Bad $DLO eps print unfortunately, good revenue, but in this environment you miss by a little bit and you get destroyed. It is what it is.

I'm curious to see why they missed, gotta listen into the earnings call.

$DLO is still the fastest growing publicly traded business in Latin America.

And by far one of the cheapest.

PE Ratio: 21

PEG Ratio: 0.92

Forward PE Ratio: 13

Price-To-FCF: 10

PS Ratio: 3.75

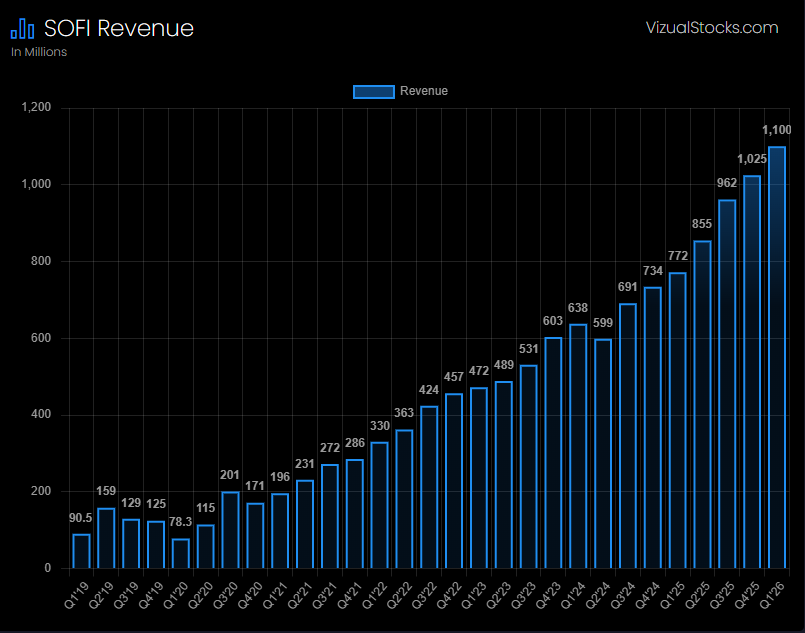

$SOFI has done nothing but improve fundamentals since going public. So the question I’m always asked is why isn’t the price action responding accordingly?

It’s a fair question.

IMO the answer is actually very simple.

The float also changed and NOT for the better.

They went public with about 530M shares outstanding according to Super Grok. Now the float sits at about $1.28B

If you can’t understand how that makes it harder for share price to rise, I’m not the person that can help it make sense.

SOFI bulls rarely mention this aspect, but that doesn’t meant it didn’t happen.

Dilution has occurred as with most businesses that are up and coming.

The dilution has been substantial.

Smarter folks can maybe explain it better than I can.

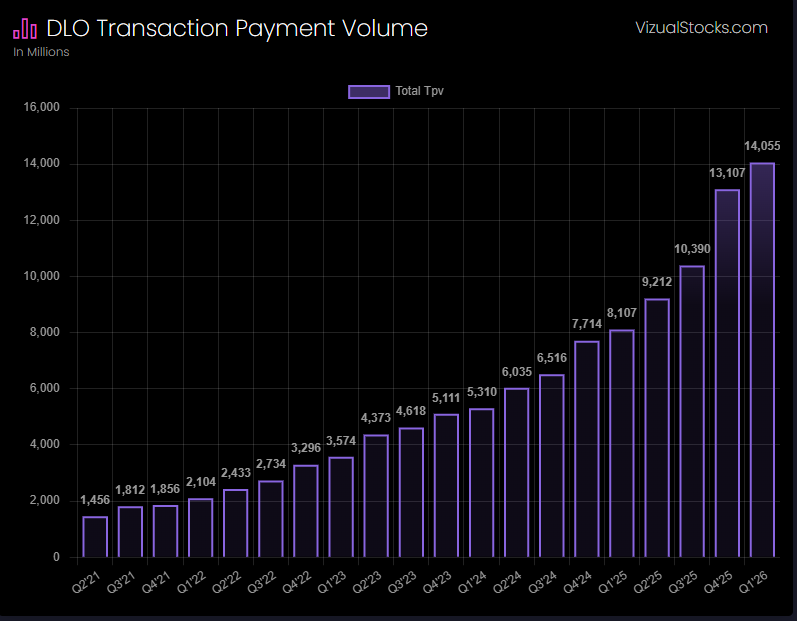

I'm updating my assumptions on $DLO post earnings yesterday.

My previous basic (and conservative) assumptions give a 3.3x (see quoted post). I think that's too conservative.

TPV growth in FY26 is expected to be 55%. I originally said a CAGR of 25% was realistic which would get us to $100B TPV by 2030.

I think we should be looking at ~28% CAGR which gets us to $140.5B in TPV by 2030.

My original take rate was 2.5% in 2030. I think that remains fair. We can look more into this if I decide to get a lot more specific but there's so much back and forth on this. Likely we see take rates continue to decline a bit...before potentially stabilizing or expanding down the road but what exactly that number is I think is quite hard to gauge.

Conservatively, 2.3% is more than fair. If anything, it's probably too low.

2.3% take rate on $140.5B gives $3.23B in revenue in 2030.

FCF margins still are at 30% guided... so 30% on $3.23B in revs gives $969M in FCF (my previous assumptions gave $750M).

With a fairly conservative 15x FCF multiple on $969M you have a $14.5B valuation compared to a $3.37B valuation today.

Conservative? Maybe. Maybe not.

Unrealistic? Most definitely not.