Honeywell spin-off: first day of trading yesterday for $HON $HONA with both tickers selling off into the close (higher pressure on RemainCo interestingly)

Implied creation values look interesting for both at current levels. While Aero is considered the premium asset, Automation's growing installed base + software monetisation strategy is under appreciated and may get the steeper re-rate overtime.

For anyone wanting to learn more (maybe too much!) about Copart, I put out an 85-page report on the business a couple years back

Speedwell Research members get access to that and several updates since.

https://t.co/jlBlliftnL

$CPRT now at around 20x FCF.

Jay Adair announced to be stepping back into the CEO role.

One of the most pristine balance sheets on the planet.

Now a good time to buy the stock?

Copart just announced that CEO Jeff Liaw is stepping down.

Former CEO Jay Adair is stepping back into the role.

Adair served as CEO from 2010 to 2022. During that time, Copart generated a 1,378% total return.

$CPRT

Really great AlphaSense expert call interview with a former VP of Geico. He touches on the dynamics between $CPRT and IAA ( $RBA)

He sees that IAA has stepped up their game and is now picking up and selling salvaged cars at the same rate Copart is.

He also thinks this could (on margin) result in some carriers moving to IAA to balance the dynamic between Copart and IAA.

Basically no insurance company wants a monopoly and so they try to balance where the volumes go between the two. This historically has been offset by Copart saving the insurers more money--so they on margin preferenced Copart.

It is important to note though that this isn't actually why we saw the volume drop off over the past 2 quarters. There hasn't been any big carrier switches or volume changes (this is just a future risk).

Their recent headwinds have been driven by under insured and non insured drivers, who when they crash, the insurance company doesn't collect the car.

The expert notes that it is very rare (never happened before) for Americans to have premiums increase 50% in a short period of time due to Covid, supply shortages (increases cost to repair and buy replacement cars), and inflation.

IAA getting better was always a risk (although one that I honestly didn't see happening in such a short period of time). Having said that, the volume/ market share shifts in the U.S. aren't likely to be that meaningful and contracts only come up for renewal every several years on a rolling basis.

The Geico executive didn't think Geico would move volumes away from Copart. (Copart is still very well run, it is just that their competitor seems to have caught up).

It is also worth remembering though that Copart is growing internationally in many markets where there is no real competitor. They don't need to take share (and weren't expected to) in the U.S. in order to grow.

I shared some key quotes from the interview in this thread. A special thank you to @AlphaSenseInc for insights.

(1/3)

Here’s a list of companies with more cash than liabilities you might want to take a look at:

Copart $CPRT is a compounding machine with a wide moat. Flipping cars is insanely profitable.

It holds 4x more cash than liabilities..

$CPRT is trading at historically cheap valuations.

- Duopoly market position

- 15% of market cap in cash

- First buybacks in years

- Owns Yards vs. Competitors leasing them

Last earnings report wasn't stellar, but in this article, I analyze whether that's an opportunity:

$CPRT Copart is one of the most quietly brilliant businesses of the last decade.

Free cash flow per share has compounded at +31% annually since 2016, a total increase of +1,330%. The stock followed: +551% over the same period.

The business model is great:

- Irreplaceable land network (250+ locations, 11 countries)

- ~33% net margins with zero debt

- $5.1B in cash earning interest while they wait

- Rising total-loss rates (now 22.8%) are a structural tailwind

However, the stock is now down ~39% from highs (not on business quality deteriorating, but on a cyclical dip in insurance volumes).

Modern cars are getting more expensive to repair (ADAS sensors, EV batteries, etc.). That means more totals. That means more volume for Copart.

Mr. Market occasionally offers you great businesses at fair prices. This might be one of those moments.

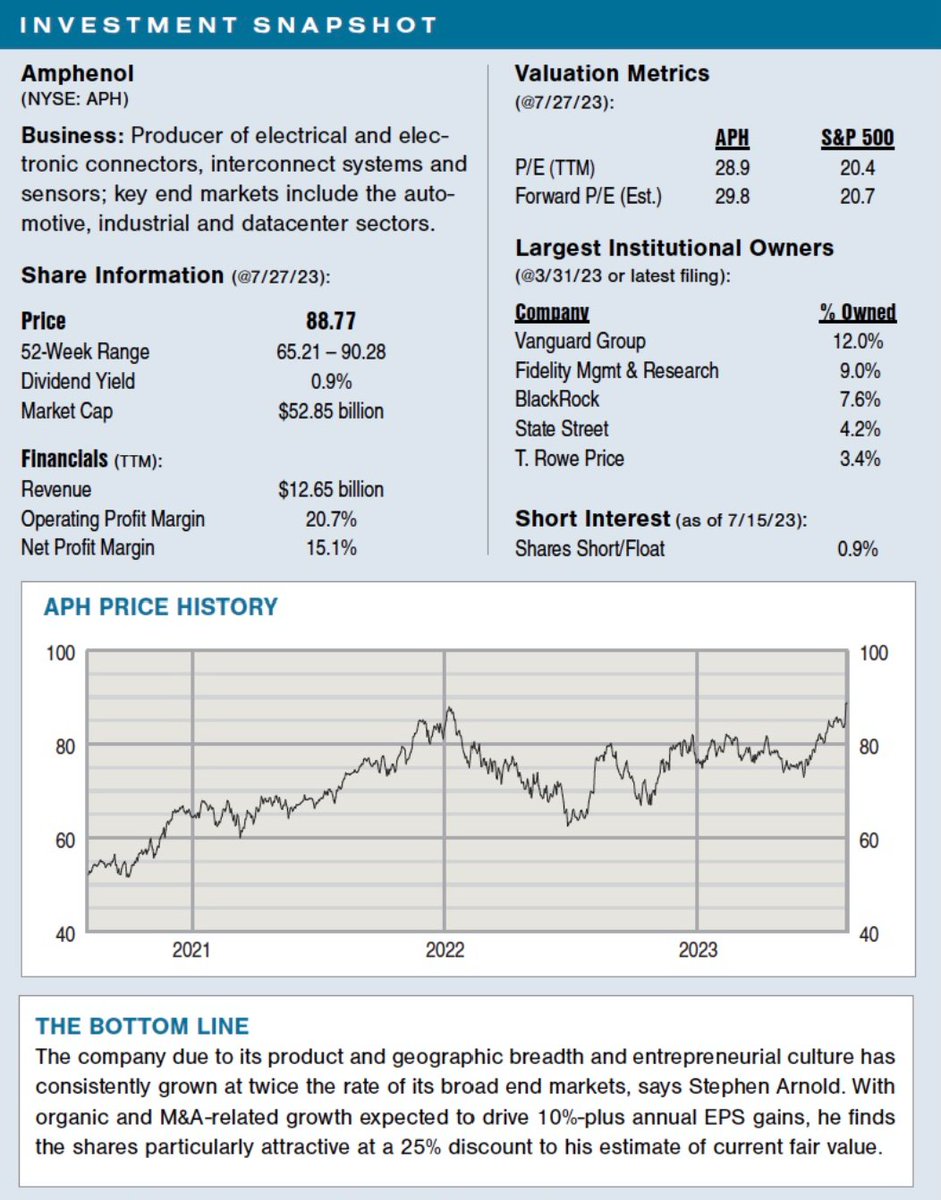

$APH - long thesis

• Earnings plowed back into organic & M&A investments

• Decentralized structure helps $APH grow above GDP rates & 2x peers

• Growth across markets positive (increasing content in cars, factory automation in industrials & cloud computing in data centers)

$APH - Amphenol (leading provider of high-tech interconnect, antenna & sensor solutions) is an under-the-radar great business

Here is the investment thesis in Barron's today

• $APH's recent dip presents a buying opportunity. Last week's DeepSeek sell off of data center exposed companies has created an attractive entry point ($APH tumbled 13% on the news).

• $APH boasts strong financials and consistent growth. $APH has a history of exceeding earnings expectations and consistent profitability. The company hasn’t seen a decline in profits since 2010 & rarely misses its quarterly earnings forecasts.

• Diversification across multiple sectors mitigates risk. Serving aerospace, mobile devices, & defense alongside data centers reduces reliance on any single market. This diversification also provides resilience against fluctuations in specific sectors.

• Strategic acquisitions fuel further expansion. $APH actively acquires, with the recent $COMM mobile networks acquisition expected to add significant revenue & expand market reach.

• A rebound in the EV market offers upside. Increased connector content in EVs positions $APH to benefit from a resurgence in this sector (whenever this happens).

• Exposure to $NVDA provides growth potential. $APH supplies connectivity products for $NVDA's GPUs (estimates are for AI-specific sales to reach over $1B this year).

• Positive growth projections remain despite recent AI concerns. Analysts predict strong revenue (13% annually through 2026) & earnings growth driven by continued demand, strategic acquisitions, & the potential for increased AI hardware demand.

• Valuation, while seemingly high, is justified by growth potential. $APH's PEG ratio is attractive, & the recent price drop makes it even more compelling. Per the article, "We can debate valuation, but as long as organic growth stays at/near these double-digit levels…shares will likely have support."

@lhamtil@yesandnotyes and @DevinLaSarre provide the beginning of the untold story of Amphenol $APH

They cover the founder Arthur J. Schmitt and the journey of the company from its beginning in 1932, through WWII, through multiple acquisitions, and several times being acquired by others.

For Part II, we'll be interviewing William Kerwin, a senior equity analyst at Morningstar who covers the IT supply chain, hardware, and semiconductor stocks.

Did Apple mention Amphenol?

Another reminder that Amphenol is likely one of the highest-quality businesses most investors have never heard of.

$AAPL $APH