$NTLA getting a late-breaking oral presentation at EAACI for Phase 3 HAELO data is an underappreciated signal.

The trial already met its primary endpoint. Now investors get the full dataset: durability, attack-free rates, safety, and potential best-in-class positioning.

6/13

As an $NTLA shareholder, I don't say this lightly: $PRME has the most compelling platform in gene editing.

It wouldn't surprise me if someone is already doing diligence and simply waiting for the BEAM arbitration to clear.

$PRME shared strong dose-escalation preclinical data for its Wilson’s Disease program in mice models:

0.4 mg/kg ➡️ >40% hepatocytes editing/protein expression (carrier status)

0.8 mg/kg ➡️ 55~75% hepatocytes editing/protein expression

Previous data at an undisclosed dose (1 mg/kg, perhaps?) showed ~90% hepatocytes editing.

Even at 0.4 mg/kg, liver copper was largely restored to normal levels by week 4.

PET imaging 24h post-copper challenge confirmed normal copper metabolism in both 0.4 and 0.8 mg/kg dose groups.

Overall, these are highly promising results. 🤞

Great news for CGD patients with the NCF1 deltaGT mutation.

$PRME is planning for the commercial launch of the PM359 in CGD in 2027+ (hopefully that's 2027).

Intellia is looking forward to giving a late-breaking oral presentation highlighting additional data from HAELO, our Phase 3 clinical trial in #HereditaryAngioedema, and to sharing new research on patients’ continued unmet needs at the upcoming @EAACI_HQ Congress. More details here: https://t.co/2DvsBKQuhd

This weekend, Intellia will have a medical tabletop at the Eastern Allergy Conference in Palm Beach, FL. HCPs: Swing by to meet the team and review our latest educational material.

https://t.co/vcR5kCeW7q

Not to brag, but have you ever seen an analyst with something this beautiful, detailed, and with high level, unique data derived? $NTLA $BBIO $ALNY

I noticed my previous graphic had echo data for Vutri and not CMR. CMR tends to perform better due to many patients with pacemakers etc not being able to take part in CMR.

So here is a very fair and as close to apples to apples look as we can get (24m, 30m, 36m- all CMR).

Small sample sizes, yet really interesting numbers across the board.

Notice Vutri had the healthiest baseline for LV mass and ECV. Here are a few possible explanations as to why the ALNY placebo did so much worse than the BBIO placebo:

1. 36 months vs. only 30 months

2. ALNY baseline was much lower which gave it more room to worsen

Important to note: 100% of extracellular volume isn't amyloid but it is heavily comprised of that. "Consistent with amyloid regression" is the foolproof way to state it.

The note at the bottom is very interesting! Let me know if you have any questions!

$NTLA

"So going into this data set, we were just mindful the market leader has mid- to upper 80% attack rate reductions. We've matched or exceeded that. And from an attack-free status, we have not seen anything more than 44% from that market leader. And the best ever produced is 60%, 62%. So we're right where we want it to be as good or better than all the existing therapies. But we also like to think what we're doing -- we're having -- we're playing an entirely different game, right? It's important to get patients attack-free. But in our case, we do that after a single outpatient 4-hour infusion, and they may never have attacks and never require chronic drug therapy again. That is a profound statement. There are many benefits for patients, but we also see a very strong value proposition with physicians and ultimately with payers that we've been doing work with since last year."

— Edward Dulac, CFO, at BoA Healthcare Conference

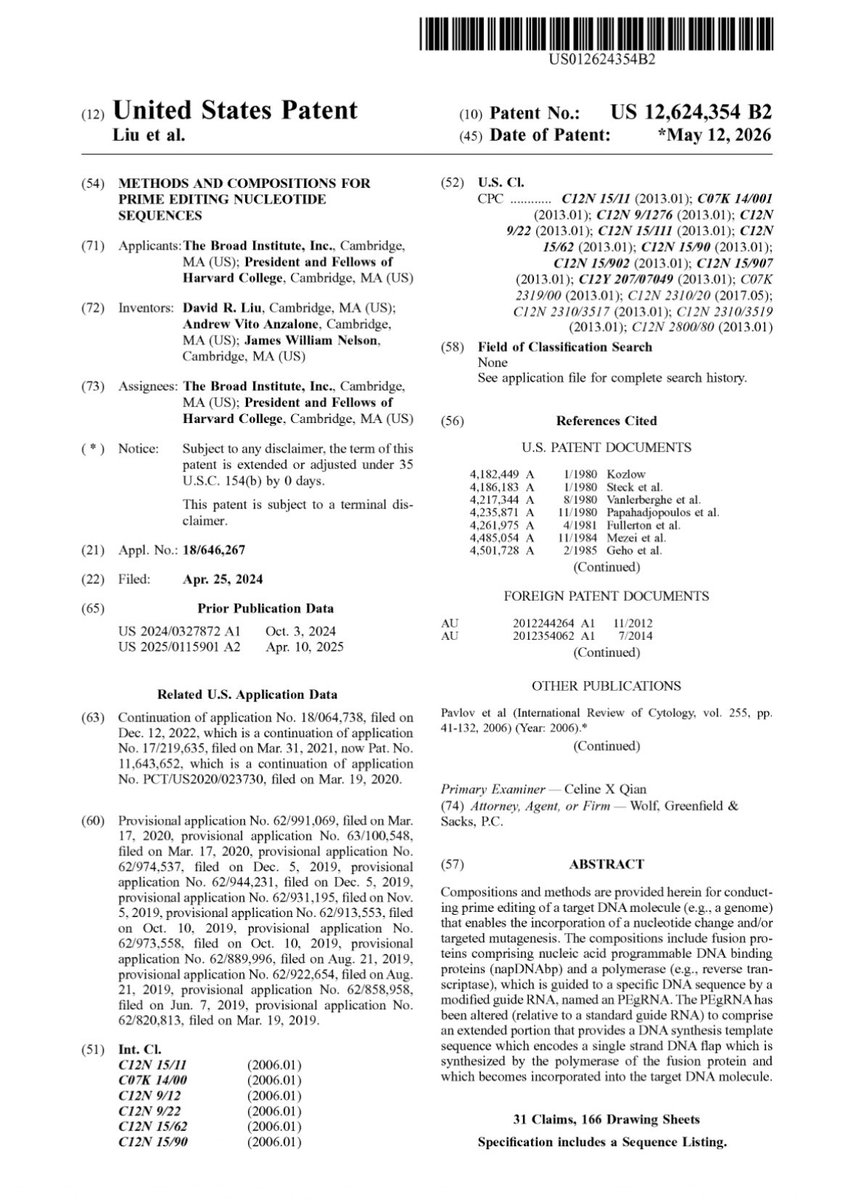

$PRME has significantly strengthened its intellectual property moat. 🧬

Today, May 12, 2026, the USPTO has issued two key patents: US 12,624,354 B2 and US 12,624,353 B2 (“Methods and Compositions for Prime Editing Nucleotide Sequences”).

They are fully granted patents that protect the core prime editing system: the fusion protein (programmable DNA-binding domain + polymerase/RT) and the engineered pegRNA with an extended template that enables precise “search-and-replace” gene editing without double-strand breaks. They cover compositions (the exact fusion protein) and methods (how the complete mechanism works with extended pegRNA).

They are continuations and divisions of the foundational patent family from the Broad Institute and Harvard. These new issuances expand and solidify protection of the core technology that underpins all current and future programs at Prime Medicine.

This fortifies the entire platform: it makes it substantially more difficult for competitors to replicate the system or design workarounds (“design around”), while further strengthening Prime’s exclusive license from the Broad Institute and Harvard for therapeutic use in humans.

A major milestone that reduces competitive and regulatory risks and enhances the long-term value of $PRME. Prime Editing leadership continues to solidify.

Genome editing $ntla 2001 is taking the $bbio stabilizer and $alny RNAi competitors to the cleaners.

Left ventricular mass data dropped, 2001 already miles ahead of competition at 12 months (vs 30 months): solid improvement vs stabilization, even in sicker patients. #attrcm

@EliKorey I think his percent ownership in $PRME at IPO was also very high (maybe ~25%)

The interesting bit is open-market purchases of $PRME, not large quantities, but still...

Interesting ownership dynamic in gene editing:

David Liu owns roughly ~11% of $PRME versus only ~3-5% of $BEAM despite co-founding both.

More interesting: $PRME is the only one where he also made open-market purchases last year while the stock was weak.

Worth paying attention 👀

@BiomedicalRX@PatternNotes Yes, same take on Q1 earnings. No shift in timelines everything is still on schedule. This was a good report. Not sure what people were expecting to justify the ~10% dump yesterday. Adding to my position here.