Personal Finance at its core is simple:

1) Emergency Fund

2) Health & Term Insurance

3) Equity for compounding

4) Diversification across countries & assets.

After 10 years in financial journalism, I co-founded thefynprint. We give you:

1) A concierge service on financial questions like PF withdrawal, home loans, credit cards, global investing etc.

2) A WhatsApp community to discuss & share information

3) Webinars & meet-ups

4) Weekly digital magazine

Subscribe to thefynprint. It is only Rs 400 per month.

People think global = AI. Starting today, I'm going to write about my anti-AI global portfolio and why I hold each of my positions.

Starting with the largest: Berkshire Hathaway (17% allocation)

🏰 Berkshire Hathaway: what you're actually buying

Most people hold Berkshire as a market-beater - Buffett's legend. But on a rolling 10-year basis, its consistent outperformance of the S&P 500 ended around 2012. For over a decade it has roughly matched the index, not beaten it. If you own it expecting alpha, the data says you've been buying something else.

What you're actually buying: ballast. Berkshire is a cash-rich, insurance-anchored, low-beta collection of real businesses with near-zero direct AI exposure. Its value isn't that it outruns the market - it's that it holds up when the market doesn't. Lower volatility than the index, no dividend (tax-efficient for those who don't need income), and a balance sheet built to absorb shocks. It is the opposite of a high-conviction bet; it's the thing you own so the rest of the portfolio can take risk.

The cash pile is the most interesting signal. Berkshire sits on well over $300 in cash - not because it lacks ideas, but because Buffett can't find enough worth buying at current valuations. That is itself a statement: the most patient value investor alive is, in effect, saying prices are too high. Holding Berkshire is partly holding that judgment.

The risks:

→ The edge may be structurally gone. Private capital (Blackstone, Apollo) now competes for the distressed-asset and crisis financing deals that were once Berkshire's alone. The be greedy when others are fearful advantage is more crowded than it was.

→ The succession transition. Buffett has stepped back; Greg Abel runs it now. The market must decide what the business is worth without the founder - a re-rating risk in either direction.

→ The law of large numbers. At over a trillion dollars in value, market-beating returns are mathematically harder. Size is its own headwind.

The synthesis: Berkshire is no longer a bet that you'll beat the market - it's a bet that prudence, cash, and low volatility will be rewarded in an expensive, AI-feverish market. Held as an alpha engine, it will likely disappoint. Held as ballast - the steady core that lets you own riskier things elsewhere - it does exactly its job. The mistake isn't owning it; it's owning it for the wrong reason.

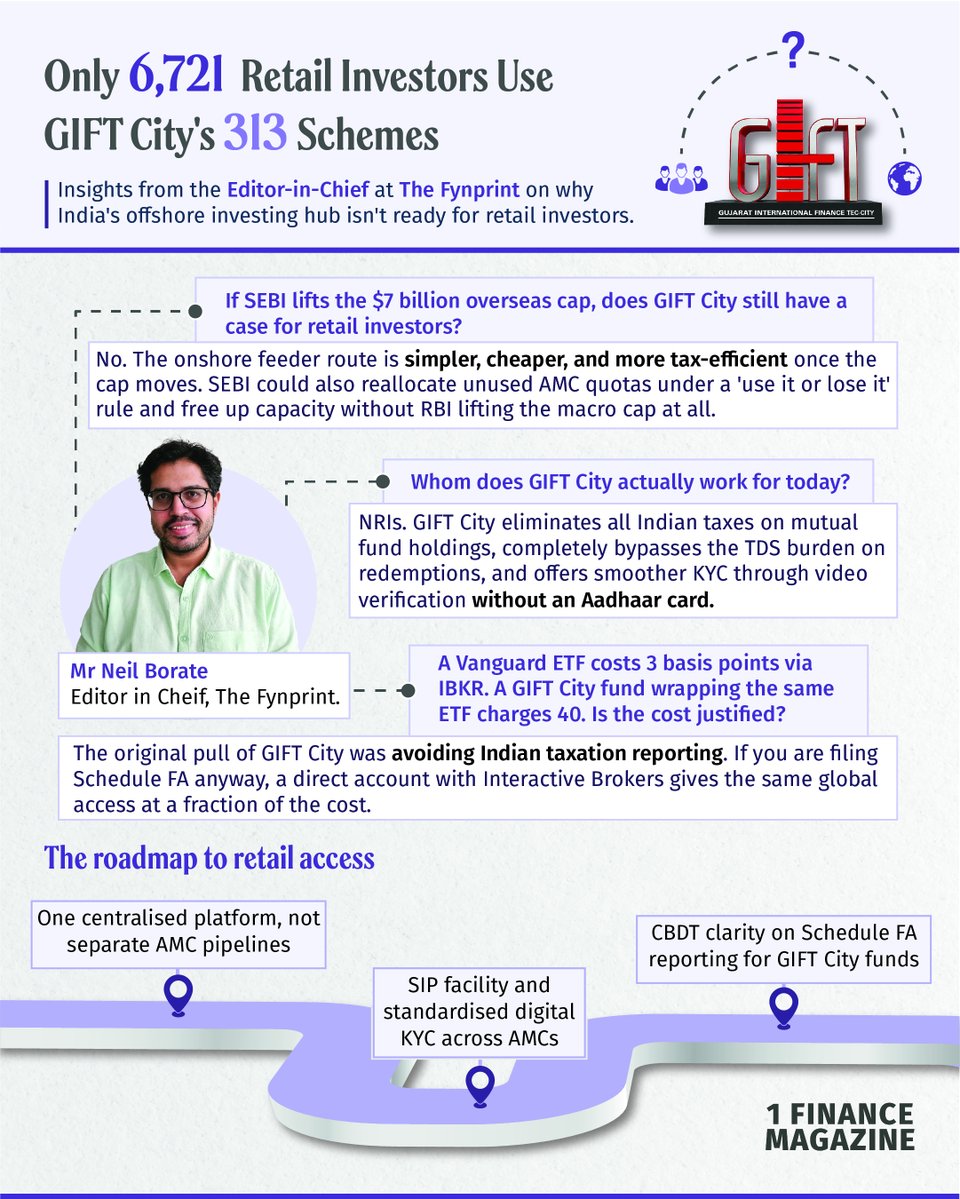

GIFT City gets pitched to almost every client I meet as the smart way into global markets.

For a lot of them, it's an expensive detour.

So for our March 2026 edition of @1FinanceHQ magazine, instead of repeating the pitch, we asked Neil Borate (@ActusDei) the questions the sales decks skip.

@Attain_Zero 1) BRK - 18%, other two are 9% each approx.

2) I don't try to own every sector.

3) Brazil is my third largest. Also have Mexico, Vietnam, China, Indonesia, Japan in lesser proportions. I'm actively increasing China's weight.

We didn’t start FinRight to solve PF.

PF found us.

People were stuck with rejected claims, KYC issues, transfer delays and no clear next step.

That’s when we realised PF doesn’t need more confusion.

It needs the right guidance.

If your PF claim, transfer or withdrawal is stuck, don’t keep guessing.

Book a call with our PF expert today.

#EPFO #PFWithdrawal #PFClaim #PFTransfer #finright

@PrismVault Legacy & personal circumstances. I started investing in the US many years ago, before I knew about UCITS. Shifting incurs taxes. And I'm single with no kids. Estate planning takes a back seat a bit. Over time I may move to ucits or gift

Investing abroad is not unpatriotic. Profits from global investments are still taxed in India, and individual wealth generation contributes to the national economy through spending.

- Neil Borate (@ActusDei ) on Global Investing

Indians do look at global markets for opportunities. Why?

Cheaper stocks, stronger moats sometimes.

Some investors it a full-time pursuit. We profile one such former Uber executive in Chennai today. Story by @PosteAnil

https://t.co/gs3cw86q5x

DSP GIFT City Update:

Underperformance by Design: The fund has underperformed by explicitly sitting out a large portion of the AI hardware cycle. Management notes they are constructive on AI but refuse to pay upfront for high expected earnings.

Idiosyncratic Drivers: Recent positive performance came from bottom-up, non-benchmark ideas. Top contributors for May included Swedish zinc smelter Boliden AB (+19.9%) and Constellation Software (+12.6%).

Concentration Risks: The fund holds 28 stocks, but exposure is heavily concentrated. The top 10 positions account for 43.2% of the portfolio, led by Amazon (6.4%) and TSMC (5.8%).

High Cash Drag: The portfolio is currently sitting on a 24.8% cash level. Management states this isn't a macro call, but rather a result of a lack of new ideas meeting their hurdle return expectations.

Summary: Operating out of GIFT City, this unconstrained fund is currently a steep contrarian bet. For investors looking at it, the core question is whether its high cash drag and lack of mainstream AI exposure will eventually be rewarded by a market valuation correction.