Minor changes to the portfolio in April 2026.

Added to $META Meta, $MA Mastercard, $AMZN Amazon, $BN Brookfield, and $FICO FICO.

Only buys.

The portfolio is built around some of the world’s strongest, highest‑moat platforms, with a heavy tilt toward scalable, asset‑light, data and network effects businesses.

These companies benefit from immense economies of scale, proprietary infrastructure, pricing power, and data advantages that reinforce their moats as they grow. Their revenue bases skew toward recurring or highly repeat‑purchase models (cloud subscriptions, advertising, developer and enterprise contracts, etc.) with strong operating leverage, making incremental margins very attractive as utilization increases.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep equity research into my holdings (as well as other compounding machines) and highly relevant thematic trends shaping today's markets. Link here and in bio: https://t.co/u5CjOu8mrE

$GOOG

$META

$NVDA

$AMZN

$V

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

Minor changes to the portfolio in April 2026.

Added to $META Meta, $MA Mastercard, $AMZN Amazon, $BN Brookfield, and $FICO FICO.

Only buys.

The portfolio is built around some of the world’s strongest, highest‑moat platforms, with a heavy tilt toward scalable, asset‑light, data and network effects businesses.

These companies benefit from immense economies of scale, proprietary infrastructure, pricing power, and data advantages that reinforce their moats as they grow. Their revenue bases skew toward recurring or highly repeat‑purchase models (cloud subscriptions, advertising, developer and enterprise contracts, etc.) with strong operating leverage, making incremental margins very attractive as utilization increases.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep equity research into my holdings (as well as other compounding machines) and highly relevant thematic trends shaping today's markets. Link here and in bio: https://t.co/u5CjOu8mrE

$GOOG

$META

$NVDA

$AMZN

$V

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

Data center developer Switch is in talks to raise billions of dollars at a valuation of at least $50 billion, as it seeks to capitalize on soaring demand for the infrastructure needed to support artificial intelligence, according to people with knowledge of the deal.

Brookfield Asset Management, KKR and other private equity and institutional investors have been in talks to invest in the round, people familiar with the matter said. Their conversations are early and there is no guarantee they will lead to a deal. Terms of the funding round could still change and the discussions could still fall apart.

Source: The Information

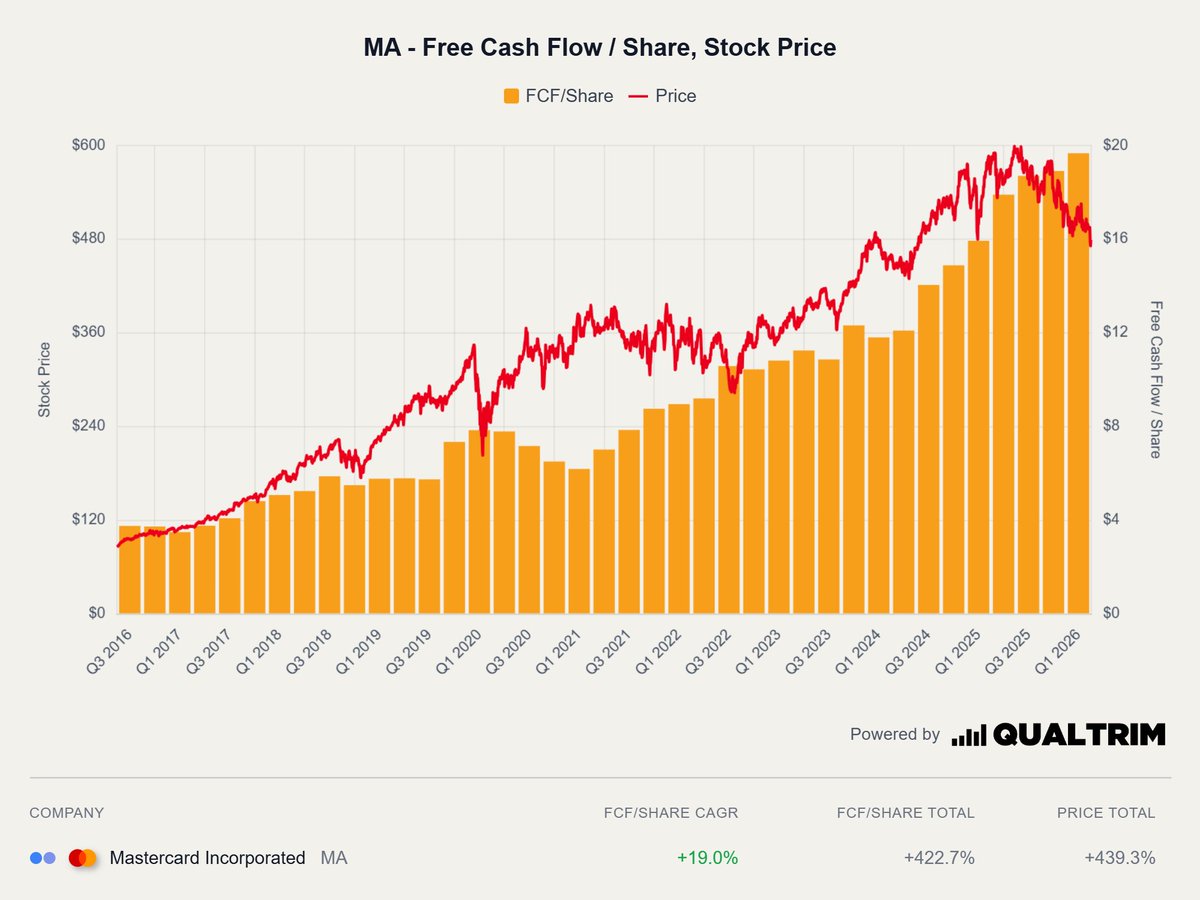

$MA Investing in high-quality companies is all about finding businesses with durable moats that protect them from competition and allow them to earn high returns on capital.

Like a toll bridge on a busy highway, these companies provide essential products or services, possess immense pricing power, and require very little cash to maintain their operations. This capital efficiency allows them to generate mountains of free cash flow, which management can then reinvest back into the business or use to buy back shares.

When you find an elite business capable of doing this year after year, you don't need to trade or timing the market...you simply buy, hold, and let the power of compounding build immense wealth over time.

Mastercard at a 4.18% FCF yield is very attractive.

I just published our latest deep dive on Amphenol $APH.

A boring compounder with exposure to some of the most important long-term trends in the market - data centers, space, robotics, and electrification - yet still trading at a very reasonable valuation.

Hope you enjoy the read. Link in the comments. ⬇⬇

Return on invested capital identifies the businesses that create value.

Owner earnings measures what owners actually receive.

The moat framework explains why some businesses sustain those returns for decades while competition erodes them for everyone else.

This is the third piece in the free foundational framework, and the answer to the question the ROIC piece raised.

Dropping tomorrow at 9am ET: https://t.co/BgpM5eGi47

Eighteen months ago, $APP AppLovin was the market’s cleanest expression of the AI-advertising trade: a 700% gain in 2024, a fortress margin profile, and a machine-learning auction engine that appeared to print money.

The narrative in 2026 has inverted. The stock round-tripped from an all-time high near $734 in December to a trough near $320 in early spring, then clawed back to $613.70 (yesterday's close) — all while reporting record results. This is no longer a momentum story; it is a “prove it” year.

What makes AppLovin unusual is that both sides of the debate are internally coherent. The bull case and the bear case each survive serious scrutiny, which is rare in ad-tech, where one side is usually arguing in bad faith.

The question this report answers: does the current price compensate an owner for the durability of the AXON moat — or is it paying a compounder multiple for a business whose compounding is unproven outside one mature vertical?

Read the full bull vs. bear report here: https://t.co/x9XYyFjhwH

$APP AppLovin is one of the cleanest tests of quality investing in the market right now.

The bull case is textbook compounding. AXON — its machine-learning ad engine — turned cheap mobile-game inventory into a performance network running ~84% EBITDA margins and converting most of it straight to cash. Now it's expanding into e-commerce and connected TV, with a public ad platform launching in 2026.

The bear case is a real fight, not a strawman. The data edge is rented on Apple and Google's rails, mobile gaming is mature, a securities class action and reported regulatory scrutiny hang over its data practices, and the e-commerce story is being extrapolated off a tiny base.

The crux: the market is conflating AXON's proven dominance in gaming with unproven durability outside it — and pricing the e-commerce option as if it's already de-risked at ~41x owner earnings.

A durable, AI-native ad tollbooth, or rented-land ad-tech at the wrong multiple? True quality investing means digging past the noise to verify the moat before paying for it. Our verdict: Watch.

Bull vs. Bear — full breakdown linked below. Available tomorrow at 8:30am ET.

https://t.co/m8oThBzF49

$APP AppLovin is one of the cleanest tests of quality investing in the market right now.

The bull case is textbook compounding. AXON — its machine-learning ad engine — turned cheap mobile-game inventory into a performance network running ~84% EBITDA margins and converting most of it straight to cash. Now it's expanding into e-commerce and connected TV, with a public ad platform launching in 2026.

The bear case is a real fight, not a strawman. The data edge is rented on Apple and Google's rails, mobile gaming is mature, a securities class action and reported regulatory scrutiny hang over its data practices, and the e-commerce story is being extrapolated off a tiny base.

The crux: the market is conflating AXON's proven dominance in gaming with unproven durability outside it — and pricing the e-commerce option as if it's already de-risked at ~41x owner earnings.

A durable, AI-native ad tollbooth, or rented-land ad-tech at the wrong multiple? True quality investing means digging past the noise to verify the moat before paying for it. Our verdict: Watch.

Bull vs. Bear — full breakdown linked below. Available tomorrow at 8:30am ET.

https://t.co/m8oThBzF49

Alphabet $GOOGL is reportedly considering an $80B equity raise to help fund its next phase of growth.

The proposed structure includes $30B in underwritten offerings, a $40B at-the-market program, and a $10B strategic investment from Berkshire Hathaway $BRK.

When a business has the combination of multiple expansion and earnings growth, you have two different factors multiplying each other.

This is exactly what we are going to see with $META going forward. At a stock price of around $608, the market is offering a dominant, accelerating franchise at a FRACTION of what it is worth.

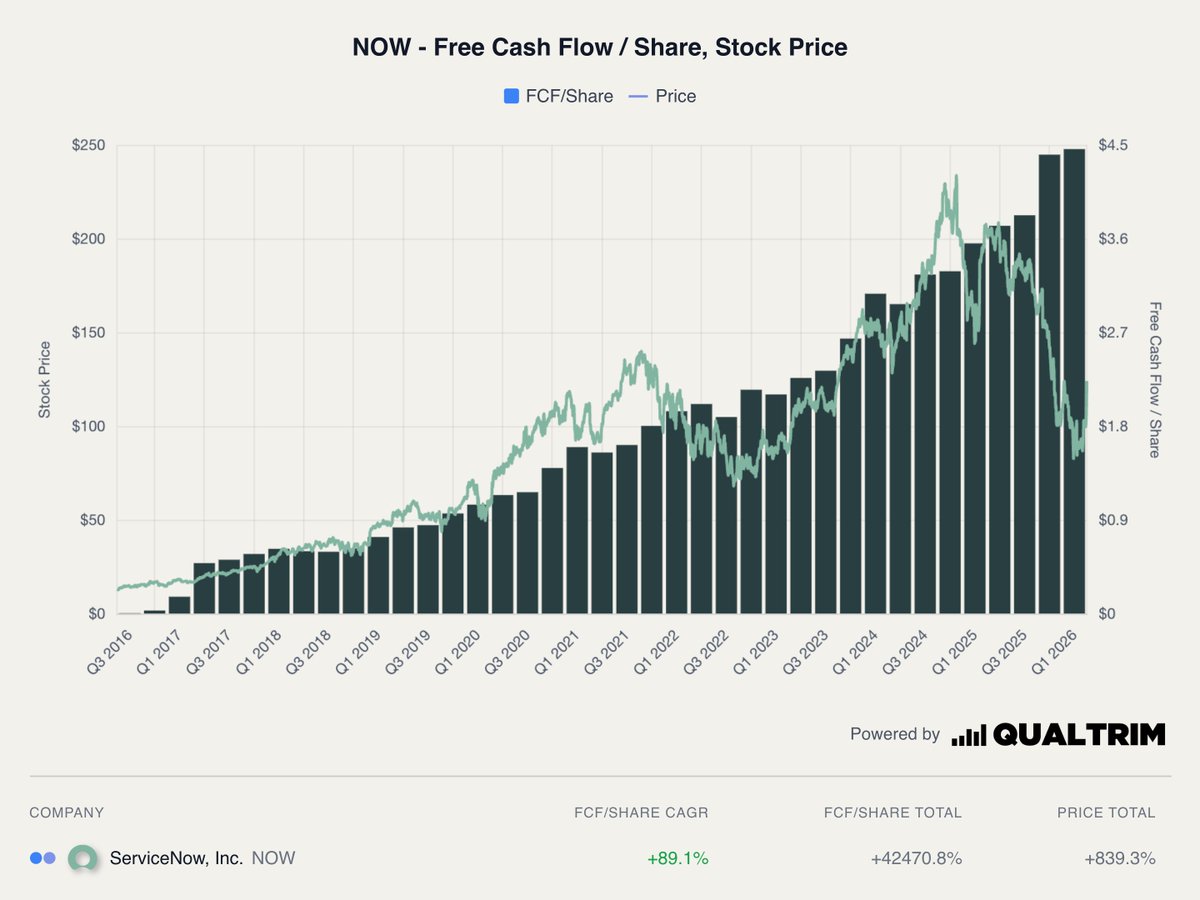

$NOW ServiceNow shares have staged a powerful turnaround, surging nearly 40% in May alone. This explosive move represents a dramatic reversal from earlier in the year when the stock tumbled over 40% due to panic selling across the software sector.

Looking at this through the lens of business fundamentals and competitive moats, the recent surge is driven by a profound shift in market sentiment. Investors are realizing that artificial intelligence is a powerful tailwind for ServiceNow, not an existential threat.

Deep-dive: https://t.co/sYSjVxB2IZ

$NOW ServiceNow has fallen roughly 60% from its high, now trading near $90. The selloff has been driven by fears that AI commoditizes workflow software and that enterprise IT budgets are softening. Consensus has shifted from "secular winner" to "structurally challenged" in under twelve months. Valuation has compressed materially.

The fundamentals tell a different story. FY2025 revenue grew 21%. Free cash flow reached $4.6 billion. Q1 2026 subscription revenue grew 22%. Remaining performance obligations stand at $27.7 billion, up 25%. This does not look like a business in decline.

Sunday special deep dive dropping at 10am ET: https://t.co/biNFbiqGJd

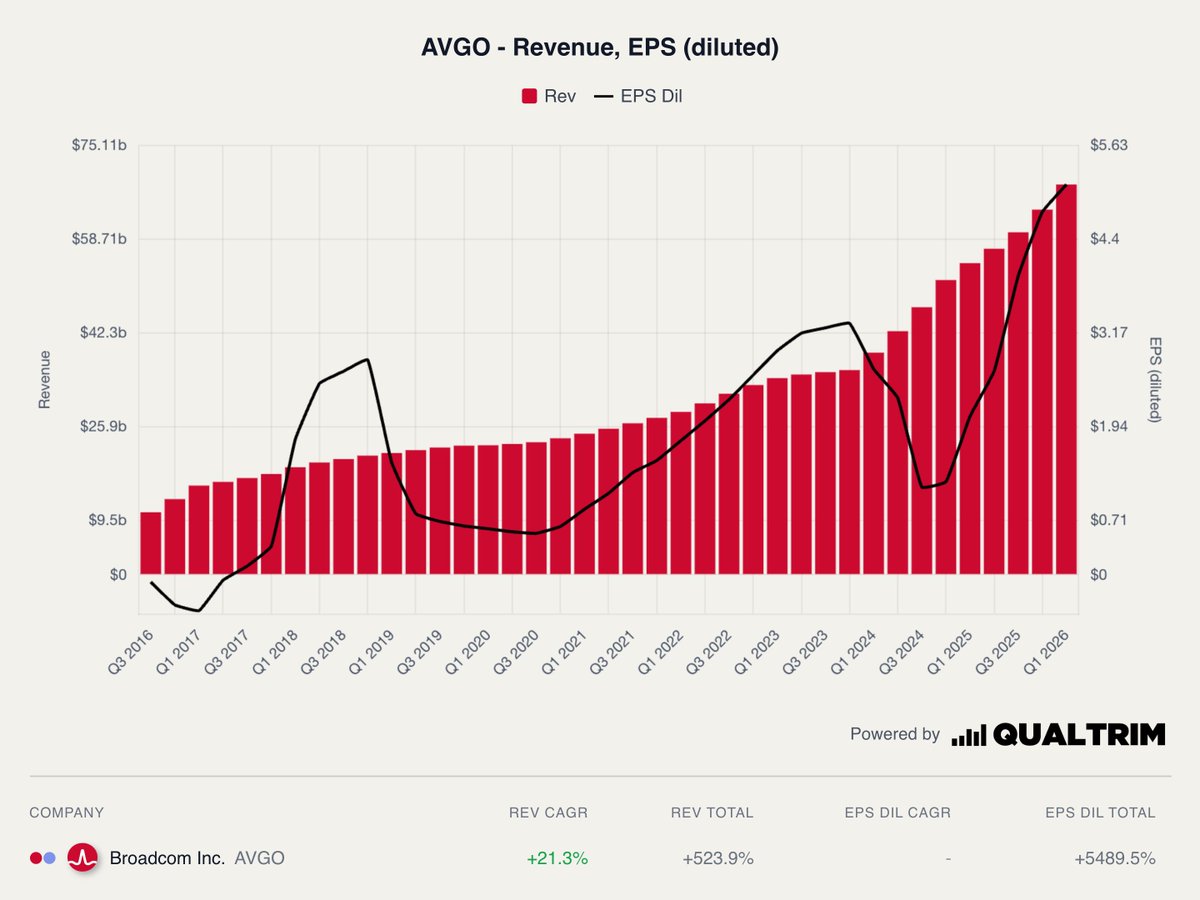

$AVGO When evaluating a business through the lens of long-term compounding, we look for a rare combination: a wide economic moat, an indispensable product, excellent capital allocation, and a long runway for growth.

Looking at Broadcom, it becomes clear that this is not your typical cyclical tech company. It has quietly engineered itself into becoming a quality toll road on the modern digital highway.

$GEV GE Vernova is a pure-play on electrification and grid resilience at exactly the right moment. With demand for power infrastructure accelerating, and margins improving, is this a compounder in the making? Interesting take below.

We just published our deep dive on GE Vernova $GEV.

Before anything else, GE Vernova is ultimately a survivor of the brutally cyclical gas turbine industry - now finally harvesting the rewards of the discipline and restructuring work done over the past decade.

The stock is up more than +800% since the spin-off. The question is: is there still room for upside?

We break it all down in our full investment thesis. Link in the comments. ⬇⬇

$V Visa and $MA Mastercard are two of the best businesses on the planet. They operate a global duopoly, taking a tiny slice of nearly every digital payment made worldwide. They don't take on credit risk, they have near-unbeatable competitive moats, and their profit margins are legendary.

For years, the only problem was their price tags. During the 2021 market bubble, investors bid them up to an expensive 50x to 60x free cash flow. At those prices, the stocks just didn't offer a good margin of safety (thought still amazing businesses).

But, fast forward to today. Thanks to a mix of market normalization and temporary headlines, valuations have compressed back down into the mid-to-high 20x P/FCF range.

The bottom line is simple: the underlying businesses are just as dominant as ever, but the stocks are at their most reasonable prices in nearly a decade. For long-term investors, this valuation reset is a rare opportunity to buy two elite compounding machines at a steep discount.

Which is better to own? Found out here: https://t.co/k1eqM0jJFi

$SPGI S&P Global looks like a highly attractive buying opportunity right now.

S&P Global is a world-class business with a massive competitive moat—companies will always need credit ratings and financial data.

While the business itself remains incredibly strong, the stock got a bit expensive in 2022 when investors bid it up. Since then, hype has cooled off, and the valuation has dropped back down to around 22x P/FCF.

Because you are now paying a remarkably fair price for a compounding machine that rarely goes on sale, the margin of safety is the best it has been in years.