use, just like traditional credit accounts.

of course, still real work to do on risk, LTVs, liquidations, refunds, tax, compliance, chargebacks, but the direction is pretty clear;

and that's a big part of what we’re building at @PulsarMoneyApp

looking deeply in this space so let me know if you have any other ideas and views on these infra protocols we should take a close look at

Neobanks changed the consumer experience.

Now the next step is how all the pieces come together: payments, stablecoins, intelligent money movement, and financial products that can operate without adding complexity for the user.

Join the conversation next week.

Neobanks & payments infra are becoming one of the most important conversations in fintech.

Next Tuesday, we’re hosting an X Space with @xMoney_com to talk about what next-gen of financial products need to get right.

Set a reminder 👇

https://t.co/5CqbAkNGyh

Ready for Pulsar coffee meet-ups in the US?

This summer, we’ll be hosting open spaces to talk fintech, AI, and what’s next - with close friends and new ones. ☕️

delivering great products is no longer enough to build a moat

some takes from the Lovable coffee:

AI is decentralizing development and vibecoding will become insane during the next years. everyone becomes a builder. product quality is slowly becoming the standard, not the differentiator

the bigger moat increasingly becomes distribution and brand

- distribution through partnerships, integrations, ecosystems and real use cases

- brand through community, power users, culture and how people perceive and represent your company

one thing that impressed me about Lovable was the evolution of the company itself. they started as GPT Engineer. very technical positioning, builder-first, little focus on branding. then they made a strong pivot toward community, non-technical users and brand development

probably one of the best examples of how AI startups need to evolve now. AI lowers the barrier to building. brand and distribution decide who wins at scale. thanks @felixhhaas for the coffee meetup and chats