I've been fighting this whole time with my hands tied behind my back. Now I am unleashed.

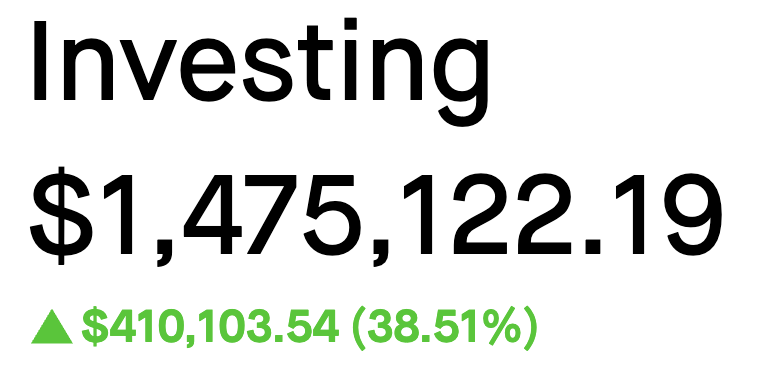

My mind, the very thing they mocked, just built a public portfolio worth $1.475 million with my

company valued over $50 million.

You're not just going to see my brain power. You're going to feel it rumble through the ground

beneath your feet. $CLOV $OPEN $SOFI

$CLOV

Watch what happens when I stop typing and start talking.

I tell it what I want to look at, I press OK, and the mouse starts moving on its own. I am not touching anything. It takes over the whole browser, does the work, and answers my questions the entire time, like I am sitting next to a colleague who never gets tired.

This is AL Stock Trades Intelligence, the agentic system I have been building for years. Blood, sweat, and a lot of long nights went into it. Getting to finally share it is humbling in a way I did not expect.

The early feedback from people I trust has meant the world to me. I am honored anyone took the time at all.

In this clip I asked it to break down Clover Health. Fair warning, it came back a good deal more bullish than I am, which made me laugh.

So let me be clear about a few things. I hold a position in CLOV, which means I am not neutral. None of this is financial advice. It is for educational purposes only, and you should take every word, mine and the machine's, with a healthy grain of salt. Always do your own homework.

The part I keep coming back to is my local high school. I cannot wait to put this in front of them and give them the kind of head start I never had growing up. That is what all of this was really for.

Enough from me. Press play and tell me what you saw.

$CLOV

I am going to speculate here, but after taking some time to digest this graph, something jumps out immediately.

You see the green sections below, which of course includes Clover, sitting far above the rest. Then you see the red.

Sure, you could say this is simply big versus small. But I think we already moved past that conclusion. The real story is new versus old.

Here is where I want to take it one step further.

What Clover may have just demonstrated, based on this data, is something much bigger.

If you remove administrative metrics from the equation, the companies shown in green, including Clover, suddenly separate themselves from the pack because they are focused on clinical quality.

Meanwhile, many healthcare insurance incumbents have spent years optimizing for administration instead of optimizing for patient outcomes.

Talk to almost any doctor and they will probably tell you exactly that, maybe with more colorful language.

Most people already knew this intuitively.

But seeing it illustrated this clearly is different.

When you remove metrics designed for administrators that have nothing to do with actual healthcare and nothing to do with patient A1C levels, what appears is a massive divergence between old systems and new systems.

If I were an incumbent right now, whether that is Humana, UnitedHealthcare, or others, I would be paying attention.

Because CMS has already signaled that many of these measures were eventually going away.

That means survival becomes simple.

Change or get left behind.

If I were running one of these incumbents today, I see only two paths.

Spend billions building a system that actually works. Which I think it's risky especially if it doesn't work.

Or use somebody else's.

Personally, I am speculating the answer might be Counterpart Health.

The future is going to be interesting.

Good luck everyone.

$CLOV $ALHC $HUM $UNH $ELV

One Chart Just Showed Who Medicare Advantage Was Really Leaning On

Clover Health did not just win a lawsuit last week. It handed the entire Medicare Advantage industry a mirror, and most of the giants do not love what they see in it.

On May 27 a federal judge in Georgia ordered CMS to set aside and recalculate Clover's 2026 Part C Star Rating on its main PPO plan. Every other Star Ratings fight you have heard about argued that the government counted wrong. Clover argued something far more dangerous. It argued the government was never allowed to count certain quality measures in the first place. That is the gap between disputing a referee's call and asking whether the rule was ever written into the book.

For a few days that stayed a legal abstraction. Then Yubin Park, PhD, a data scientist and the founder of mimilabs, turned it into a number. He pulled the specific Part C measures in dispute out of the formula, recalculated the weighted scores for every parent company in the program, and plotted the result. One picture. Sixty nine companies. And it carries the part of the story the court filing never could.

Read it like a map.

Left to right is where a company stands today on its Part C Stars. That vertical red line at four stars is not decoration. It is a cliff edge. Stand on the high side and the federal bonus payments swell. Slip just below it and they disappear.

Top to bottom is the consequence of Clover's argument. A bubble that floats upward gains points once the disputed measures vanish. A bubble that sinks loses them. Height is simply telling you whether those measures were quietly helping a company or quietly hurting it.

Bubble size is the number of contracts a company holds, so the fat circles are the names you already know and the small ones are the upstarts. Green marks the companies that come out ahead. Red marks the ones that fall back. And the single purple diamond, parked near the very top, is Clover.

Clover gaining the most is the least shocking thing on the chart. Nobody sues over measures that were doing them favors.

The shock is the formation around it, and this is the read Park pulls into focus. The companies bleeding red are not a random scatter. They are the incumbents. UnitedHealth. CVS Aetna. Elevance. Centene. Humana. The heaviest circles on the board. The companies climbing into the green sit on the opposite side. Devoted Health. Alignment. SCAN. Provider Partners. Newer, smaller, built in a different decade. As Park puts it, the easy assumption is that this is a story about size, when it is really a story about generation. The established names give ground. The younger ones take it.

Here is the reason from the ground up. The measures Clover challenged are mostly the service and access layer. Phone support. Call center availability. Member satisfaction surveys. Care coordination. Whether patients felt they were seen quickly. Those are precisely the operations a sprawling insurer with decades of call center muscle tends to run well, and they are not the same thing as clinical results. Take that service layer out of the score and what remains leans toward actual medical quality, where the leaner newcomers suddenly stop looking outgunned.

So the uncomfortable read is this. A real slice of the incumbents' Star advantage may have been resting on operational polish rather than better medicine. Clover went hunting for relief for one plan. What it exposed was a question about how the entire scoreboard is built.

This is not a contest for bragging rights. Clover told the court that the slide from four stars to 3.5 is worth roughly 120 million dollars to one company in a single year. Run that math across every giant sitting in the red and the number gets serious fast. And Stars do far more than pay bonuses. They decide which plans may grow, which get frozen out of expansion, and which can be terminated. The rating behaves less like a prize and more like a permit to operate.

A few honest guardrails before anyone sprints too far. The ruling binds Clover today and no one else. CMS has already asked the judge to reconsider, (that motion was denied) and appeals are widely expected. And Park is candid that this is a fast directional model rather than a courtroom grade actuarial study. Individual bubbles may shift. The overall shape is the part that is hard to dismiss.

What stays with me is how quietly it happened. No alarm went off. It took one curious analyst, one clean dataset, and one chart to suggest that a small plan's lawsuit may have traced a fracture running directly beneath the largest names in the business. Watch what the incumbents do next. Whether they stay silent or start filing will tell you how seriously they are taking it.

I am not an investment adviser and this is not investment advice. This is market education and my own reading of a public court ruling and a public dataset. Always do your own homework before you put a dollar at risk.

Analysis and chart by Yubin Park, PhD.

Citations

Park, Y. (2026, May 30). Clover vs. CMS:

The Battle Line Goes Far Beyond Clover [Post with data visualization]. LinkedIn. Chart titled "Parent Org: Avg Published Part C Star vs Score Change Under Clover Ruling." Underlying data: mimilabs (dataset mimi_ws_1.partcd, 2026), weighted per the CMS 2026 Star Ratings Technical Notes, covering 69 parent organizations with at least two contracts.

-Building on: Assefa, J. (2026, May 29). When a Three-Leaf Clover Wants a Fourth Star [Article].

@Badie912 I think with how fast counterpart is growing and other interoperability measures alongside the success of @EvidenceOpen, it's very clear that people are realizing that health care needs reform to bend the cost curves downwards.

$CLOV $ALHC $HUM $UNH $ELV

One Chart Just Showed Who Medicare Advantage Was Really Leaning On

Clover Health did not just win a lawsuit last week. It handed the entire Medicare Advantage industry a mirror, and most of the giants do not love what they see in it.

On May 27 a federal judge in Georgia ordered CMS to set aside and recalculate Clover's 2026 Part C Star Rating on its main PPO plan. Every other Star Ratings fight you have heard about argued that the government counted wrong. Clover argued something far more dangerous. It argued the government was never allowed to count certain quality measures in the first place. That is the gap between disputing a referee's call and asking whether the rule was ever written into the book.

For a few days that stayed a legal abstraction. Then Yubin Park, PhD, a data scientist and the founder of mimilabs, turned it into a number. He pulled the specific Part C measures in dispute out of the formula, recalculated the weighted scores for every parent company in the program, and plotted the result. One picture. Sixty nine companies. And it carries the part of the story the court filing never could.

Read it like a map.

Left to right is where a company stands today on its Part C Stars. That vertical red line at four stars is not decoration. It is a cliff edge. Stand on the high side and the federal bonus payments swell. Slip just below it and they disappear.

Top to bottom is the consequence of Clover's argument. A bubble that floats upward gains points once the disputed measures vanish. A bubble that sinks loses them. Height is simply telling you whether those measures were quietly helping a company or quietly hurting it.

Bubble size is the number of contracts a company holds, so the fat circles are the names you already know and the small ones are the upstarts. Green marks the companies that come out ahead. Red marks the ones that fall back. And the single purple diamond, parked near the very top, is Clover.

Clover gaining the most is the least shocking thing on the chart. Nobody sues over measures that were doing them favors.

The shock is the formation around it, and this is the read Park pulls into focus. The companies bleeding red are not a random scatter. They are the incumbents. UnitedHealth. CVS Aetna. Elevance. Centene. Humana. The heaviest circles on the board. The companies climbing into the green sit on the opposite side. Devoted Health. Alignment. SCAN. Provider Partners. Newer, smaller, built in a different decade. As Park puts it, the easy assumption is that this is a story about size, when it is really a story about generation. The established names give ground. The younger ones take it.

Here is the reason from the ground up. The measures Clover challenged are mostly the service and access layer. Phone support. Call center availability. Member satisfaction surveys. Care coordination. Whether patients felt they were seen quickly. Those are precisely the operations a sprawling insurer with decades of call center muscle tends to run well, and they are not the same thing as clinical results. Take that service layer out of the score and what remains leans toward actual medical quality, where the leaner newcomers suddenly stop looking outgunned.

So the uncomfortable read is this. A real slice of the incumbents' Star advantage may have been resting on operational polish rather than better medicine. Clover went hunting for relief for one plan. What it exposed was a question about how the entire scoreboard is built.

This is not a contest for bragging rights. Clover told the court that the slide from four stars to 3.5 is worth roughly 120 million dollars to one company in a single year. Run that math across every giant sitting in the red and the number gets serious fast. And Stars do far more than pay bonuses. They decide which plans may grow, which get frozen out of expansion, and which can be terminated. The rating behaves less like a prize and more like a permit to operate.

A few honest guardrails before anyone sprints too far. The ruling binds Clover today and no one else. CMS has already asked the judge to reconsider, (that motion was denied) and appeals are widely expected. And Park is candid that this is a fast directional model rather than a courtroom grade actuarial study. Individual bubbles may shift. The overall shape is the part that is hard to dismiss.

What stays with me is how quietly it happened. No alarm went off. It took one curious analyst, one clean dataset, and one chart to suggest that a small plan's lawsuit may have traced a fracture running directly beneath the largest names in the business. Watch what the incumbents do next. Whether they stay silent or start filing will tell you how seriously they are taking it.

I am not an investment adviser and this is not investment advice. This is market education and my own reading of a public court ruling and a public dataset. Always do your own homework before you put a dollar at risk.

Analysis and chart by Yubin Park, PhD.

Citations

Park, Y. (2026, May 30). Clover vs. CMS:

The Battle Line Goes Far Beyond Clover [Post with data visualization]. LinkedIn. Chart titled "Parent Org: Avg Published Part C Star vs Score Change Under Clover Ruling." Underlying data: mimilabs (dataset mimi_ws_1.partcd, 2026), weighted per the CMS 2026 Star Ratings Technical Notes, covering 69 parent organizations with at least two contracts.

-Building on: Assefa, J. (2026, May 29). When a Three-Leaf Clover Wants a Fourth Star [Article].

@Badie912 Absolutely. The question that I have is: Is this new lawsuit going to increase the probability of the amount of eyes on Clover Health? That then people will come to the realization of the hypothesis that I've had for a while, which will help be a catalyst?

$CLOV

Quick follow up on the Clover Insurance v. HHS case.

Earlier I posted about the government's Motion for Reconsideration filed on May 28. Clover's legal team responded the next day, on May 29, with their opposition brief.

Here is what Clover filed.

Clover's opposition argues the court should deny the government's motion outright. They make four main points.

First, they say the government invoked the wrong rule. Rule 60(a), which the government cited, is for fixing tiny clerical errors like a typo in a dollar amount. It cannot be used to undo a substantive ruling like setting aside a Star Rating.

Second, they argue that under Rules 60(b)(1) and 59(e), which do allow a court to reconsider a decision, the moving party has to show something genuinely new that the court did not already consider. Clover says the government's reply brief is largely a copy of arguments already made in their earlier 60 page opposition and cross-motion, which the court already addressed in the 72 page ruling. Nothing new, no basis for reconsideration.

Third, and this is the sharpest point in my view, Clover notes that the late reply brief was a reply to the government's own cross-motion, not to Clover's motion for summary judgment. Clover's motion (the one the court granted) had its briefing fully closed back on April 29. So even if the court reads the government's late reply, it has no direct bearing on the order granting Clover's motion. That reply was about supporting the government's losing cross-motion, which is a separate matter.

Fourth, Clover walks through the procedural history to argue the government created this situation themselves. They missed an earlier February deadline by over a month and a half. The court already excused that default once. Then instead of filing a proper motion to extend the May 8 reply deadline under Local Rule 6.1, the government slipped an extension request into a different motion about page lengths. Clover's position is that you cannot bury an extension request inside an unrelated filing and then claim the court made a mistake.

My personal take, again I am not a lawyer and this is just my own read as someone following the case:

I think Clover's third argument is the most important one strategically. By pointing out that the late reply was on the cross-motion and not on Clover's own motion, Clover gave the judge a clean way to deny reconsideration without having to admit any error. The judge can essentially say that even if the reply had been considered, it would not have affected the outcome of Clover's motion, which was already fully briefed and granted on its merits.

That move accomplishes two things at once. It preserves Clover's win at the district court level, and it weakens the appellate argument the government was trying to set up by getting the late reply formally rejected.

Why is Clover moving so fast? They want to start the recalculation clock. Every day this drags out at the district level is a day CMS is not actually recalculating the rating. Clover's brief literally tells the court that the government should "focus their efforts on expeditiously effectuating the Court's judgment." Translation: stop stalling, start recalculating.

The realistic outcome here, in my opinion, is that the judge denies the government's motion, possibly notes the extension was granted, but rules that the reply would not have changed her decision anyway. That gives the government a marginally cleaner record but keeps Clover's substantive win intact.

The district court phase is winding down. The next real question is whether the government files a notice of appeal to the Eleventh Circuit and whether anyone seeks to stay the recalculation order during that appeal.

Pace of filings tells you something too. Government filed Thursday. Clover responded Friday. Both sides moving fast.

Curious to hear what the lawyers and federal court watchers in the community think. Am I reading this right? Anything I am missing? Open town hall.

$CLOV

Beat earnings. Raise guidance. Announce a major SaaS deal. Stock drops 20%.

Heard it here first, right?

I screenshotted this Reddit exchange a while back and I have been sitting on it. I blanked out the names because these are hard working people just like all of us, and I want to keep this purely educational using real market commentary.

Look closely and you can see something important. Retail has been conditioned to expect this stock to go down. And here is what most people miss. A pattern is only a pattern until it isn't.

So why did the stock struggle in 2025? It wasn't magic. Part D costs spiked. That pressured operational cash flow, driven in large part by rising net income losses. The market saw deterioration and it priced it in.

Now rewind to 2024. Fundamentally the company performed far better, and the stock was rewarded handsomely for it. In Q2 2024 alone, Clover Health posted positive net income of $7.41 million.

So here is what I keep coming back to.

I look at these comments. Then I look at the Robinhood trading trends, which show real retail activity. And what I see right now is enormous net selling. Retail is rushing for the exit at the exact moment this company is on track for its first net income profitable year.

That leaves two possibilities.

One. Retail sees something the market doesn't. Maybe medical costs keep climbing and 2025 repeats itself.

Two. This is the handoff. The transition where retail sells and institutions accumulate. The crowd calls them smart money. We have watched this exact movie play out before, and I can show you the data on Palantir.

I am not a financial advisor and I am not licensed in finance. This is simply my opinion and personal commentary. But I believe it is the second one. I believe Clover Health is in the middle of a real turnaround, and it is hard to watch people who held through everything fold right at the finish line.

Here is something else I have noticed. As the price falls, the negativity crawls out of the woodwork. I block a lot of it, because I choose to surround myself with people who are fair, balanced, and capable of actual critical thinking.

Let me put my neuroscience hat on for a second, since that happens to be one of my degrees. One of my favorite lectures covered how the brain runs on inhibition. Cut the head off a chicken and the body keeps sprinting around the yard. Why? Because the inhibitory signal is gone. No direction. No control. Just motion for the sake of motion.

That is exactly what a lot of these voices online remind me of. No filter. No signal. No purpose. Just noise running in circles. People call them trolls. I call them a body with no head.

I ignore them. But plenty of good people get rattled by it, and I think that is the entire point. They call it fear, uncertainty, and doubt for a reason. It is part of the game.

And the game rewards patience. Ask Warren Buffett, who has been repeating the same lesson for decades. Psychology is most of the battle. Fundamentals carry the rest.

For those of you who have followed me from the beginning, you know I have done my best to stay honest, lead with integrity, and bring you the strongest research I can find, because I love discovery. I am a scientist at heart.

You have also watched something rare. You have watched people whose conviction was supposedly built on first principles fold in the final minute. It is almost biblical. Selling out right before what I call a triple dragon. That is the moment a company flips from negative to positive across all three at once: operational cash flow, free cash flow, and net income.

It is wild to witness. Almost like watching an NPC inside a simulation follow a script.

And that part has been the most educational of all. It is one thing to read the data and see retail selling while institutions grow their stake through SEC 13F filings. It is another thing entirely to watch real people online live through the exact wealth transfer Wall Street politely labels as dumb money moving to smart money. That lesson is burned into my hippocampus.

Noise aside, we have built something beautiful here, and I am grateful for every one of you. When someone in this community does the work, I cite them, because we are all in this together and together we are stronger.

I cannot wait to see what we build from here.

$CLOV

A lot of people spent the last year calling Andrew Toy a terrible CEO. The public record disagrees, and it is not close.

Go back to the third quarter 2025 earnings call on November 4. Clover had just been handed a 3.5 star rating for the 2026 ratings year, down from 4. A weak CEO spins that. He buries it in a slide, blames the environment, and moves on. Toy did the opposite. He put it at the top of the call and said the misses were not acceptable. His words, not mine: "these misses aren't at all acceptable to us." Then he named the aspiration behind it without flinching. Four stars, not 3.5.

Then he showed the receipt that actually counts. On that same call, Clover pointed to its HEDIS score of 4.72, among the best clinical quality scores of any PPO in the country. Sit with that. The clinical care was elite. What dragged the composite rating was the administrative and process scoring, not the medicine.

So the company did the unglamorous thing. It took that argument to federal court.

On May 27, a federal judge found CMS improperly included twenty measures in Clover's calculation and ordered the rating recalculated, the rating that sits under roughly 120 million dollars in bonus payments. To be precise, because precision is the whole point, the recalculation is not finished and the government has asked the court to reconsider. I am not declaring a final number. I am telling you what a judge has already put in writing.

Now line it up. Owned the miss on the record. Showed elite clinical scores. Named the four star bar. Took the methodology to court and got a federal judge to agree the measures were applied unlawfully.

That is not the profile of a terrible CEO. That is the profile of one who tells you exactly what he is going to do and then goes and does it.

Here is the part the critics will not enjoy. One number is not a diagnosis. They saw 3.5, called time of death, and never opened the rest of the chart. The HEDIS score, the methodology, the legal filings, all of it public, all of it ignored. Rendering a verdict from a single data point is not analysis. It is impatience dressed up as expertise.

I read the full record before I form an opinion. That is the only difference between my read and theirs, and it is the difference between being early and being loud.

Not investment advice. Just the public filings, read in full and out loud.

The chart was always there. Most people just refused to turn the page.

$CLOV

I said this was grounds for an appeal. I got laughed at in the replies. On May 27, a federal judge wrote that argument into a court order.

Here is the timeline that ends the debate.

November 7. Clover quietly files suit against CMS over the star ratings downgrade.

November 25. I post that the downgrade is grounds for an appeal. I had never read the complaint. I reached the same conclusion Clover's attorneys did, from the same public record, on my own. Eighteen days apart, same logic, zero coordination.

The reasoning was not complicated. You do not bury a plan under bloated administrative measures and then call the score a verdict on clinical quality. If the ruler is bent, the measurement is challengeable.

May 27. The court partially grants Clover summary judgment, finds CMS improperly included twenty measures, and orders the agency to recalculate the PPO rating that sits under roughly 120 million dollars in bonus payments. Two independent grounds. CMS used data it had no statutory authority to use. And CMS skipped the notice and comment rulemaking the law requires before adding measures to the system.

A court did not say Clover got unlucky. A court said the measures were applied unlawfully.

Watch how cleanly the pieces lock. CMS itself went on record that the system leaned too hard on administrative and process measures and too little on outcomes. The court then threw out measures built on call center data and similar inputs. The agency's own words and the judge's order landed on the exact same target. That is not a coincidence. That is a confession meeting a verdict.

Let me be precise, because precision is the thing they cannot stand. I never promised a final star count and I am not promising one now. Recalculation is pending and the government has asked the court to reconsider. What I claimed was that grounds existed. They did. In writing. From a judge.

Now the uncomfortable part for the people who showed up to lecture me. Their stance was a prediction. Clear measures, Clover blew it, move on. That prediction is currently sitting under a court order to recalculate. Predictions get tested. Mine passed. Theirs did not.

So the only swing left is the one that takes no thought at all. Attack the person instead of the chain of logic. It is the cheapest move on the board, because it costs zero reasoning to throw. Reach for it and you are announcing you ran out of argument several exits back.

I will keep showing my work, link by link, from public filing to conclusion, so anyone can audit every step. Find a crack in the lattice and I will hear you out. Swing at the man instead and you have only confirmed the structure holds.

The order is public. Clover Insurance Company v. HHS, Southern District of Georgia, case 2:25-cv-00142. Do not take my word for it. Read it.

Not investment advice. Just someone reading the public docket out loud.

The receipts were never hidden. I just keep stacking them.

$CLOV

CMS said:

- Too many administrative measures

- Too little focus on outcomes

- Need to remove 12 measures

- Need a more stable, simplified, fair system

- Need less emphasis on process measures

- Need better reflection of true clinical quality

This is exactly Clover's argument:

"Don't punish us for BS admin measures when our clinical outcomes are excellent."

This is grounds for an appeal...

@JO_Nathan777@ALSTOCKTRADES I appreciate you so much, brother! Blood, sweat, and tears and to think that we went from excel spreadsheet to a full agentic autonomous model!

This is @AlbertAlan and what he has built @ALSTOCKTRADES I am learning so much from him and his platform, and one day I will be able to teach others what I have learned to not only my family but others in my life and continue to build with the amazing people in our platform.

![AlbertAlan's tweet photo. $CLOV $ALHC $HUM $UNH $ELV

One Chart Just Showed Who Medicare Advantage Was Really Leaning On

Clover Health did not just win a lawsuit last week. It handed the entire Medicare Advantage industry a mirror, and most of the giants do not love what they see in it.

On May 27 a federal judge in Georgia ordered CMS to set aside and recalculate Clover's 2026 Part C Star Rating on its main PPO plan. Every other Star Ratings fight you have heard about argued that the government counted wrong. Clover argued something far more dangerous. It argued the government was never allowed to count certain quality measures in the first place. That is the gap between disputing a referee's call and asking whether the rule was ever written into the book.

For a few days that stayed a legal abstraction. Then Yubin Park, PhD, a data scientist and the founder of mimilabs, turned it into a number. He pulled the specific Part C measures in dispute out of the formula, recalculated the weighted scores for every parent company in the program, and plotted the result. One picture. Sixty nine companies. And it carries the part of the story the court filing never could.

Read it like a map.

Left to right is where a company stands today on its Part C Stars. That vertical red line at four stars is not decoration. It is a cliff edge. Stand on the high side and the federal bonus payments swell. Slip just below it and they disappear.

Top to bottom is the consequence of Clover's argument. A bubble that floats upward gains points once the disputed measures vanish. A bubble that sinks loses them. Height is simply telling you whether those measures were quietly helping a company or quietly hurting it.

Bubble size is the number of contracts a company holds, so the fat circles are the names you already know and the small ones are the upstarts. Green marks the companies that come out ahead. Red marks the ones that fall back. And the single purple diamond, parked near the very top, is Clover.

Clover gaining the most is the least shocking thing on the chart. Nobody sues over measures that were doing them favors.

The shock is the formation around it, and this is the read Park pulls into focus. The companies bleeding red are not a random scatter. They are the incumbents. UnitedHealth. CVS Aetna. Elevance. Centene. Humana. The heaviest circles on the board. The companies climbing into the green sit on the opposite side. Devoted Health. Alignment. SCAN. Provider Partners. Newer, smaller, built in a different decade. As Park puts it, the easy assumption is that this is a story about size, when it is really a story about generation. The established names give ground. The younger ones take it.

Here is the reason from the ground up. The measures Clover challenged are mostly the service and access layer. Phone support. Call center availability. Member satisfaction surveys. Care coordination. Whether patients felt they were seen quickly. Those are precisely the operations a sprawling insurer with decades of call center muscle tends to run well, and they are not the same thing as clinical results. Take that service layer out of the score and what remains leans toward actual medical quality, where the leaner newcomers suddenly stop looking outgunned.

So the uncomfortable read is this. A real slice of the incumbents' Star advantage may have been resting on operational polish rather than better medicine. Clover went hunting for relief for one plan. What it exposed was a question about how the entire scoreboard is built.

This is not a contest for bragging rights. Clover told the court that the slide from four stars to 3.5 is worth roughly 120 million dollars to one company in a single year. Run that math across every giant sitting in the red and the number gets serious fast. And Stars do far more than pay bonuses. They decide which plans may grow, which get frozen out of expansion, and which can be terminated. The rating behaves less like a prize and more like a permit to operate.

A few honest guardrails before anyone sprints too far. The ruling binds Clover today and no one else. CMS has already asked the judge to reconsider, (that motion was denied) and appeals are widely expected. And Park is candid that this is a fast directional model rather than a courtroom grade actuarial study. Individual bubbles may shift. The overall shape is the part that is hard to dismiss.

What stays with me is how quietly it happened. No alarm went off. It took one curious analyst, one clean dataset, and one chart to suggest that a small plan's lawsuit may have traced a fracture running directly beneath the largest names in the business. Watch what the incumbents do next. Whether they stay silent or start filing will tell you how seriously they are taking it.

I am not an investment adviser and this is not investment advice. This is market education and my own reading of a public court ruling and a public dataset. Always do your own homework before you put a dollar at risk.

Analysis and chart by Yubin Park, PhD.

Citations

Park, Y. (2026, May 30). Clover vs. CMS:

The Battle Line Goes Far Beyond Clover [Post with data visualization]. LinkedIn. Chart titled "Parent Org: Avg Published Part C Star vs Score Change Under Clover Ruling." Underlying data: mimilabs (dataset mimi_ws_1.partcd, 2026), weighted per the CMS 2026 Star Ratings Technical Notes, covering 69 parent organizations with at least two contracts.

-Building on: Assefa, J. (2026, May 29). When a Three-Leaf Clover Wants a Fourth Star [Article].](https://pbs.twimg.com/media/HJqnisKb0AAJAlS.jpg)